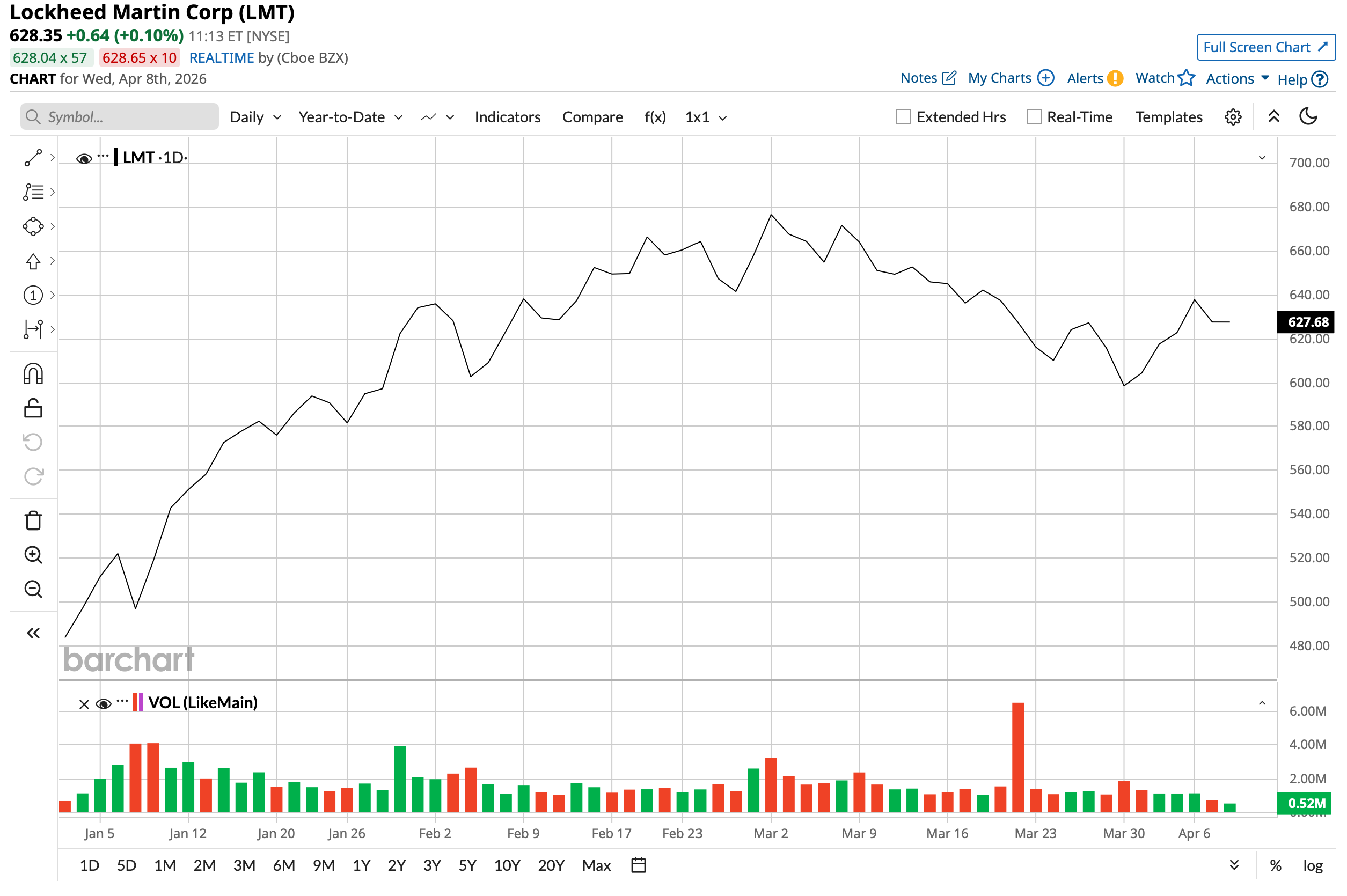

As the war in the Middle East rages on, shareholders of legacy defense major Lockheed Martin (LMT) should be a happy lot. The stock is up almost 30% on a year-to-date (YTD) basis and looks set for further appreciation as mixed signals continue to emerge about the cessation of the ongoing conflict. Thus, even amid talks of a ceasefire, prudent investors should continue to hold on to the shares of a critical defense player like Lockheed Martin.

www.barchart.com

www.barchart.com Why? Apart from being a major bulwark for the U.S. against any possible hostilities due to their dependable munitions, the LMT stock also offers a dividend yield of 2.22%. This makes its shares a play on stable income and growth for investors, where both are at a premium in this volatile market.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

About Lockheed Martin

Founded in 1995 but tracing its origins way back to 1912, Lockheed Martin is a global aerospace, defense, and security company involved in building fighter jets, precision weapons, and missile systems, among others. Its market cap currently stands at $144.7 billion, and it has been working closely with the US government for decades, positioning itself as a reliable partner.

