E-commerce and technology giant Amazon.com (AMZN) has been navigating a volatile start to the year, caught between aggressive artificial intelligence (AI) spending plans and rising geopolitical tensions. The situation has become more complex as conflict in the Middle East intensified, with recent drone strikes damaging three Amazon Web Services (AWS) data centers in the UAE and Bahrain. At the same time, the escalation has disrupted the Strait of Hormuz, pushing oil prices higher and directly impacting Amazon’s logistics network.

As fuel costs surge, the company is now facing rising expenses to move packages, putting pressure on its e-commerce margins. To offset these costs, Amazon has announced a 3.5% fuel and logistics surcharge for third-party sellers in the U.S. and Canada. The company acknowledged that it had been absorbing higher fulfillment and logistics costs, but with expenses remaining elevated, it is now following other major carriers in passing part of that burden back to sellers through temporary surcharges.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Starting Apr. 17, the new fee will apply to Fulfillment by Amazon (FBA) orders in the U.S. and Canada, as well as remote fulfillment shipments from the U.S. into Canada, Mexico, and Brazil, broadening the impact across its seller ecosystem. And the ripple effect could be meaningful. The sellers would pass on higher costs to consumers, and prices for everyday goods on the platform may rise, potentially hurting Amazon’s e-commerce business just as the company ramps up spending on AI.

So, with rising costs, geopolitical risks, and pricing pressure now in play, here’s a closer look at the stock.

About Amazon Stock

Seattle-based Amazon may have started by reshaping online shopping, but its evolution into a broad-based technology powerhouse has been striking. What began as an e-commerce disruptor has steadily expanded into cloud computing, artificial intelligence, data centers, and digital media, placing Amazon at the center of how people shop, work, and consume content. Its presence in entertainment is equally significant.

Through platforms like Prime Video, Amazon Music, gaming, and Twitch, the company has built a meaningful position in the global streaming and digital content ecosystem. Meanwhile, AWS remains a critical pillar of the business, sitting at the heart of the cloud and AI boom by providing infrastructure that supports startups, enterprises, and large-scale organizations worldwide. Now, Amazon is pushing further into AI, increasing investments as it looks to deepen its role across the next wave of technological transformation.

With a market capitalization of roughly $2.3 trillion, Amazon remains one of the most dominant forces in tech, but its stock has seen a choppy ride in 2026. Shares are down 4.15% year-to-date (YTD), broadly in line with the 0.92% decline in the S&P 500 Index ($SPX), reflecting a more cautious tone across the market. Zooming out, the longer-term picture looks steadier. Over the past year, Amazon has delivered a 29.64% gain, closely tracking the broader market’s 36.13% return.

www.barchart.com

www.barchart.com Amazon’s Q4 Earnings Snapshot

Amazon delivered massive scale in its fiscal 2025 fourth-quarter results, released on Feb. 5, but the market’s reaction showed that even blockbuster numbers don’t always guarantee investor enthusiasm. The company reported a staggering $213.4 billion in revenue, up 14% year-over-year (YOY) and comfortably ahead of Wall Street’s $211.5 billion estimate. A key engine behind that growth was AWS, where revenue surged 24% to $35.6 billion, highlighting continued strength in cloud and AI-driven demand.

Other segments also contributed solidly to the top line. North America sales rose 10% to $127.1 billion, while the international business climbed 17% to $50.7 billion, underscoring Amazon’s ability to scale across geographies and business lines. On paper, it was a quarter that reflected the company’s immense operating reach and diversified growth drivers.

Yet, despite the strong revenue performance, the stock fell more than 5% in the sessions following the release. Investors appeared to focus on two key concerns. Slight earnings miss and rising capital intensity weighed on investor sentiment. Quarterly EPS came in at $1.95, up 4.8% YOY, but just shy of expectations of $1.98.

The bigger story, however, was the company’s forward-looking strategy. CEO Andy Jassy signaled a major step-up in AI infrastructure spending, guiding for approximately $200 billion in capital expenditures for 2026. While part of this investment will support core retail and non-AI operations, the bulk is aimed at expanding Amazon’s generative AI capabilities, including new data centers and custom silicon such as Trainium and Graviton.

