Artificial intelligence (AI) may be reshaping the tech world, but in 2026, it’s also shaking confidence in software stocks. Despite the AI boom, the software industry has had a rough ride, especially after AI startup Anthropic rolled out its Claude Cowork plugins earlier this year. The launch sparked fresh fears that AI agents could disrupt traditional SaaS models by replacing, rather than enhancing, existing software platforms.

That uncertainty has weighed heavily on legacy names like Salesforce (CRM) and ServiceNow (NOW) both of which have seen double-digit declines so far this year as investors question their long-term relevance in an AI-driven world. But not everyone on Wall Street is convinced the threat is real. For instance, analysts at Wedbush believe the sell-off is overdone. After recent conversations with CIOs across the industry, the investment firm argues that fears of OpenAI or Anthropic evolving into full-scale enterprise software giants are a stretch.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Instead of replacing software platforms, AI is more likely to be embedded within them, driving new use cases, not destroying old ones. The firm believes the worst may already be behind for software stocks. In fact, Wedbush sees the recent pullback in Salesforce and ServiceNow as “disconnected’ from their long-term AI monetization potential. So, given this bullish outlook, is the current dip in CRM and NOW a buying opportunity for investors?

Stock #1: Salesforce

San Francisco-based Salesforce is the world’s leading customer relationship management (CRM) platform, built to help businesses strengthen and manage their customer relationships. Since its founding in 1999, Salesforce has been at the forefront of the shift to cloud-based software and continues to evolve as companies move into an AI-driven era of digital transformation.

A key part of that evolution is Agentforce, the company’s most ambitious AI initiative, which introduces autonomous AI agents designed to perform tasks for both employees and customers. By bringing together data from across an organization, Salesforce provides a unified, 360-degree view of each customer. Its broad suite of solutions, covering sales, service, marketing, commerce, and IT, enables businesses to operate more efficiently and stay aligned across functions.

Together, these capabilities reflect Salesforce’s push toward a more intelligent and streamlined approach to customer management in a rapidly changing digital landscape. Its ecosystem also includes widely used platforms such as Slack, Tableau, and MuleSoft. The company’s market capitalization currently stands at roughly $162.8 billion.

Shares of this software heavyweight have been under intense pressure as AI fears rattle sentiment. The stock has tumbled 36.74% over the past year and plunged another 36.68% in 2026, sharply underperforming the broader S&P 500 Index ($SPX), which surged 25% last year and is only marginally lower this year.

www.barchart.com

www.barchart.com While investors have been aggressively selling software stocks, Salesforce continues to deliver solid underlying performance. The company’s fiscal 2026 fourth-quarter results, released on Feb. 25, comfortably beat Wall Street expectations on both revenue and earnings. Salesforce reported revenue of $11.20 billion, up 12.1% year-over-year (YOY), marking its fastest growth rate in two years, and slightly ahead of the $11.17 billion consensus estimate.

Growth was supported by the successful integration of Informatica and a strong 13% increase in subscription and support revenue. Momentum was also evident in its forward-looking metrics. Current remaining performance obligation (cRPO), a key measure of contracted but yet-to-be-recognized revenue, rose 16% YOY to $35.1 billion, highlighting strong demand visibility.

On the profitability front, adjusted EPS surged 37.1% to $3.81, easily surpassing analysts’ expectations of $3.03 per share. The company also returned a substantial $14.3 billion to shareholders during the period, including $12.7 billion in share repurchases and $1.6 billion in dividends. A major highlight of the quarter was Agentforce, Salesforce’s autonomous AI platform, which continues to gain traction.

CEO Marc Benioff emphasized that Salesforce is evolving into the “operating system for the Agentic Enterprise.” Agentforce’s annual recurring revenue (ARR) climbed to $800 million, representing a sharp 169% YOY increase. Engagement levels were equally impressive, with more than 2.4 billion “Agentic Work Units” delivered and 19 trillion tokens processed during the period. Importantly, adoption appears to be deepening within Salesforce’s existing customer base, with 60% of bookings for Agentforce and Data 360 driven by expansions from current clients.

Looking ahead, the company struck a cautiously optimistic tone. For the first quarter of fiscal 2027, Salesforce expects revenue in the range of $11.03 billion to $11.08 billion and adjusted EPS between $3.11 and $3.13. It also reaffirmed its longer-term ambitions, updating its fiscal 2030 revenue target to $63 billion, signaling confidence in its AI-driven growth trajectory.