While its F-35 Lightning II remains its flagship product used by the U.S. and NATO allies alike, the company's PAC-3 and THAAD missile systems also have heavy demand across the various geopolitical hotspots around the world.

Coming to its shareholder activities, the company is on the brink of becoming a “Dividend Aristocrat,” having raised dividends consecutively for the past 23 years.

Yet, are these reasons convincing enough to buy the LMT stock? If not, then here are some more.

Superb Q4

Lockheed Martin's earnings may have missed the Street estimates by a whisker, yet the results were far from disappointing, as a record backlog ($193.6 billion, +10% YoY) of orders and strong revenue growth were the hallmarks of a robust quarter.

Q4 2025 saw the company reporting revenues of $20.3 billion, up 9.1% from the previous year. Further, earnings jumped to $5.80 per share from just $2.22 per share in the year-ago period, as it just missed the consensus estimate of $5.80 per share. Notably, over the past nine quarters, LMT's earnings have missed estimates on just three occasions.

The past 10 years have seen Lockheed Martin growing its revenue and earnings at CAGRs of 6.35% and 4.84%, respectively. Granted, it may not be the growth seen in the high-flying tech names, but investors should be mindful of the fact that it is a defense company with limited or close to no exposure to the consumer market.

Cash flow from operations and free cash flow both grew at a healthy pace when compared to the previous year, coming in at $3.2 billion and $2.8 billion compared to $1 billion and $441 million in the year-ago period, respectively. Overall, LMT closed 2025 with a cash balance of $4.1 billion, much higher than its short-term debt levels of $1.2 billion.

For 2026, the management has guided for revenues to be in the range of $77.5 billion and $80 billion, the midpoint of which would denote an annual growth rate of about 5%. Earnings expectations are between $29.35 and $30.25 per share. In the middle, this would imply a growth rate of about 39% on a YoY basis.

Meanwhile, even after such a sharp uptick this year, the LMT stock continues to trade at reasonable levels when compared to the sector median. Its forward P/E, P/S, and P/CF are 20.98, 1.83, and 16.31, while the sector medians are at 19.21, 1.75, and 15.07, respectively.

Lock in To Lockheed

Its impressive financials apart, Lockheed Martin distinguishes itself from peers primarily through its immense scale and unrivaled dominance in tactical aircraft. Unlike Boeing (BA), which divides its attention between commercial aviation, Lockheed operates as a deeply focused defense titan. The F-35 fighter jet program alone acts as an unparalleled moat while securing decades of guaranteed sustainment contracts. This flagship asset provides predictable cash flow visibility. Difficult for peers to easily replicate, this brings financial stability that uniquely positions the firm to confidently fund future dividends and share repurchases.

Meanwhile, while competitors like RTX (RTX), formerly Raytheon, excel in precision munitions and commercial jet engines, and L3Harris (LHX) dominates tactical communications, LMT often sits structurally above them as the prime systems integrator, essentially building the macro platforms that incorporate those various subsystem components. Moreover, to sharpen its competitive edge, the company is actively embedding AI capabilities across its physical and digital portfolio.

A standout example is the customized VISTA training jet, a modified F-16D, which executed over 17 hours of complex flight maneuvers controlled entirely by advanced AI agents. The firm is also deploying machine learning algorithms within its predictive maintenance software to anticipate component failures on military aircraft before they actually happen, which drastically reduces fleet downtime and significantly lowers operational costs for the Pentagon.

Peering into the future, shareholder value will largely stem from the highly classified Skunk Works division and its aggressive development of Collaborative Combat Aircraft. These unmanned autonomous drones will fly alongside human pilots in combat, representing a lucrative new growth vector as the military seeks to rapidly expand fleet capacity at a lower unit cost. Additionally, the firm is investing heavily in advanced strike capabilities, specifically the Mako multimission hypersonic missile designed to penetrate sophisticated enemy air defenses at speeds exceeding Mach 5. The space segment also offers substantial upside as the team develops advanced missile warning satellites and commercial lunar infrastructure.

Successfully transitioning these complex developmental programs into active production phases has the potential to trigger margin expansion and drive meaningful equity appreciation over the coming decade.

