Palantir Technologies Inc. PLTR is benefiting from its AI strategy, driven by Foundry, Gotham and Artificial Intelligence Platform (AIP). The company’s software is used for several purposes across different business functions and organizational levels, including automotive manufacturing workers, utility operations analysts, oil and gas technicians, and operators, thereby enabling real-time insights and operational efficiency.

PLTR has a Growth Score of A. This style score condenses key financial metrics to reflect a fair sense of the quality and sustainability of its growth.

It also has an encouraging earnings surprise history. Its earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and matched once, delivering an average beat of 11.6%.

The company’s first-quarter fiscal 2026 earnings are expected to increase 123.1% year over year. The company’s fiscal 2026 and 2027 earnings are projected to rise 74.7% and 44.6%, respectively. Revenues are anticipated to grow 61.3% in fiscal 2026 and 39.8% in fiscal 2027.

Factors That Bode Well for PLTR

PLTR’s top line benefits from its strong, comprehensive AI strategy and multiple platforms, which promote AI adoption across both government and commercial sectors. The Gotham platform allows users to find patterns deep within the datasets, like signals from intelligence sources and reports from confidential informants, while bridging the gap between analysts and operators to respond efficiently to the risks identified within the platform.

The Foundry platform transforms a company's operations by creating a central operating system for its information, while the AIP allows responsible AI advantage across the enterprise by using the core components built to activate large language models and other AI within any organization, efficiently.

PLTR’s AIP is the most sought-after solution among organizations, enabling them to process large datasets and derive real-time insights. This service is especially valuable in sectors requiring extensive data integration, such as defense, healthcare, finance and intelligence, where operational efficiency and decision-making speed are critical. A utility company’s annual contract value (ACV) expanded from $7 million in the first quarter of 2025 to $31 million by year-end, while an energy company’s ACV expanded from $4 million to more than $20 million during the same time frame.

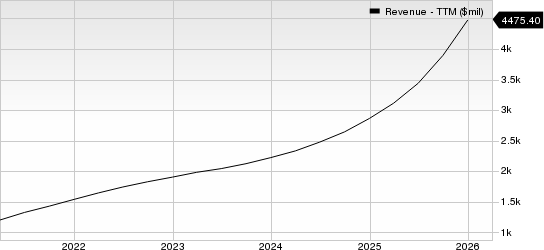

Palantir Technologies Inc. Revenue (TTM)

Palantir Technologies Inc. revenue-ttm | Palantir Technologies Inc. Quote

The company’s modular sales approach also drives new client generation, allowing them to purchase specific product components instead of committing to the full platform upfront and incorporating usage-based pricing, which lowers the entry barrier.

PLTR’s strong balance sheet, with cash and equivalents worth $7.2 billion and a current ratio of 7.11 as of Dec. 31, 2025, suggests that the company is well-positioned to meet its short-term obligations.

Risks to Watch

PLTR has never declared and currently has no plans to pay cash dividends. This may discourage cash dividend-seeking investors, leaving them with potential returns only from share price appreciation. Since share price appreciation is variable, dividend-focused investors may hesitate to bet on it.

The stock is also currently trading at a significantly elevated valuation with a forward price-to-earnings ratio of 94.54X, far exceeding the industry average of 24.19X and a forward price-to-sales ratio of 41.51X, compared with the industry benchmark of 3.43X. Historically, such high valuations have often preceded substantial stock price declines.

Zacks Rank & Stocks to Consider

PLTR currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

A couple of better-ranked stocks in the industry are Guidewire GWRE and HubSpot, Inc. HUBS.

Guidewire sports a Zacks Rank #1 at present. It has a long-term earnings growth expectation of 12.6%.

GWRE beat the Zacks Consensus Estimate in three of the last four reported quarters and matched once, with the earnings surprise being 44.7%, on average.

HubSpot also sports a Zacks Rank of 1 at present. It has a long-term earnings growth expectation of 18.6%.

HUBS delivered a trailing four-quarter earnings surprise of 3%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Guidewire Software, Inc. (GWRE): Free Stock Analysis Report

HubSpot, Inc. (HUBS): Free Stock Analysis Report

Palantir Technologies Inc. (PLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).