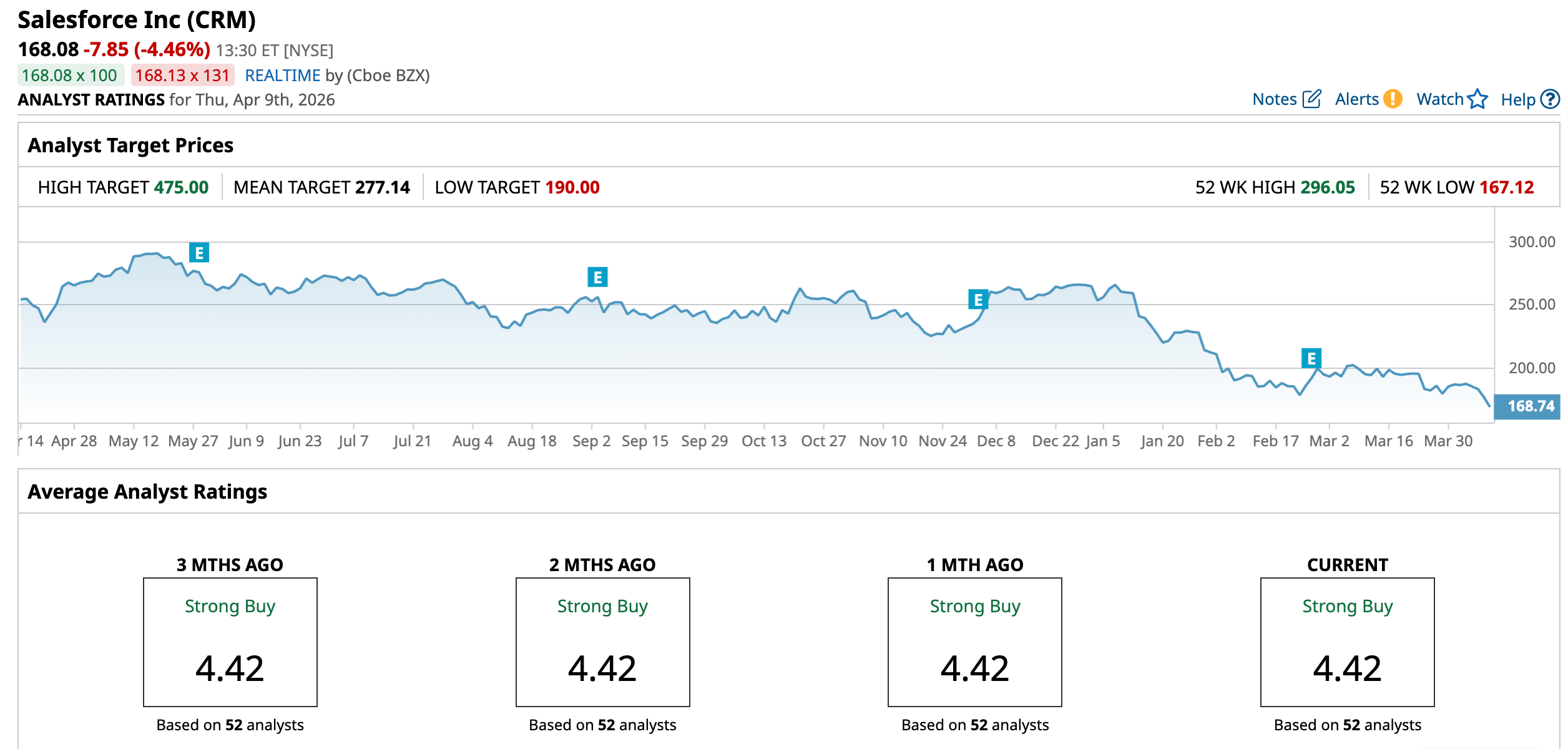

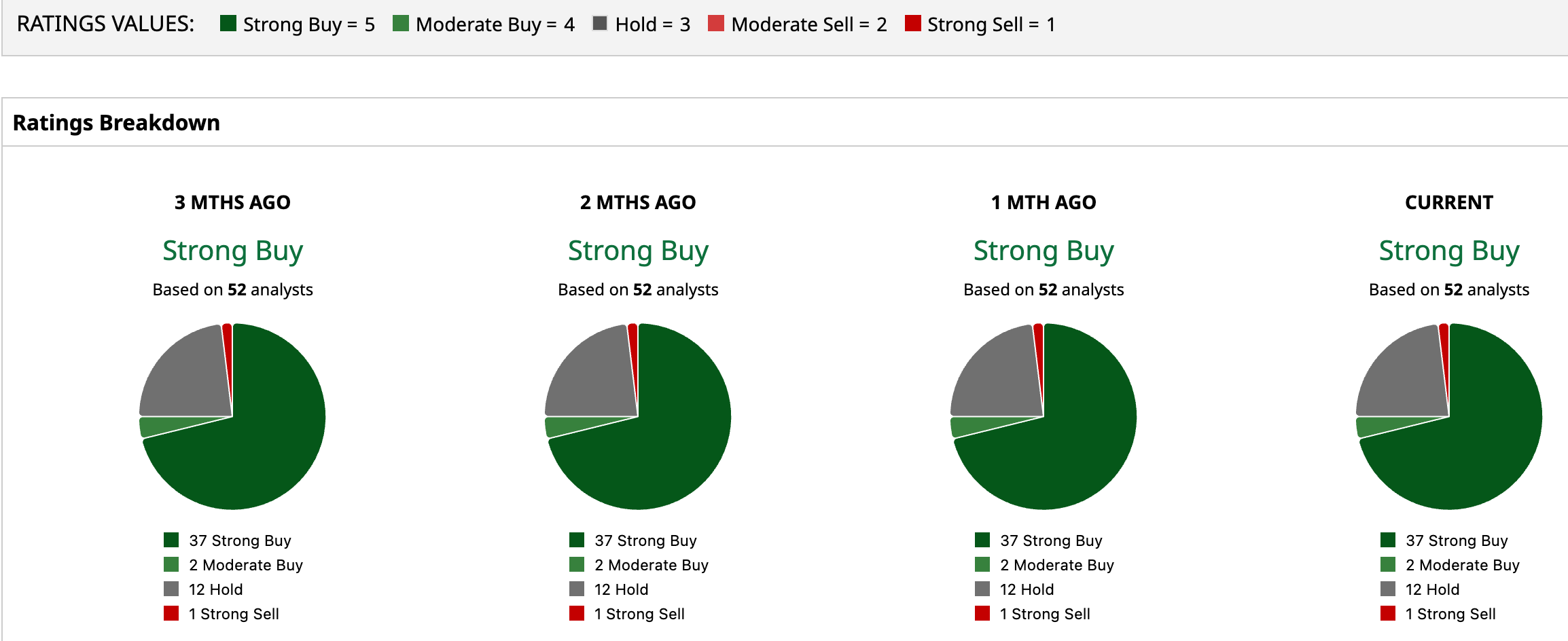

Wall Street’s confidence in Salesforce remains firmly intact, with the stock commanding a “Strong Buy” consensus rating that underscores broad bullish sentiment. Out of 52 analysts covering the name, an overwhelming 37 have issued “Strong Buy” ratings, while two recommend “Moderate Buy.” Meanwhile, 12 analysts remain on the sidelines with “Hold,” and just one stands out with a “Strong Sell,” highlighting how overwhelmingly positive the Street’s view remains.

The upside case is also notable, with an average price target of $277.14, implying a 64.9% gain, while the Street-high target of $475 suggests potential upside of up to 182.6% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Stock #2: ServiceNow

Headquartered in Santa Clara, ServiceNow is a major player in cloud-based enterprise software, focused on helping organizations simplify and automate their day-to-day operations. Established in 2004, the company began with IT service management solutions but has steadily grown into a comprehensive platform that links together people, systems, and processes across large enterprises.

Artificial intelligence is becoming an increasingly important part of that platform. ServiceNow is weaving generative AI and machine learning into its offerings to power automation, surface insights, and make interactions more intuitive. These capabilities are aimed at cutting down manual effort and helping teams respond more quickly across areas like IT, customer support, human resources, and risk management.

Currently valued at a market capitalization of around $101.9 billion, ServiceNow has fallen out of favor on Wall Street, mirroring the broader weakness in software stocks. Shares have dropped nearly 46% over the past year, and the sell-off has only intensified in 2026, with the stock down about 36.4% year-to-date (YTD), significantly lagging the broader market across both periods.

www.barchart.com

www.barchart.com ServiceNow ended the year on a strong note, delivering a fiscal 2025 fourth-quarter report in late January that comfortably topped Wall Street expectations on both revenue and earnings. The company reported total revenue of $3.57 billion, marking a robust 20.5% YOY increase, while its core subscription revenue, the primary growth engine, shot up 21% to $3.47 billion. Notably, the top line also came in ahead of the Street’s estimate of $3.52 billion, underscoring sustained demand for its platform.

The company’s forward-looking indicators painted an equally impressive picture. Current remaining performance obligations (cRPO), which represent contracted revenue set to be recognized over the next 12 months, surged 25% YOY to $12.85 billion. Large deal activity remained strong, with 244 transactions exceeding $1 million in net new annual contract value (ACV), reflecting nearly 40% YOY growth.

