The cybersecurity sector is facing a sharp sentiment reset in 2026, with leading platforms like Palo Alto Networks (PANW) caught in a broader selloff driven by investor concerns that next-generation artificial intelligence (AI) could both disrupt traditional security models and compress long-term margins. Yet, just as the narrative turned cautious, a new catalyst emerged, with Anthropic’s launch of Project Glasswing, a high-profile collaboration that includes Palo Alto alongside major technology leaders to deploy advanced AI for defensive cybersecurity.

At the center of the initiative is Anthropic’s powerful Claude Mythos Preview model, which has already demonstrated the ability to uncover thousands of critical vulnerabilities across software systems, capabilities that could redefine how enterprises approach threat detection and prevention.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The announcement initially reignited optimism, briefly lifting cybersecurity stocks as investors interpreted the partnership as validation that companies like Palo Alto will remain relevant in an AI-driven security landscape. However, that enthusiasm proved short-lived, with shares pulling back again.

With PANW stock now down 25% over the past six months, investors wonder whether or not the stock can rebound anytime soon.

About Palo Alto Networks Stock

Palo Alto Networks is a leading global cybersecurity platform provider headquartered in Santa Clara, California. The company offers a broad suite of solutions spanning network security, cloud security, and AI-driven security operations. Palo Alto Networks is valued as a large-cap technology leader with a market cap of $127.1 billion, reflecting its scale and strategic importance in the rapidly evolving cybersecurity landscape.

Palo Alto Networks has experienced a notable reset in valuation over recent months, reflecting both sector-wide pressure and evolving investor expectations around AI-driven cybersecurity.

Over the past 52 weeks, the stock has declined 7.45% and 15.46% year-to-date (YTD) amid a broader derating across high-growth cybersecurity names as multiples compress. Moreover, the stock slumping 25% over the past six months reflects heightened volatility and fragile investor positioning.

Importantly, this weakness comes even as Palo Alto announced a new partnership tied to Project Glasswing from Anthropic, highlighting the company’s push into AI-driven cybersecurity. While the announcement briefly lifted sentiment, the rally proved short-lived, suggesting that investors are demanding clearer evidence of monetization, margin expansion, and sustainable AI integration rather than headline partnerships alone. The stock rose 2.3% intraday on Apr. 8 following the news, but declined in the next session by 3.9% on Apr. 9.

Project Glasswing is a major AI-driven cybersecurity initiative built on its Claude Mythos Preview model. The project brings together top tech players, including Microsoft Corporation (MSFT), Amazon.com (AMZN), NVIDIA Corporation (NVDA), and Alphabet (GOOG) (GOOGL) to strengthen defenses against rapidly evolving AI-powered threats.

The initiative highlights how advanced AI models can already uncover thousands of critical software vulnerabilities, raising both risk and urgency for stronger cyber defenses. Analysts view this as a positive for leading cybersecurity firms, arguing that companies like Palo Alto are well-positioned to monetize rising demand as cyber spending, currently 5% of IT budgets, could double in the coming years.

www.barchart.com

www.barchart.com Priced at 78.16 times forward earnings, the stock trades at a premium to the sector median.

Steady Q2 Financials But Lowered Guidance

Palo Alto Networks reported its fiscal second quarter 2026 results on Feb. 17, delivering solid top line growth and margin expansion, although guidance weighed on investor sentiment.

The company generated revenue of $2.6 billion, up 15% year-over-year (YOY). Profitability improved meaningfully as non-GAAP net income increased to $732 million or $1.03 per share from $566 million or $0.81 per share, representing strong earnings growth and an earnings beat versus expectations.

From a recurring revenue perspective, Palo Alto continued to demonstrate strong platform traction. Next-Generation Security (NGS) ARR grew 33% YOY to $6.3 billion, while remaining performance obligations (RPO) increased 23% to $16 billion, highlighting strong backlog visibility and customer commitment to long-term contracts. Margins also remained robust, with non-GAAP operating margin at 30.3%.

However, the key debate centered on forward guidance. For fiscal Q3 2026, the company guided to revenue of $2.941 billion to $2.945 billion (around 28% to 29% growth) and non-GAAP EPS of $0.78 to $0.80, the latter falling below expectations. For the full fiscal year 2026, Palo Alto raised its revenue outlook to $11.28–$11.31 billion (up 22% to 23% YOY), but lowered EPS guidance to $3.65 to $3.70, reflecting margin pressure from acquisitions and higher operating costs.

