Myriad Genetics, Inc. MYGN is well-placed for growth in the coming quarters due to its steady rollout of new testing panels and product enhancements. The company is also progressing in its Cancer Care Continuum strategy, supported by rising demand in hereditary cancer and a 2026 launch calendar. Solid financial health further adds to its appeal. However, coverage and reimbursement changes for GeneSight remain a risk to Myriad Genetics' revenue growth. Macroeconomic headwinds and input cost pressures are other challenges.

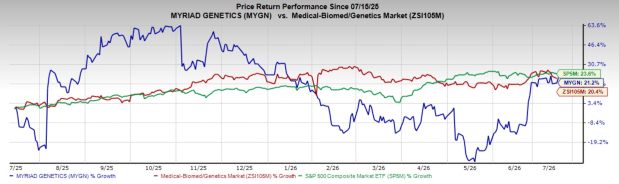

Over the past year, this Zacks Rank #3 (Hold) company’s shares have risen 21.2% compared with the industry’s 20.4% growth and the S&P 500’s gain of 23.6%.

The renowned genetic testing and precision medicine company has a market capitalization of $553.5 million. The company’s earnings yield of 0.1% remains well ahead of the industry’s -14.4% yield. MYGN’s earnings surpassed estimates in three of the trailing four quarters and missed on one occasion, delivering an average surprise of 237.5%.

Tailwinds for MYGN Stock

Product Launches and Upgrades: Myriad Genetics continues to refresh its menu with new panels, regulatory progress and clinical data that can improve utility and reduce provider friction. After expanding the MyRisk panel to 63 genes across more than 11 cancer types, the company launched additional disease-specific panels in the first quarter of 2026. Myriad Genetics also enhanced the Foresight carrier screen by adding genes that make the offering compliant with American College of Medical Genetics and Genomics recommendations. Meanwhile, Prequel is positioned to provide results earlier in pregnancy.

In March, Myriad Genetics initiated a limited launch of Precise MRD for breast cancer patients and stated early customer feedback has been positive as community oncology workflows develop. In tumor profiling, the company received FDA approval for MyChoice CDx as a companion diagnostic for Zejula in advanced ovarian cancer, which can support broader guideline use. In prostate cancer, management expects to launch its AI-enhanced Prolaris test in June 2026.

Image Source: Zacks Investment Research

Renewed Strategic Priorities: Myriad Genetics continues to execute its Cancer Care Continuum strategy, using a dedicated hereditary cancer sales force and workflow programs to drive adoption. In the first quarter of 2026, overall Cancer Care Continuum volumes rose 13% year over year, with MyRisk growing 10% in the affected population and 16% in the unaffected population compared with the year-ago quarter. These trends supported 2% year-over-year revenue growth on stable total testing volumes.

Mental Health remains an important pillar, with GeneSight volumes up 7% year over year in the first quarter and ordering clinicians exceeding 39,000. Management also highlighted improved reimbursement trends and payer coverage in GeneSight, aided by biomarker legislation and revenue cycle optimization. While Prenatal volumes declined 12% year over year, Myriad Genetics is working on reactivating accounts, expanding access and preparing for the FirstGene launch to support a return to growth in the second half of 2026.

Sound Solvency With Slight Leverage: Myriad Genetics exited the first quarter of 2026 with $124.4 million of cash and cash equivalents, down from $149.6 million as of Dec. 31, 2025. This reflects typical first-quarter cash burn and increased commercial investment. Long-term debt was $120.3 million at quarter-end, broadly consistent with year-end 2025. Management noted access to $199 million in capital, which provides the flexibility to fund planned launches while maintaining financial discipline.

What Concerns MYGN Stock?

GeneSight Coverage End Risks Revenues: Coverage decisions remain a key swing factor for Myriad Genetics’ Mental Health franchise. While GeneSight test volume grew 7% year over year in the first quarter of 2026 and revenues increased 24% to $38.3 million on improved reimbursement trends, the business remains exposed to payor policy changes that can alter access, pricing and cash flow. The broader company revenue increase of 2% year over year still reflects a mix of offsets across categories. Any renewed coverage tightening could limit operating leverage as Myriad Genetics invests in launches.

Macroeconomic Pressures: Myriad Genetics operates across multiple reimbursement regimes and faces ongoing cost exposure in labor, laboratory supplies and commercial execution. Management expects gross margins to fluctuate quarter to quarter in 2026 based on product mix and pricing trends, even as adjusted gross margin guidance remains 68% to 69%. Tariff-related input costs and inflation can be difficult to pass through in diagnostic testing, and a slower spending environment at provider offices could extend the time needed to rebuild Prenatal Health volumes after recent ordering disruption and account reactivation efforts.

MYGN Stock Estimate Trend

In the past 30 days, the Zacks Consensus Estimate for the company’s 2026 earnings per share (EPS) has remained constant at 1 cent.

The Zacks Consensus Estimate for 2026 revenues is pegged at $859.2 million, suggesting a 4.2% increase from the year-ago reported number.

Top MedTech Stocks

Some better-ranked stocks in the broader medical space are Phibro Animal Health PAHC, Align Technology ALGN and Integra LifeSciences IART.

Phibro Animal Health has an earnings yield of 10.1% compared with the industry’s 3% yield. Its earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 16.3%. PAHC shares have rallied 8.1% against the industry’s 27.9% decline over the past year.

PAHC carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Align Technology, carrying a Zacks Rank #2, has an estimated long-term earnings growth rate of 10.3% compared with the industry’s 5.5% growth. Shares of the company have dipped 7.4% against the industry’s 11.7% growth. ALGN’s earnings outpaced estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 7.8%.

Integra LifeSciences, carrying a Zacks Rank #2, has an earnings yield of 13.7% against the industry’s negative 3% yield. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 16.7%. IART shares have rallied 56.7% against the industry’s 5.3% decline over the past year.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Myriad Genetics, Inc. (MYGN): Free Stock Analysis Report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

Integra LifeSciences Holdings Corporation (IART): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).