These efforts are already gaining traction. Trainium and Graviton have surpassed a combined $10 billion annual revenue run rate, growing at a triple-digit pace YOY as demand for Amazon’s in-house chips accelerates.

Looking ahead, Amazon expects first-quarter 2026 revenue between $173.5 billion and $178.5 billion, representing 11% to 15% growth. Operating income is projected in the range of $16.5 billion to $21.5 billion, compared to $18.4 billion in the same quarter last year, signaling continued growth.

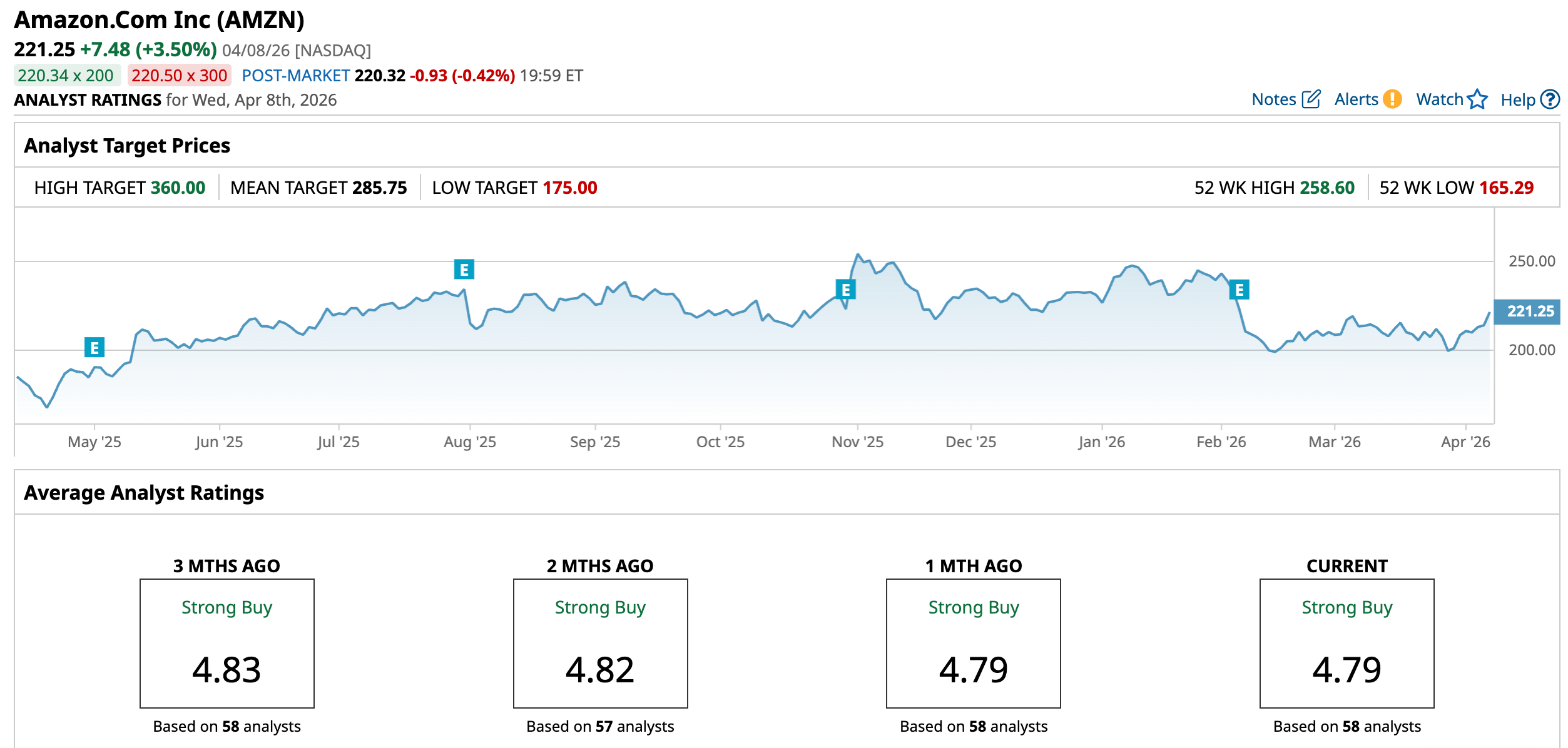

How Are Analysts Viewing Amazon Stock?

