JPMorgan Chase & Co. JPM used its second-quarter 2026 earnings call to push the story beyond a headline beat and toward a stronger full-year revenue outlook. Management highlighted a rare mix of elevated market activity, resilient consumer trends and broad-based business momentum.

The call also mattered because executives spent much of the Q&A defending the durability of those tailwinds while updating investors on leadership succession, capital deployment and the bank’s next wave of AI and digital investments.

JPM Raises the 2026 Revenue Bar

Chief financial officer Jeremy Barnum said JPM now expects full-year net interest income excluding Markets of about $96.5 billion, up from the prior $95 billion view. Total NII is now expected to reach about $105.5 billion, helped by roughly $9 billion of Markets NII.

Barnum said the revised outlook reflects stronger deposit balances across wholesale and consumer banking, along with a somewhat firmer rate backdrop. He added that the most important implication is a higher exit run rate into next year.

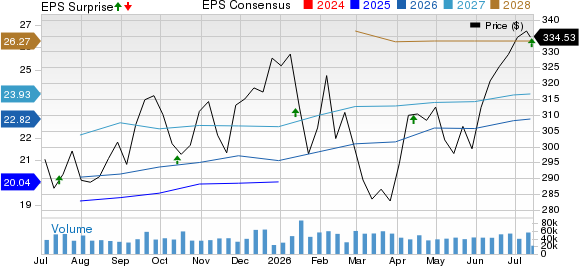

The quarter itself added support. Excluding significant items, JPM reported EPS of $6.14, which topped the Zacks Consensus Estimate of $5.59. Fourth-quarter revenues came in at $57.35 billion, beating the estimate of $49.14 billion.

JPMorgan Chase & Co. Price, Consensus and EPS Surprise

JPMorgan Chase & Co. price-consensus-eps-surprise-chart | JPMorgan Chase & Co. Quote

JPMorgan Sees a Healthy Deal Backdrop

Barnum described the commercial environment as especially supportive in investment banking and trading, though he stopped short of calling it fully repeatable. Investment banking fees rose 30% year over year, while Markets revenues climbed 35%.

He said the banking pipeline remains robust even after some transaction pull-forward, with large equity deals and faster M&A closings helping second-quarter performance. Management also said current activity levels are encouraging more activity rather than shutting it down.

At the same time, Barnum drew a distinction between healthy conditions and permanence. He said the market is clearly risk-on, but JPM is trying to support clients without relaxing its own risk discipline.

JPM’s Consumer Trends Stay Constructive

Barnum said consumers and small businesses remain resilient despite elevated gas prices and inflation. He pointed to solid spending trends, stronger tax refunds and a durable labor market as key supports.

That message aligned with the numbers in Consumer & Community Banking, where revenues rose 8% year over year to $20.3 billion, and net income increased 3% to $5.3 billion. Management also noted more than 500,000 net new checking accounts in the quarter.

On credit, Barnum said delinquencies are tracking better than expected across FICO bands. JPM also lowered its full-year card net charge-off rate outlook to about 3.2%, reflecting stronger consumer performance.

JPMorgan Pushes Growth Despite Cost Pressure

One of the sharper exchanges in the Q&A centered on expenses. Barnum raised the adjusted expense outlook to about $107.5 billion, saying the increase was driven mostly by volume- and revenue-linked costs tied to unusually strong activity.

Jamie Dimon, chairman and chief executive officer, rejected the idea that the bank should manage for perpetual operating leverage. He argued JPM’s model is to keep investing in branches, technology, bankers and marketing while still producing strong returns.

That stance also shaped the AI discussion. Dimon said the bank already has close to 1,000 use cases in motion, with roughly 50 considered especially important across fraud, risk, marketing, hedging, note-taking and document review. He framed AI as a tool to improve service and productivity, not a reason to assume structurally higher margins.

JPM Sticks With Organic Capital Deployment

Capital allocation drew another heavy round of questions after the bank bought back $6.2 billion of stock in the quarter and reported a 14.1% standardized CET1 ratio. Dimon said buybacks are an investment decision, not simply a return of capital.

He said the bank still sees a large set of organic opportunities across cards, branches, payments, digital products and international expansion. That helps explain why management remains willing to preserve flexibility even with returns running well above long-term targets.

On regulation, Dimon again pressed for changes to Basel III endgame proposals, arguing that some capital calculations still double-count risk. Barnum added that regulatory stability would be welcome, but said JPM’s current valuation is not obviously being capped by regulation alone.

JPMorgan Broadens the Leadership Story

Leadership succession also moved to the foreground. Dimon said the elevation of Doug Petno and Troy Rohrbaugh to co-presidents does not change the expected succession timetable, which he again described as being measured in several years and ultimately up to the board.

Dimon defended Rohrbaugh’s move into the consumer role by emphasizing broad management ability, culture and operating depth rather than narrow product experience. He said the bank wants leaders who can carry the franchise across businesses, not just excel in one silo.

That answer fit the broader tone of the call. JPMorgan presented itself as a bank still leaning into growth, still investing through the cycle and still treating today’s unusually favorable environment as a chance to build, not coast.

Zacks Signals Still Favor Selectivity

JPM carries a Zacks Rank #2 (Buy). Under the Zacks framework, Rank #1 (Strong Buy) and #2 stocks have the strongest potential to outperform over the next one to three months, especially when paired with favorable Style Scores. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Style Score picture is mixed. JPM has a Momentum Score of A, but Value, Growth and VGM Scores of F. That combination points to stronger price-action support than broad style-based appeal, and it also means the current Zacks Rank can still change as estimate revisions move after the quarter.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).