Vicor VICR sits in a part of the AI build-out that is becoming harder to ignore. Faster processors matter, but dense computing also raises the importance of power conversion, current density and heat management.

That puts Vicor’s architecture story close to the hardware bottlenecks shaping data centers. The company is not just selling components; it is trying to make power delivery a strategic part of AI system design.

Why AI Chips Need More From Vicor

Higher processor power density makes power delivery a more critical design constraint. Vicor’s Advanced Products are concentrated in data-center and hyperscaler applications, where AI accelerators, graphics processing units and custom application-specific integrated circuits need compact, efficient power systems.

The company’s Factorized Power Architecture, Vertical Power Delivery and Modular Current Multiplier technologies are positioned around higher efficiency, greater power density and lower thermal losses than conventional power solutions.

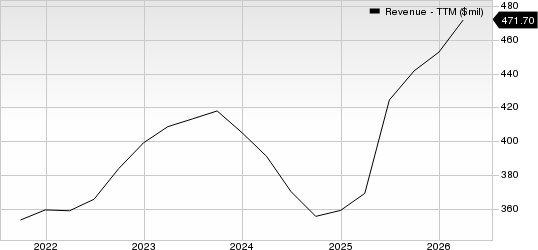

VICR’s Mix Shows the Trend in Action

Vicor’s mix already reflects this demand shift. Advanced Products, including royalty revenues, rose from 55.3% of total revenues in 2023 to 61% in 2025 and represented 57.5% of revenues in the first quarter of 2026.

Vicor Corporation Revenue (TTM)

Vicor Corporation revenue-ttm | Vicor Corporation Quote

First-quarter results showed the same direction. Advanced Products revenues increased 3.7% sequentially to $64.9 million, while royalty revenues rose 39.1% year over year to $14.97 million. Management also cited strong bookings across high-performance computing, industrial and aerospace and defense markets, with book-to-bill above 2.0.

Vicor’s one-year backlog reached $300.6 million in the first quarter of 2026, up 70% sequentially, and management described near-term capacity as essentially sold out.

Vicor is responding at its first chip fabrication facility. It now believes Fab 1 can support an annual revenue run rate of at least $1.5 billion, up from the prior target of roughly $1 billion, helped by cycle-time reductions, debottlenecking and moving selected process steps to a nearby Vicor-controlled site.

Vicor’s Licensing Trend Could Matter More

Licensing is becoming more than a secondary revenue stream. Royalty revenues were about $15 million in the first quarter of 2026, and 2026 revenue guidance of nearly $570 million assumes royalty revenues rise only somewhat under existing agreements.

That creates business-model leverage if more agreements are signed. At the same time, earnings quality can be more sensitive to legal costs and enforcement timing, since operating expenses increased 4% sequentially to $45.5 million in the first quarter, partly due to higher legal spending tied to intellectual-property enforcement.

What This Means for VICR Investors

For investors, VICR offers exposure to a specific AI infrastructure constraint rather than broad semiconductor demand alone. The company’s 2026 outlook calls for nearly $570 million in revenues, supported by AI-driven demand and capacity expansion efforts.

VICR shares have jumped a whopping 137.8% year to date (YTD), outperforming the Zacks Computer & Technology sector’s return of 15.8%. The company has outperformed competitors, including Monolithic Power MPWR, Analog Devices ADI and Texas Instruments TXN over the same timeframe. Shares of Monolithic Power, Analog Devices and Texas Instruments have appreciated 49.2%, 44.1% and 73.6%, respectively, YTD.

The risk is execution. The second three-dimensional interconnect line is expected to be installed between the third quarter and the fourth quarter of 2026, but it is not expected to contribute meaningfully until late 2026 and beyond. That leaves shipments, customer ramps and royalties as key variables.

Conclusion

The bottom line is that Vicor’s story fits an AI supply chain where power architecture is becoming more strategic. Demand and backlog support the operating case, but valuation leaves less room for disappointment after a large rerating.

VICR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vicor Corporation (VICR): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).