Analyst Opinion on LMT Stock

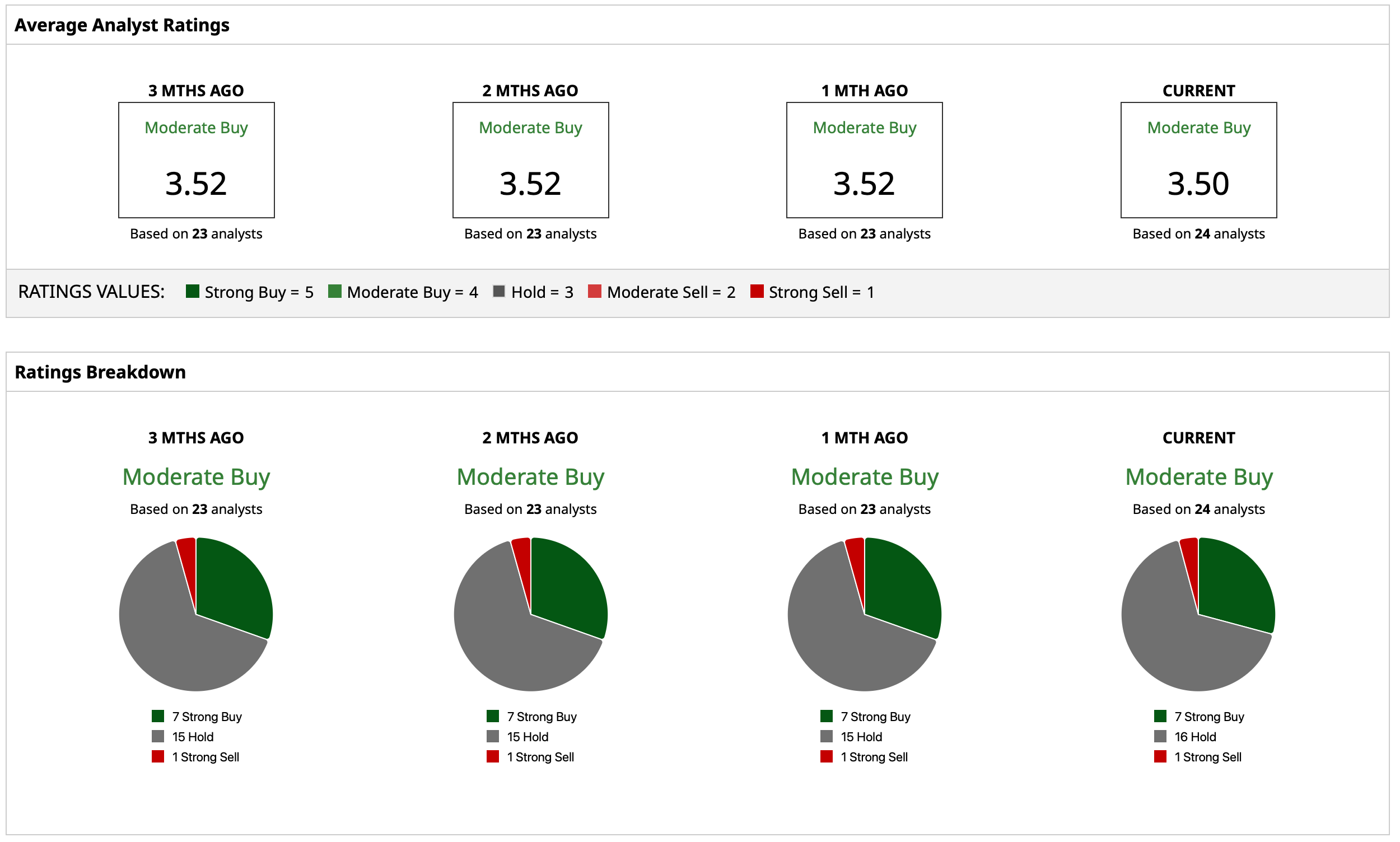

Thus, analysts have attributed to the LMT stock a consensus rating of “Moderate Buy” with a mean target price of $655.91, which denotes an upside potential of about 5% from current levels. Out of 24 analysts covering the stock, seven have a “Strong Buy” rating, 16 have a “Hold” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Lockheed Martin Stock Is Up 30% in 2026 and Yields 2%. Is It a Top Buy While the Iran War Drags On? Bank of America Warns That the Middle East Oil Shock Is Bad News for Carvana Stock. Should You Sell CVNA Now? Protect Your Profits Before It’s Too Late: The Options Strategy That Smart Investors Use Before a Drop Exxon Mobil Stock Threatens to Break Below Its 50-Day MA. Should You Buy the Dip?