Fiscal 2026 profit is expected to be $2.14 per share as per consensus, up 30.5% YOY, and rise another 7% to $2.29 per share in fiscal 2027.

What Do Analysts Expect for Palo Alto Networks Stock?

Last month, Cantor Fitzgerald reiterated an “Overweight” rating on Palo Alto Networks after its strong Q2 FY2026 results, which beat expectations.

Also, Barclays reiterated an “Overweight” rating and $200 price target on Palo Alto Networks after CEO Nikesh Arora made a $10 million insider purchase. Barclays views the move as a bullish indicator amid AI-related concerns.

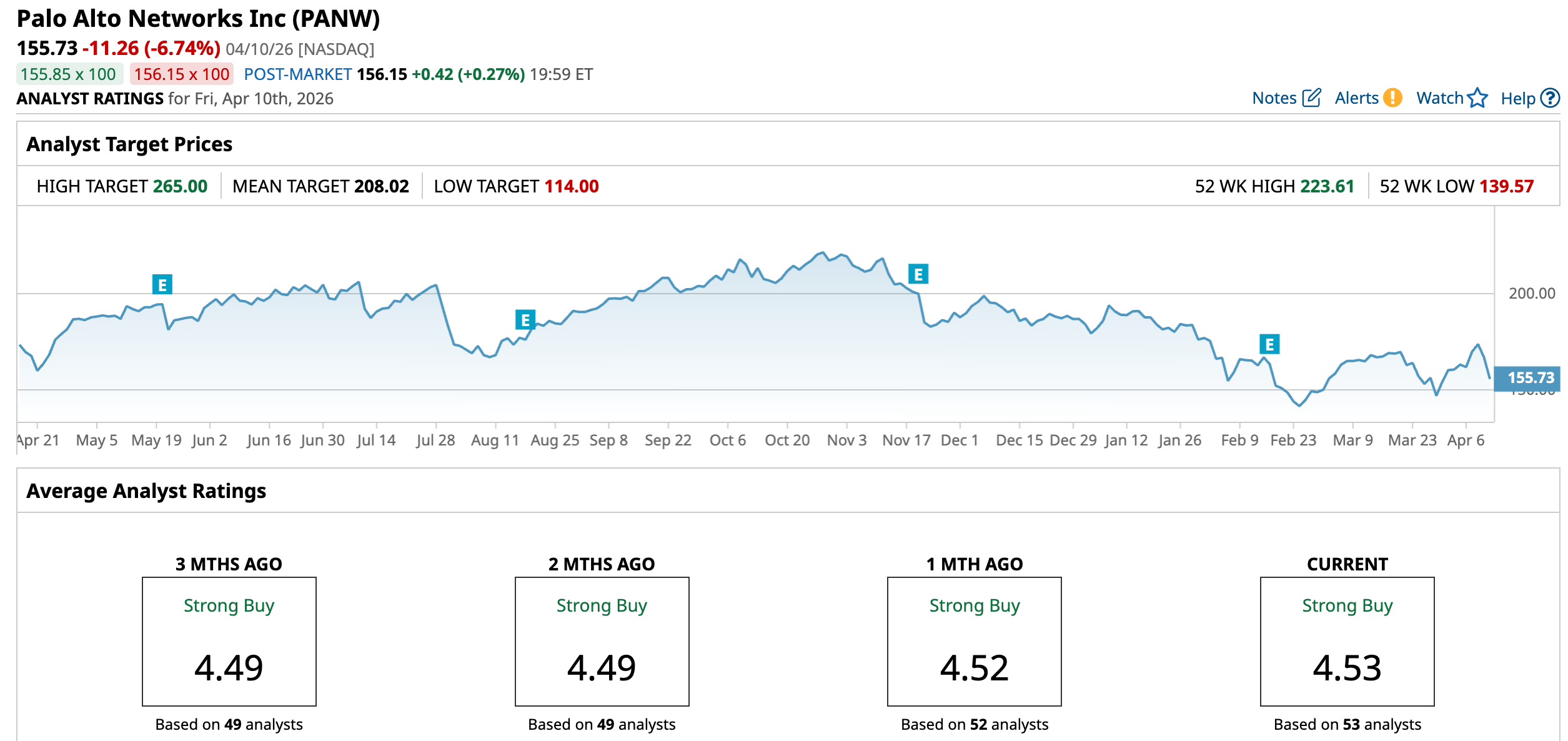

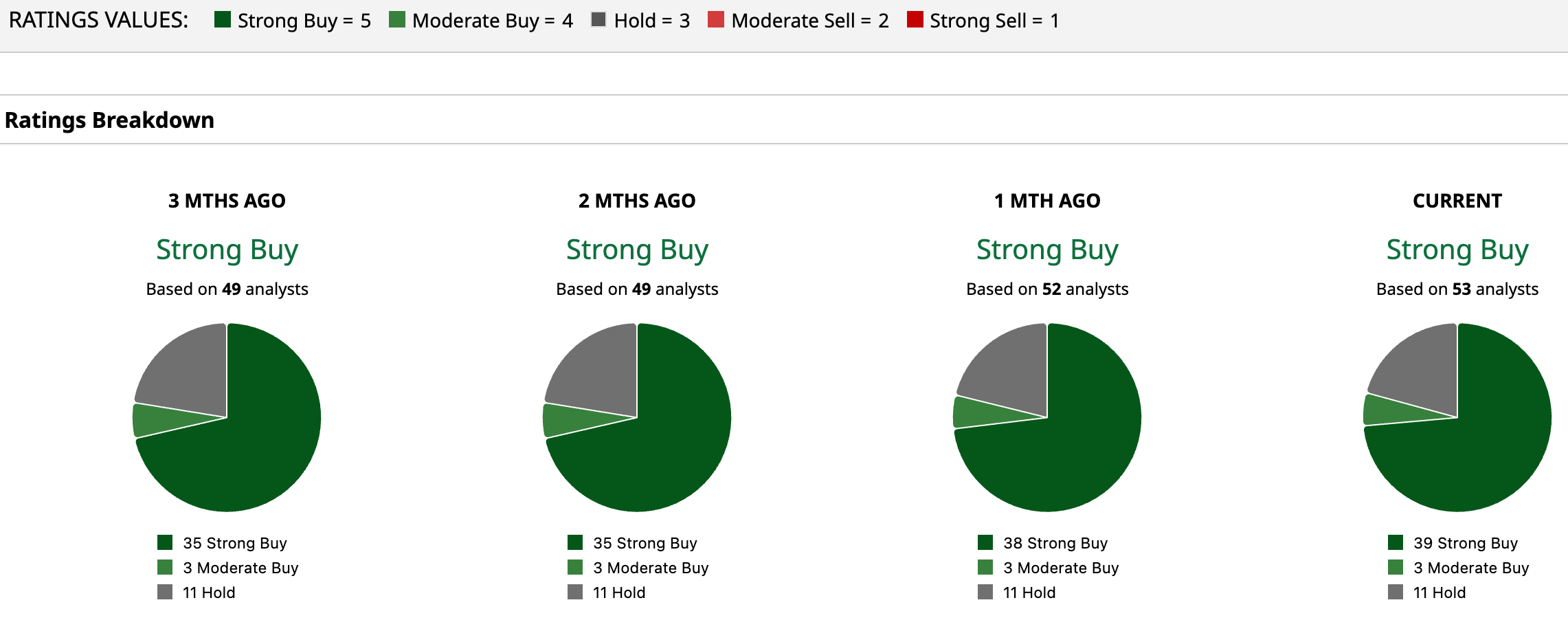

The stock has a consensus “Strong Buy” rating overall. Of 53 analysts covering the stock, 39 recommend a “Strong Buy,” three advise for a “Moderate Buy,” and the remaining 11 suggest a “Hold.”

The average analyst price target of $208.02 indicates potential upside of 33.58% from the current price levels. The Street-high price target of $265 suggests that the stock could rally as much as 70.17% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As the Cybersecurity Selloff Continues, Palo Alto Just Scored a New Deal with Anthropic. Should You Buy the Dip in PANW Stock? Dear ASML Stock Fans, Mark Your Calendars for April 15 Palantir Stock Is at 6-Month Lows - Time to Buy PLTR? JPMorgan Is Betting on the ‘American Dream’ with a New $1.5 Trillion Initiative. What Does That Really Mean?