The Clorox Company's CLX Household segment remains its biggest source of stability, but recent commentary suggests that strength in one business alone may not be enough to drive broader growth. While the segment continues to benefit from solid demand in cleaning products and successful innovation, weakness in a few other categories is weighing on the company's overall momentum.

Management highlighted that the Cleaning business is the portfolio's standout performer. Product launches, including the Clorox PURE allergen platform and additions to the Scentiva lineup, are gaining shelf space, generating strong early consumer response and outperforming internal expectations. Despite an intensely promotional environment, the company has said that it continues to gain market share in cleaning, reinforcing the strength of its flagship brands.

However, the positive momentum in Household is being offset elsewhere. Fresh Step cat litter remains in the middle of a multi-year transformation, with new packaging, product claims and pricing architecture creating temporary disruption. Although distribution gains have met expectations, shelf placement issues and the complexity of converting shoppers to new products have slowed the recovery. Management also acknowledged that Food categories remain under pressure from elevated promotions and weaker-than-expected category demand.

Clorox believes execution rather than demand is the key variable. With the ERP rollout completed, management expects better service levels, stronger on-shelf execution and faster commercialization of innovation. Retail distribution points increased more than 5% in the third quarter of fiscal 2026, while additional shelf resets are expected through the fourth quarter. The company is also expanding revenue growth management initiatives, targeted pricing actions and brand investments to strengthen value perception.

The Household segment provides an important foundation, but Clorox's ability to sustain long-term growth will ultimately depend on whether improvements in Litter, Food and other businesses can match the momentum already visible in Cleaning.

CLX’s Price Performance, Valuation & Estimates

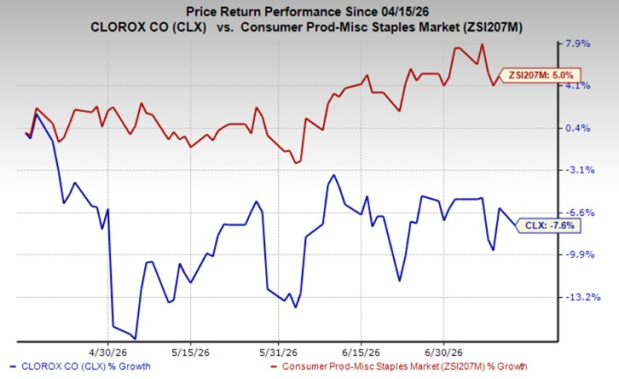

Shares of the Zacks Rank #4 (Sell) company have lost 7.6% in the past three months against the industry’s growth of 5%.

Image Source: Zacks Investment Research

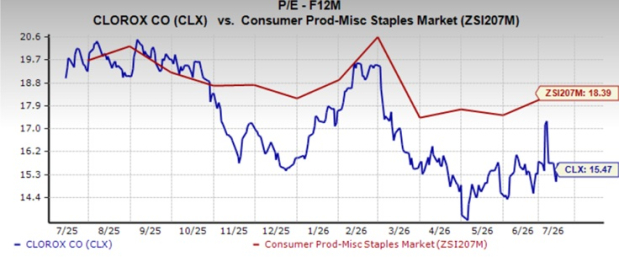

From a valuation standpoint, CLX trades at a forward price-to-earnings ratio of 15.66X compared with the industry’s average of 17.59X.

Image Source: Zacks Investment Research

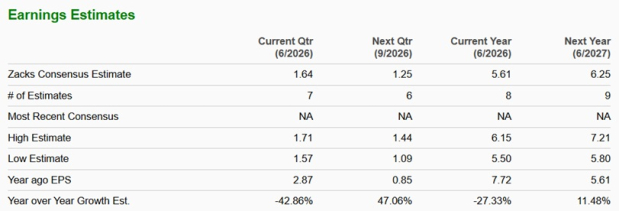

The Zacks Consensus Estimate for CLX’s fiscal 2026 earnings implies a year-over-year decline of 27.3%, while that of fiscal 2027 shows growth of 11.5%. The company’s EPS estimate for fiscal 2026 has been unchanged in the past 30 days.

Image Source: Zacks Investment Research

Stocks to Consider in the Consumer Staples Space

United Natural Foods UNFI is the leading distributor of natural, organic and specialty food and non-food products in the United States and Canada. The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for United Natural Foods’ current financial-year EPS indicates growth of a whopping 254.9% from the prior-year reported level. UNFI delivered a trailing four-quarter earnings surprise of 29.9%, on average.

Church & Dwight Co. Inc. CHD develops, manufactures and markets a broad range of household, personal care and specialty products. The company currently has a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for CHD’s 2026 EPS indicates growth of 6.2% from the previous year’s reported figure. Church & Dwight delivered a trailing four-quarter average earnings surprise of 6.5%.

Krispy Kreme DNUT operates as a branded retailer and wholesaler of doughnuts, coffee and other complementary beverages and treats and packaged sweets. The company currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for Krispy Kreme’s current financial-year EPS indicates growth of 30% from the year-ago reported number. DNUT delivered a trailing four-quarter negative earnings surprise of 6.3%, on average.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Clorox Company (CLX): Free Stock Analysis Report

Church & Dwight Co., Inc. (CHD): Free Stock Analysis Report

United Natural Foods, Inc. (UNFI): Free Stock Analysis Report

Krispy Kreme, Inc. (DNUT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).