Ondas Inc. ONDS will release results for the fourth quarter of 2025 on March 25, 2026.

ONDS’ earnings beat the Zacks Consensus Estimate in the last quarter while missing in the previous three quarters, with an average negative surprise of 21.16%.

Let us see how ONDS is expected to fare in terms of revenues and earnings this time.

The Zacks Consensus Estimate for the fourth-quarter 2025 bottom line stands at a loss of 6 cents, unchanged in the past 30 days. The same for revenues is pegged at $28 million, indicating a 578% jump from the year-ago actual.

Ondas Holdings Inc. Price and EPS Surprise

Ondas Holdings Inc. price-eps-surprise | Ondas Holdings Inc. Quote

Management has twice updated guidance for the fourth quarter, underscoring strong business momentum, especially in its Ondas Autonomous Systems (“OAS”) division.

Fourth-quarter 2025 revenues are now expected to be between $29.1 million and $30.1 million, compared with the prior target (announced at investor day in January) of $27 million to $29 million. Management had originally guided for revenues of more than $15 million during the third quarter earnings call.

Full year, revenues are anticipated to be $49.7 million to $50.7 million, increased from the earlier targeted range of $47.6 million to $49.6 million. Management had originally guided for revenues of at least $36 million

Earnings Whispers for ONDS

Our proven model does not predict an earnings beat for Ondas this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not the case here.

ONDS currently has a Zacks Rank #3 and an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping ONDS Q4 Results

Ondas entered 2026 following a transformational year marked by a pivot to autonomous systems, aggressive portfolio expansion and platform scaling. Management remains focused on driving OAS from a collection of specialized autonomous drone systems into a multi-domain global autonomy platform.

Through the OAS unit, the company is expanding its footprint with new defense and homeland security customers across Europe, the Middle East and the United States. Growing traction for both its Optimus System and Iron Drone Radar system bodes well.

It recently announced a merger agreement with Mistral Inc. Mistral is a U.S.-based defense prime contractor that has supported U.S. military, federal and public safety programs over the past few decades. Under the agreement, Mistral will merge with a subsidiary of Ondas while continuing to manage its existing contracts. The merger is anticipated to conclude in the second quarter of 2026.

Mistral is a prime contractor on U.S. Army and USSOCOM uncrewed and autonomous platforms procurement vehicles. Mistral brings U.S.-based manufacturing, assembly, integration and quality assurance capabilities to Ondas’ operations, supporting program execution and compliance with the country’s defense sourcing requirements. Management highlighted that the transaction “aligns” with the company’s broader strategy to expand its footprint in U.S. defense procurement.

Counter-UAS (C-UAS) remains one of the most compelling near-term growth drivers. Increasing usage of low-cost drones amid simmering geopolitical tensions are likely to have driven demand for C-UAS. At the investor day, management noted that it was seeing active deployments in airport environments and critical infrastructure protection across Europe, with more than $60 million in orders in 2025.

Image Source: Zacks Investment Research

In March, ONDS secured multiple orders totaling nearly $6 million for the counter-drone systems (including Sentrycs cyber-RF C-UAS) from existing defense and homeland security customers in the Middle East and other regions, amid the current regional conflict.

To complement organic expansion, ONDS is focusing on M&A to strengthen the portfolio offerings and broaden its reach across multiple domains, including unmanned ground systems, robotics, fiber-optic communications and subsurface intelligence and demining robotics. In the past year, it has acquired Sentrycs, Apeiro Motion and Zickel, among others. This is likely to have aided fourth-quarter revenue performance.

Recent acquisitions include Roboteam, which specializes in multi-mission tactical ground robotics, as well as Rotron Aero, a UK-based developer of advanced UAS and long-range autonomous platforms. It also acquired BIRD Aerosystems and INDO Earth Moving Ltd.

A strong balance sheet is a key enabler of the M&A strategy. ONDS’ pro forma cash balance exceeded $1.5 billion as of Dec. 31, 2025, adjusted for its earlier completed equity offering of approximately $1 billion, providing substantial financial flexibility.