ServiceNow also expanded its base of high-value customers, ending the quarter with 603 clients generating over $5 million in ACV, up roughly 20% from a year ago. A key strategic highlight was ServiceNow’s deepening partnership with Anthropic, aimed at embedding Claude models more deeply into the ServiceNow AI Platform. These models are helping power an enterprise-grade AI development environment, enabling developers of all skill levels to build and deploy agentic workflows with built-in governance.

On the profitability front, adjusted EPS rose 26% YOY to $0.92, beating expectations of $0.87. Also, the company took steps to reward shareholders and manage dilution following its December 2025 5-for-1 stock split, with its board authorizing an additional $5 billion share repurchase program, including plans for a near-term $2 billion accelerated buyback.

Looking ahead, ServiceNow offered a confident outlook. For the first quarter of fiscal 2026, subscription revenue is expected to land between $3.650 billion and $3.655 billion, implying approximately 22.5% YOY growth at the midpoint. For the full year, subscription revenue is projected in the range of $15.53 billion to $15.57 billion, reflecting anticipated growth of roughly 20.5% to 21%, signaling continued momentum as the company scales its AI-driven platform.

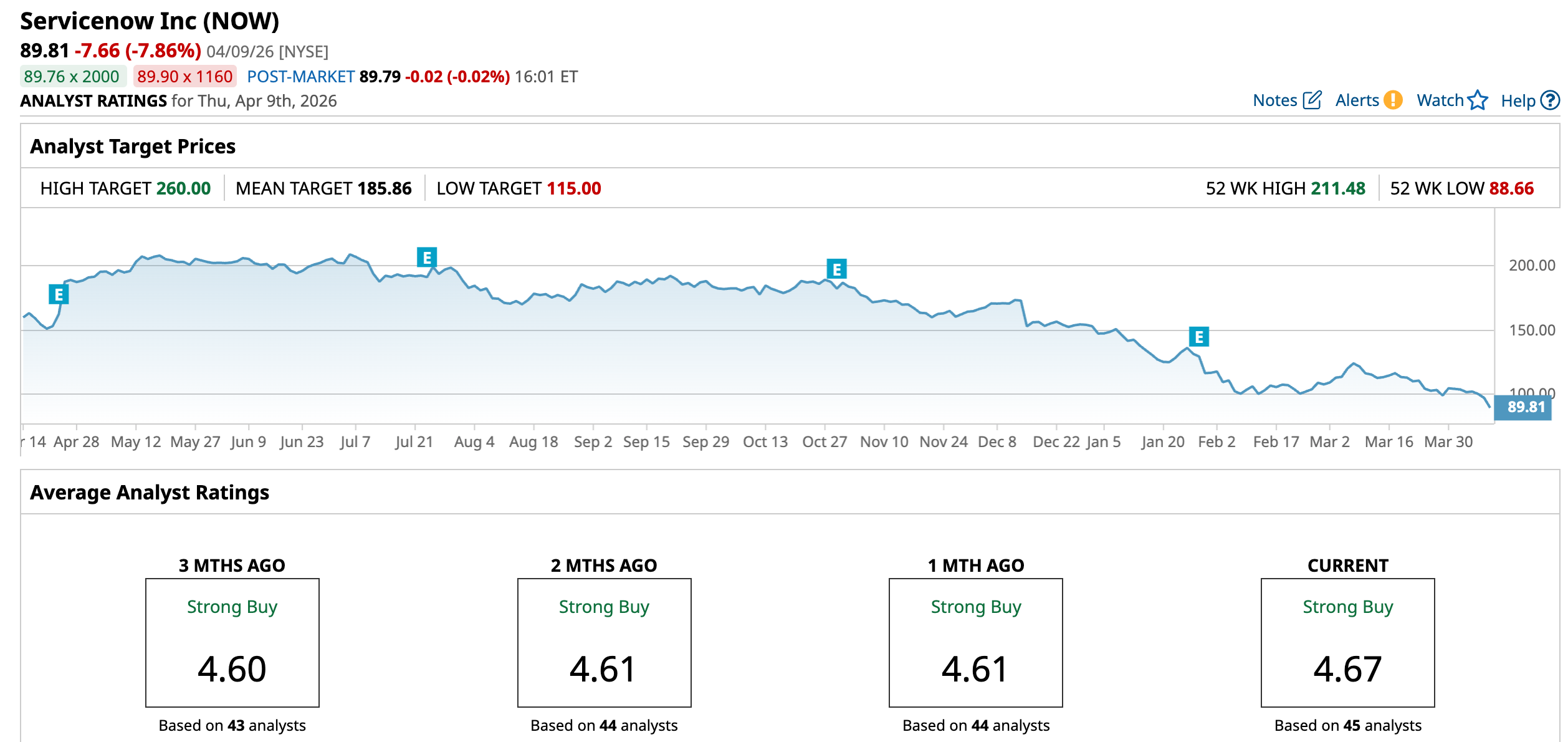

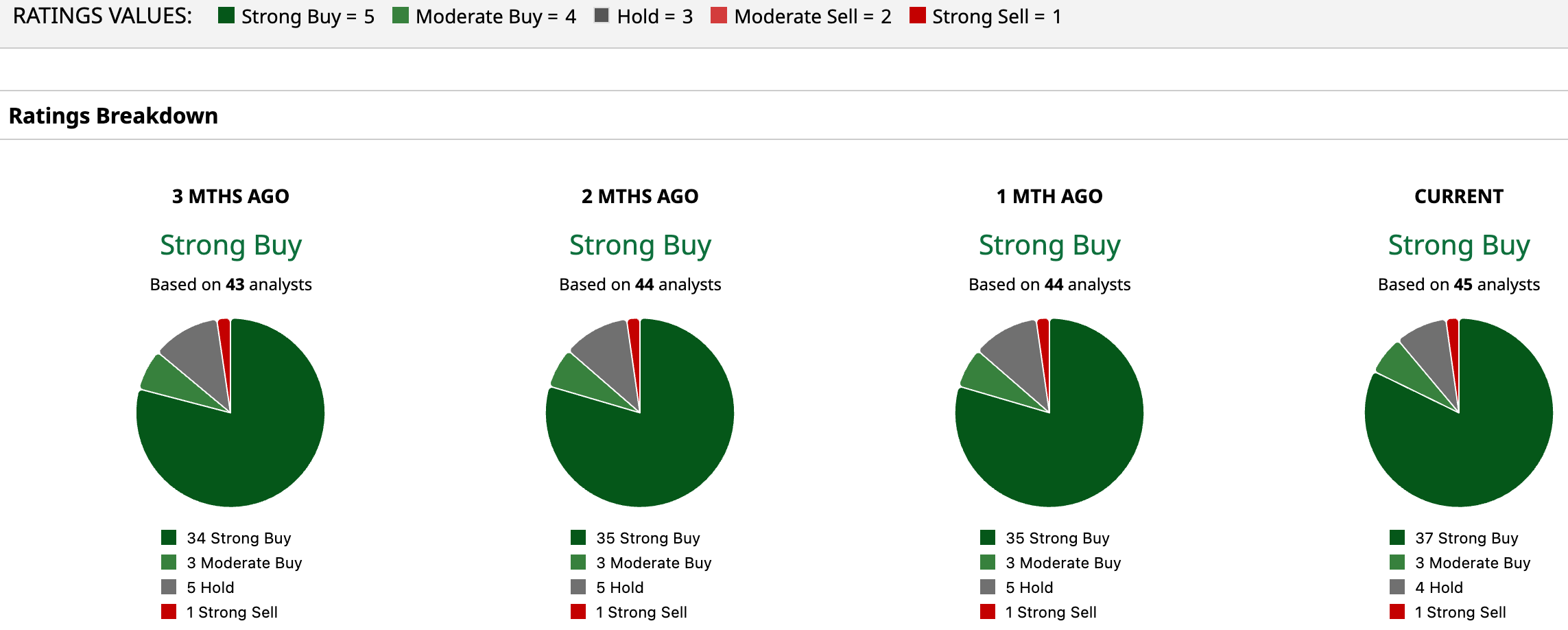

Overall, Wall Street’s optimism around ServiceNow remains strong, with the stock earning a “Strong Buy” consensus rating that reflects broad confidence in its long-term outlook. Of the 45 analysts covering the name, a dominant 37 rate it a “Strong Buy,” while three recommend “Moderate Buy.” Only four sit on the sidelines with “Hold,” and just one has issued a “Strong Sell,” underscoring how tilted sentiment remains toward the bullish side.

Moreover, despite recent weakness, analysts see significant upside ahead. The average price target of $185.86 implies a 107% gain, while the Street-high target of $260 points to a potential surge of up to 189.5% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The Selloffs in ServiceNow and Salesforce Stocks Are Disconnected, Says Wedbush. Should You Buy the Dips? Should You Chase the Rally in BlackBerry Stock Today? Micron Stock Is Up on Ceasefire News. Should You Buy MU Here? Palantir Stock Slumps on Michael Burry Comments. Should You Buy the Dip or Stay Away?