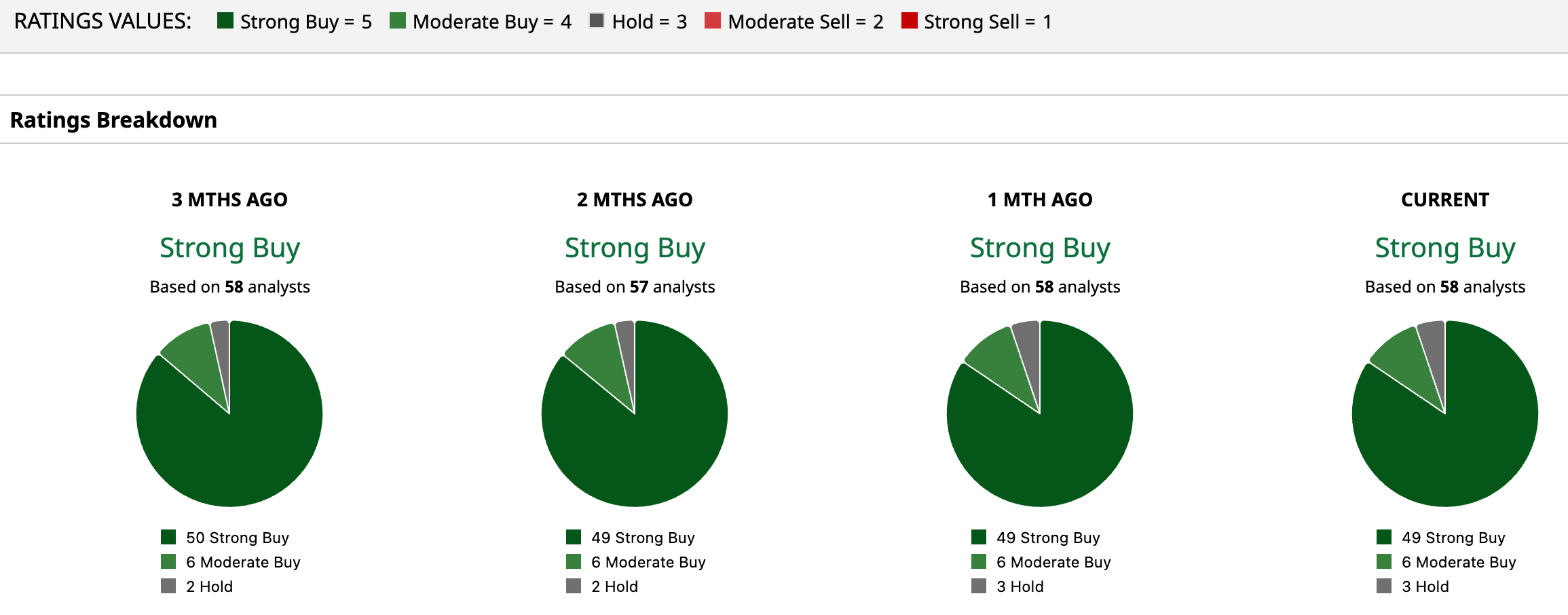

With Apr. 17 drawing closer and uncertainty still clouding the company’s near-term outlook, Wall Street’s conviction in Amazon remains firmly intact. The stock carries a “Strong Buy” consensus rating, reflecting broad optimism around its long-term growth story. Out of 58 analysts, an overwhelming 49 rate it a “Strong Buy,” with six issuing “Moderate Buy” and just three opting for “Hold,” a clear indication that bullish sentiment dominates the Street.

The upside case is equally compelling. The average price target of $285.75 points to a potential 29.2% gain, while the Street-high target of $360 suggests the stock could rally as much as 62.7% from current levels, highlighting strong confidence that Amazon’s AI and cloud-driven growth could power the next leg higher.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Should You Chase the Rally in Royal Caribbean Stock Today? Seaport Research Warns on AVGO Stock: Broadcom Is Confronting the ‘Limits of the Industry’ This S&P 500 Stock Is Up 814% in Just the Past Year Broadcom Is Making AI Chips with Google. Does That Make AVGO Stock a Buy Now?