Morgan Stanley MS is slated to announce first-quarter 2026 earnings on April 15 before the opening bell. As always, the company’s financial performance and the ensuing management conference call are expected to draw close attention from analysts and investors to understand how it is navigating the current operating backdrop.

Morgan Stanley’s 2025 performance was impressive, driven by robust trading and deal-making activities. This time, the company’s results will likely be robust given the solid trading and investment banking (IB) performance. The Zacks Consensus Estimate for first-quarter revenues of $19.88 billion suggests 12.1% year-over-year growth.

In the past seven days, the consensus estimate for earnings for the to-be-reported quarter has remained unchanged at $3.08. The figure indicates an 18.5% increase from the prior-year quarter.

Estimate Revision Trend

Image Source: Zacks Investment Research

MS has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, with the average beat being 18.19%.

Earnings Surprise History

Image Source: Zacks Investment Research

Factors to Impact Morgan Stanley’s Q1 Results

IB Income: Deal-making activity was robust in the first quarter despite the Middle Eastern conflict and the ensuing uncertainty about its impact on the economy in the last month of the quarter. While global mergers and acquisitions (M&As) volume declined year over year, deal value rose as big transactions dominated the space. Unlike last year, when President Donald Trump’s announcement of ‘Liberation Day’ tariff plans led to the deal drought for several months, this time, companies acknowledged that volatility is part of life, and they will have to do business around it. Lower capital costs and a focus on scale and AI integration drove the M&As.

Thus, robust deal-making activities are expected to have driven Morgan Stanley’s advisory fees in the quarter. The company’s position as one of the leading players in the space is likely to have aided advisory fees to some extent. The Zacks Consensus Estimate for advisory fees is pegged at $883.7 million, indicating a whopping year-over-year jump of 51.6%.

The first quarter saw decent IPO activity, with issuance volume improving despite fewer companies getting listed. On the other hand, global bond issuance volume was solid. So, Morgan Stanley’s equity and fixed income underwriting fees are expected to have improved in the quarter on a year-over-year basis.

The Zacks Consensus Estimate for equity underwriting fees of $395.2 million suggests year-over-year growth of 23.9%. The consensus estimate for fixed-income underwriting fees is pegged at $667.3 million, indicating a fall of 1.4%. The consensus estimate for total underwriting fees of $1.06 billion implies a rise of 6.7%.

The Zacks Consensus Estimate for IB income of $2.02 billion indicates a year-over-year jump of 29.5%.

Trading Revenues: The performance of Morgan Stanley’s trading business (constituting a significant portion of its top line) is expected to have been solid in the first quarter of 2026, supported by increased client activity and market volatility. Major factors that influenced trading business in the quarter included shifting expectations around AI, rising geopolitical tensions, particularly concerns over the Middle East and the risk of an oil shock, persistent inflation concerns and uncertainty around the Fed’s monetary policy stance. Volatility was high in equity markets and other asset classes, including commodities, bonds and foreign exchange.

The Zacks Consensus Estimate for the company’s equity trading revenues is pegged at $4.74 billion, suggesting a rise of 15% from the prior-year quarter. The consensus estimate for fixed-income trading revenues of $2.9 billion indicates a gain of 11.2%.

Net Interest Income (NII): In the to-be-reported quarter, the Federal Reserve kept interest rates unchanged. This, along with a solid lending scenario and stabilizing funding/deposit costs, is expected to have offered much-needed support. Hence, Morgan Stanley’s NII is likely to have witnessed a modest improvement in the quarter.

The Zacks Consensus Estimate for net interest revenues is pegged at $2.58 billion, suggesting a rise of 9.7% on a year-over-year basis.

For the wealth management segment, management expects NII to rise modestly on a sequential basis.

Expenses: Cost reduction, which has long been Morgan Stanley's primary strategy for remaining profitable, is unlikely to have provided much support in the March-ended quarter. As the company has been investing in franchises, overall costs are anticipated to have been elevated.

What Our Quantitative Model Unveils for MS

Our proven model does not predict an earnings beat for Morgan Stanley this time around. This is because it doesn’t have the right combination of the two key ingredients — a positive Earnings ESP and a Zacks Rank #3 (Hold) or better.

The Earnings ESP for Morgan Stanley is 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

MS currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Morgan Stanley’s Price Performance

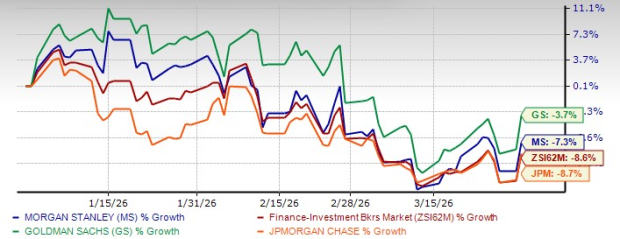

In the first quarter, the MS stock performance was subdued as the Middle East conflict and private credit-related concerns hurt investor sentiment. The stock performed better than the industry and JPMorgan JPM, while lagging behind Goldman Sachs GS.

1Q26 Price Performance

Image Source: Zacks Investment Research

Goldman is scheduled to announce first-quarter 2026 numbers on April 13, while JPMorgan is set to announce results on April 14.

Over the past month, the Zacks Consensus Estimate for Goldman’s first-quarter 2026 earnings has been revised north to $16.48. On the other hand, the consensus estimate for JPMorgan has been revised lower to $5.46 over the past 30 days. At present, both GS and JPM carry a Zacks Rank #3.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Goldman Sachs Group, Inc. (GS): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

Morgan Stanley (MS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).