Nonetheless, heavy dependence on the OAS division for revenue growth in the increasingly crowded drone space is a concern. Competition has intensified with drone companies such as Red Cat Holdings RCAT, AeroVironment AVAV and Unusual Machines UMAC vying to capture a larger share.

Image Source: Zacks Investment Research

If a single large customer delays, reduces or cancels, revenues would decline materially. Moreover, revenues from Ondas Networks in the near term are expected to remain modest, with meaningful commercialization likely beginning in 2026.

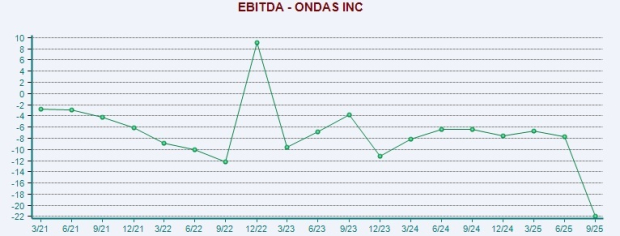

ONDS is in the middle of a massive transition and already incurring sizable expenses as it invests heavily in research and development and commercialization efforts. These moves strengthen long-term competitive moat, but amplify short-term financial pressure. The company expects the 2025 adjusted EBITDA loss to be between $32.4 million and $32.9 million. Net loss is projected to be between $52.8 million and $53.3 million.

For the fourth quarter, Ondas expects to incur a net loss of $20.9 million to $20.4 million and adjusted EBITDA between a loss of $11.4 million and $10.9 million.

Further, so many acquisitions in such a short period of time can create integration overload risk. Although these buyouts provide undeniable technological depth, investors must watch closely for an increase in expenses and execution risks.

Image Source: Zacks Investment Research

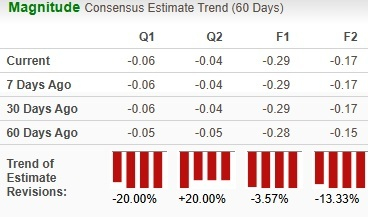

Analysts have revised their earnings estimates downwards for 2025.

ONDS Stock Performance vs. Peers

ONDS’ shares have surged 48.1% over the past six months, outperforming the Wireless-National industry’s decline of 3.5%. The S&P 500 composite and the Zacks Computer and Technology sector have edged down 0.4% and 2.4%, respectively, in the same time frame.

Image Source: Zacks Investment Research

Red Cat and Unusual Machines stocks are up 33.7% and 29.6%, respectively, over the same time frame, while AeroVironment is down 26.6%.

Key Valuation Metric for ONDS

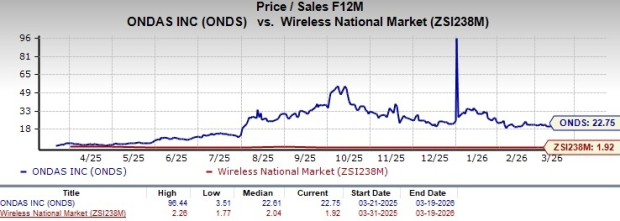

ONDS stock is trading at a substantial premium, with a forward 12-month price/sales of 22.75X compared with the industry’s 1.92X.

Image Source: Zacks Investment Research

In comparison, AVAV, RCAT and UMAC trade at multiples of 4.84X, 9.95X and 30.12X, respectively.

How to Approach ONDS Before Q4 Earnings Release

Ondas’ operational momentum, underpinned by surging OAS revenues, an expanding $65.3 million backlog (Investor Day 2026) and higher penetration across defense and homeland security markets, bodes well.

However, its premium valuation, widening losses and risks tied to rapid scaling and acquisitions warrant a cautious approach in the near term. The premium valuation exposes investors to sharp volatility and heightens downside risk in the near to medium term.

Given the balance of strong growth prospects and near-term challenges, investors may be better off holding the stock for now, while new investors need to wait for a favorable entry point.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AeroVironment, Inc. (AVAV): Free Stock Analysis Report

Ondas Holdings Inc. (ONDS): Free Stock Analysis Report

Red Cat Holdings, Inc. (RCAT): Free Stock Analysis Report

Unusual Machines, Inc. (UMAC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).