Lamb Weston Holdings, Inc. LW reported solid third-quarter fiscal 2026 results, wherein both top and bottom lines beat the Zacks Consensus Estimate. While net sales increased, earnings decreased from the year-ago period’s actuals.

LW’s adjusted earnings were 72 cents, down 37% year over year, due to reduced adjusted gross profit and elevated adjusted selling, general and administrative (SG&A), partially offset by reduced income tax expense. However, the bottom line beats the Zacks Consensus Estimate of 61 cents.

Lamb Weston Price, Consensus and EPS Surprise

Lamb Weston price-consensus-eps-surprise-chart | Lamb Weston Quote

Net sales amounted to $1,564.8 million, beating the Zacks Consensus Estimate of $1,485 million. The top line increased $44.3 million or 3% year over year.

LW’s Quarterly Results: Key Metrics & Insights

On a constant-currency basis, sales were flat, as solid 7% volume growth was outweighed by a 7% drop in price/mix. Volume growth was driven by North America customer wins, share gains and retention. The decrease in price/mix reflects continued customer support through pricing and trade actions, as well as a shift in consumer demand toward value-oriented channels and brands. This includes increased sales to chain customers, which typically carry lower pricing. Our model suggested a volume increase of 3.4% in the quarter.

Adjusted gross profit fell $92.9 million from the prior year, landing at $327.5 million, with weaker price/mix serving as the main drag and a $32.5 million pre-tax charge related to the write-off of excess raw potatoes in the International segment, due to lower-than-expected sales volumes amid weak market demand.

Adjusted SG&A expenses rose by $9.4 million year over year to $157.4 million. Although ongoing cost savings initiatives delivered benefits, these were more than offset by normalized performance-based compensation and benefit accruals, as well as $12.7 million in write-offs of capitalized costs related to discontinued projects.

Adjusted EBITDA decreased $101.3 million year over year, reaching $271.7 million. This decline was due to reduced adjusted gross profit and elevated adjusted SG&A.

LW Provides Q3 Insights by Segment

Net sales for the North America segment, which covers customers in the United States, Canada and Mexico, increased 5% to $1,035 million compared with the prior-year quarter. Volume rose 12%, driven by customer contract wins, share gains and continued growth.

The segment’s price/mix declined 7%, reflecting ongoing price and trade support for customers, along with an unfavorable mix shift toward faster-growing chain customers and private-label products, which typically carry lower pricing.

The North America segment adjusted EBITDA declined by $12.8 million to $289.8 million. Higher volumes, reduced manufacturing costs per pound and lower adjusted SG&A, supported by cost savings initiatives and improved operating efficiencies, were more than offset by continued price and trade support and unfavorable mix.

Net sales for the International segment, which includes all customers outside North America, declined 1% to $529.8 million, including a favorable $43.7 million impact from foreign currency. On a constant currency basis, net sales decreased 9%. Volume declined 2%, reflecting softer demand in key international markets.

The segment’s price/mix declined 7% at constant currency, primarily due to continued pricing and trade actions to support customers, along with an unfavorable mix toward lower-priced geographies and products.

International segment adjusted EBITDA fell by $75.6 million year over year to $18.5 million. The decline was mainly caused by reduced sales and higher manufacturing costs per pound, including a $32.5 million pre-tax charge related to the write-off of excess raw potatoes and increased fixed factory burden from underutilized international production facilities. These elevated costs were partially offset by benefits from cost savings initiatives.

Lamb Weston’s Financial Health Snapshot

The company ended the quarter with cash and cash equivalents of $57.5 million, long-term debt and financing obligations (excluding the current portion) of $3,642.9 million and total shareholders’ equity of $1,827.1 million.

Lamb Weston generated $595.6 million as net cash from operating activities for the 39 weeks ending Feb. 22, 2026, wherein capital expenditures amounted to $256.5 million.

In the third quarter of fiscal 2026, Lamb Weston returned $51.4 million to its shareholders through cash dividends.

On March 31, management declared a quarterly dividend of 38 cents per share, payable on June 5, to its shareholders of record as of May 8, 2026.

What to Expect From LW in FY26?

The company now expects net sales in the range of $6.45 billion to $6.55 billion, compared with its prior outlook of $6.35 billion to $6.55 billion.

Adjusted EBITDA is projected between $1.08 billion and $1.14 billion, narrowed from the previous range of $1.00 billion to $1.20 billion

Capital expenditures are now anticipated to be approximately $400 million, down from the earlier outlook of around $500 million.

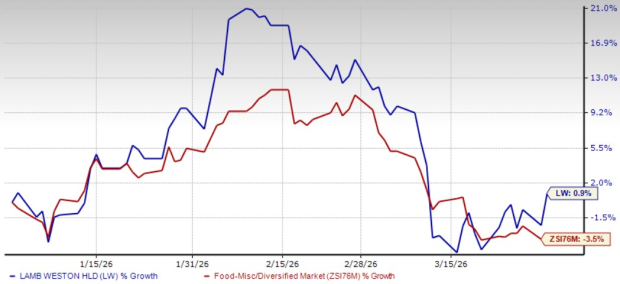

LW’s Share Price Performance

Shares of this Zacks Rank #3 (Hold) company have gained 0.9% in the past three months against the industry’s 3.5% decline.

Image Source: Zacks Investment Research

Stocks to Consider

Mama's Creations, Inc. MAMA manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 39.9% and 44.4%, respectively, from the year-ago figures. Mama's Creations delivered a trailing four-quarter earnings surprise of 133.3%, on average.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It flaunts a Zacks Rank #1 at present. HSY delivered a trailing four-quarter earnings surprise of 17.2%, on average.

The Zacks Consensus Estimate for Hershey’s current financial-year sales and earnings indicates growth of 4.8% and 30.1%, respectively, from the prior-year reported levels.

US Foods Holding Corp. USFD engages in the marketing, sale and distribution of fresh, frozen and dry food and non-food products to foodservice customers in the United States. USFD currently carries a Zacks Rank #2 (Buy). US Foods Holding delivered a trailing four-quarter earnings surprise of 2.2%, on average.

The Zacks Consensus Estimate for US Foods Holding’s current fiscal-year sales and earnings implies growth of 5.4% and 20.9%, respectively, from the year-ago figures.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hershey Company (The) (HSY): Free Stock Analysis Report

US Foods Holding Corp. (USFD): Free Stock Analysis Report

Lamb Weston (LW): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).