Lumen Technologies LUMN is in an important phase of its turnaround, with management targeting adjusted EBITDA inflection in 2026 after a period of sustained pressure. For 2026, adjusted EBITDA is forecasted to be between $3.1 billion and $3.3 billion, driven by cost discipline, portfolio rejig and balance sheet restructuring.

Lumen has resorted to aggressive cost-cutting. The company is anticipating $1 billion in cost savings by the end of 2027 through planned infrastructure simplification across the network, product portfolio and IT. Lumen is also leveraging AI tech to drive intelligence and automation. The company recently launched phase one of its ERP implementation. In the current year, Lumen expects to reach $700 million of run-rate cost benefit compared with $400 million (higher than its target of $350 million) already achieved in 2025.

Cost discipline, coupled with a roughly $500 million reduction in annual interest expense following debt paydowns, is expected to provide meaningful EBITDA support.

At the same time, Lumen is reshaping its business toward higher-margin growth areas. The explosive growth of AI workloads is driving demand for low-latency, high-bandwidth fiber connectivity between data centers, cloud regions and enterprise clients, resulting in increasing demand for Lumen's Private Connectivity Fabric (“PCF”) and network-as-a-service (NaaS) solutions. Driven by significant AI-fueled connectivity demand, Lumen has secured a total of $13 billion in PCF deals at the end of the fourth quarter of 2025.

Beyond fiber, Lumen is building the NaaS business, with its customer base now exceeding 2000. Management remains upbeat about Internet on Demand, or IoD Offnet, and expects this solution to boost market reach with more than 900 off-net ports sold already.

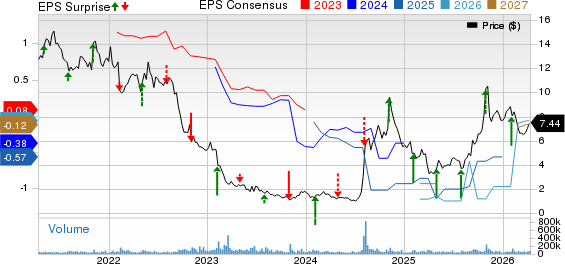

Lumen Technologies, Inc. Price, Consensus and EPS Surprise

Lumen Technologies, Inc. price-consensus-eps-surprise-chart | Lumen Technologies, Inc. Quote

The long-term outlook presented at Investor Day reinforces this shift. Lumen noted that it was working on boosting adjusted EBITDA margins to approximately the mid 30% range by 2030 from 27.1% reported in 2025.

Nonetheless, challenges persist for Lumen. The company must sustain the cost-saving momentum while stabilizing revenues and managing its debt profile. Despite deleveraging, the debt is still hovering at about $13 billion.

Further, as the company shifts toward newer growth products like fiber and cloud-based offerings, the secular headwinds in the legacy business will continue to prove a strain on the top-line expansion, at least in the near term. More importantly, management expects Business segment revenue only in 2028, implying at least a couple more years of structural decline.

The company’s ability to ramp the digital platform and capitalize on AI-driven demand will ultimately determine whether its strategic efforts deliver desired results

Taking a Look at Profitability Metrics for Rivals

Cogent Communications CCOI is a Tier 1 Internet Service Provider offering low-cost, high-speed Internet access, private network services and colocation services with ultra-low-latency data transmission. The company’s profitability is improving, driven by disciplined cost management and a favorable product mix. The company’s gross margin expanded 720 basis points year over year to 45.4% for 2025, while EBITDA margin expanded 790 basis points to 19.8%.

However, Cogent Communications expects margin rate expansion to moderate going forward. Management forecasts EBITDA margin expansion to moderate, at approximately 200 basis points per year, compared with 790 basis points achieved in 2025, caused primarily by cost savings.

AT&T T is one of the world’s leading communications service carriers. For 2025, AT&T recorded revenues of $125.6 billion compared with $122.3 billion in 2024. Adjusted EBITDA for 2025 was $46.4 billion, up from $44.8 billion in 2024.

AT&T expects adjusted EBITDA growth in the 3% to 4% range in 2026, while it expects the rate to improve to more than 5% by 2028. The company achieved more than $1 billion of cost savings in 2025 and expects to achieve an additional $4 billion annual cost savings by the end of 2028 via operational efficiency, along with reductions in legacy operations and support expenses.

LUMN Price Performance, Valuation and Estimates

Shares of LUMN have gained 11.2% in the past month against the Diversified Communications Services industry’s decline of 2.9%.

Image Source: Zacks Investment Research

Regarding the forward 12-month price/sales ratio, LUMN is trading at 0.71, lower than the sector’s multiple of 1.64.

Image Source: Zacks Investment Research

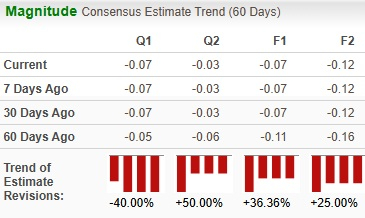

The Zacks Consensus Estimate for LUMN’s earnings for fiscal 2026 has been revised upward significantly over the past 60 days.

Image Source: Zacks Investment Research

LUMN currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AT&T Inc. (T): Free Stock Analysis Report

Cogent Communications Holdings, Inc. (CCOI): Free Stock Analysis Report

Lumen Technologies, Inc. (LUMN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).