EchoStar Gearing Up to Report Q4 Earnings: Here's What to Expect

EchoStar Corporation SATS will release results for the fourth quarter of 2025 on March 2.

The Zacks Consensus Estimate for fourth-quarter loss has been unchanged in the past 60 days at 81 cents per share. The consensus mark implies a 165.3% wider loss from the year-ago actual. The Zacks Consensus Estimate for revenues is pegged at $3.74 billion, indicating a decline of 5.7% from the year-ago actual.

EchoStar has an impressive earnings surprise history. The company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 122.7%.

Image Source: Zacks Investment Research

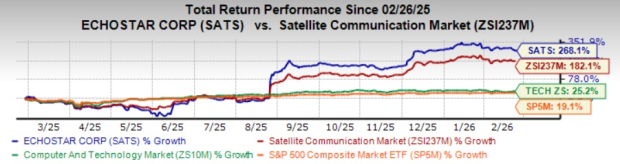

SATS stock has surged 268.1% in the past year compared with the Computer-Software industry’s growth of 182.1%. The S&P 500 composite and the Zacks Computer and Technology sector have risen 19.1% and 25.2%, respectively, in the same time frame.

Factors to Note Ahead of SATS’ Q4 Results

EchoStar is gaining from its transition away from a capital-intensive wireless buildout toward a more capital-light structure, as declining construction activity is expected to materially reduce fixed costs and shift the wireless segment toward a more variable, usage-based expense model, improving financial flexibility. Boost Mobile remains central to this evolution through its hybrid MVNO agreement with AT&T, which better aligns network costs with usage, while planned satellite-to-phone capabilities with SpaceX and AWS-3 spectrum transactions slated for 2026 and 2027 are expected to support differentiation and generate capital for long-term strategic initiatives.

The company’s Wireless segment, led by Boost Mobile, generated approximately $939 million in third-quarter revenue. Performance was supported by solid subscriber growth, better customer retention and a richer mix of higher-priced plans and value-added services, driving a 2.6% year-over-year increase in ARPU and maintaining the highest prepaid ARPU in the industry. Momentum in ARPU is likely to have supported revenue performance in the to-be-reported quarter. The Zacks Consensus Estimate for revenues from Wireless segment is pegged at $982 million for the fourth quarter.

The company announced an amended definitive agreement with SpaceX, expanding on its September deal to sell its unpaired AWS-3 spectrum license for about $2.6 billion in SpaceX stock. Upon closing, the transactions are expected to provide sufficient capital to support ongoing operations and pursue new growth opportunities, broadening the company’s strategic focus.

Also, EchoStar is benefiting from the accelerating demand for satellite-based connectivity as LEO and hybrid satellite architectures gain traction and enterprises seek dependable networks to support cloud adoption, digital transformation and remote operations. Rising needs for broadband access in rural markets, government programs aimed at bridging the digital divide and expanding mobility applications are creating tailwinds for Broadband & Satellite Services segment (primarily includes the Hughes enterprise and consumer portfolio of brands). In Hughes, enterprise revenue is becoming a larger contributor, with management indicating that enterprise services are expected to exceed 50% of segment revenue next year.

EchoStar Corporation Price and Consensus

EchoStar Corporation price-consensus-chart | EchoStar Corporation Quote

Recently, EchoStar announced that Hughes is strengthening its position in next-generation satellite communications with the launch of a new portfolio of ruggedized LEO terminals certified for Comms-on-the-Pause (COTP) service.

However, the Broadband and Satellite Services segment reported third-quarter total revenue of $346 million, down 10.6% year over year due to lower broadband service sales and weaker enterprise hardware demand. The Zacks Consensus Estimate for revenues from the Broadband & Satellite Services segment is pegged at $377 million for the fourth quarter.

Moreover, the company continues to face litigation with at least one tower company, and discussions with regulators are ongoing regarding network-related obligations. On the last earnings call, management also highlighted potential tax liabilities and decommissioning costs that could be substantial, depending on structuring outcomes. This remains concerning.

What Does Our Model Unveil for SATS?

Our proven model does not predict an earnings beat for EchoStar this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat. This is not the case here.

EchoStar has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Stocks With the Favorable Combination

Here are a few companies worth considering, as our model indicates that they possess the right combination to exceed earnings expectations in their upcoming releases:

Sweetgreen, Inc. SG currently has an Earnings ESP of +7.47% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for revenues is pegged at $159.7 million and a loss of 31 cents per share, respectively. SG is slated to report fourth-quarter 2025 results on Feb. 26.

Monster Beverage Corporation MNST currently has an Earnings ESP of +5.02% and a Zacks Rank #3.

The Zacks Consensus Estimate for revenues and earnings is pegged at $2.05 billion and 49 cents per share, respectively. MNST is scheduled to report fourth-quarter 2025 results on Feb. 26.

MongoDB, Inc. MDB has an Earnings ESP of +0.05% and a Zacks Rank #1 at present.

The Zacks Consensus Estimate for revenues and earnings is pegged at $668.2 million and $1.47 per share, respectively. MongoDB is slated to report fourth-quarter fiscal 2026 results on March 2.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EchoStar Corporation (SATS): Free Stock Analysis Report

Monster Beverage Corporation (MNST): Free Stock Analysis Report

MongoDB, Inc. (MDB): Free Stock Analysis Report

Sweetgreen, Inc. (SG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).