The first-quarter 2026 earnings season is kicking off this week and, as usual, Netflix (NFLX) will be among the first tech names to report on April 16. NFLX stock is up 10% so far this year and outperforming the average S&P 500 Index ($SPX) peer. These gains could be attributable to the company's decision to walk away from acquiring Warner Bros. Disovery (WBD) assets — a costly proposal that Netflix had failed to sell to markets.

While tech peers have whipsawed this year amid worries over Middle East tensions, NFLX stock has been relatively stable. In fact, it had the potential to outperform amid the Iran war. Indeed, NFLX stock has fared better than the broader markets over this period, although not to the extent that I had previously expected. Ahead of Q1 earnings, however, Netlfix stock looks like a buy. Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

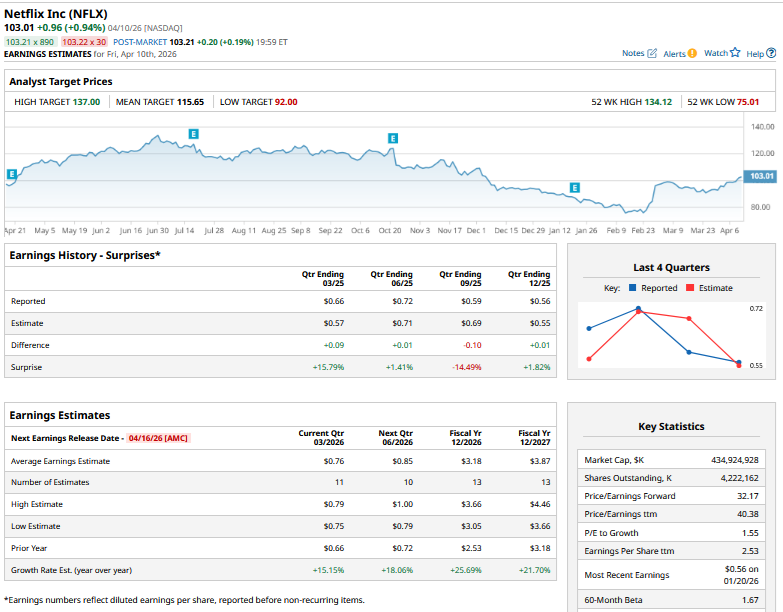

Earnings Estimates for Q1 2026

Analysts expect Netflix to report revenue of $12.17 billion in the March quarter, a year-over-year (YOY) increase of more than 15%. These estimates are in line with guidance that the company provided earlier this year while releasing Q4 2025 earnings. Analysts are also modelling for EPS of 76 cents, which is similar to the company’s guidance.

www.barchart.com

www.barchart.comNotably, Netflix raised prices across its streaming plans late last month. However, the price hikes will start reflecting in the company’s revenues in the coming quarters as existing members renew their subscriptions. Netflix had last raised prices in January 2025, but the hike did not lead to much churn, and the company added 23 million subscribers last year. While that number is below the stellar growth Netflix saw in the preceding two years, that growth came on the back of the company's password-sharing crackdown and the launch of the low-priced ad-supported tier. With that said, both stories have largely played out, even though Netflix has yet to launch its ad-supported tier in several regions.

Netflix Should See Sustainable Double-Digit Growth and Margin Expansion

Netflix has a decent moat in an otherwise crowded streaming industry, and the company has capitalized on that advantage to raise prices. The streamer has also been able to cajole many of its non-paying viewers who were watching content on borrowed passwords into becoming paying subscribers. Netflix appears to be a structural growth story that brings prospects of sustainable double-digit growth to the table, driven by subscriber growth, higher average revenue per user (ARPU), and ad revenue.

While Netflix might not see the kind of subscriber growth it saw between 2023 and 2024, its paying member base should continue to rise in the single digits over the near foreseeable future. ARPU should also rise on the back of price hikes. For context, the 2026 price hikes are in the double digits across all plans, barring the premium plan's hike of roughly 8%.

Netflix's ad business is witnessing strong growth as well, with revenue rising more than 2.5 times to $1.5 billion last year. The company expects revenue to “roughly double” this year as it capitalizes on a growing subscription base on the ad-supported tier. Going by the company’s guidance, ad revenue would account for under 6% of its consolidated revenue this year, but the business is growing in the triple digits.

Simple back-of-the-envelope calculations tell us that, with these three moving parts, Netflix should be able to deliver double-digit annual revenue growth even if it falters slightly on these variables.

Netflix expects margins to keep expanding every year, which is not an unreasonable expectation, as it aims to keep content spending growth below revenue growth. The business also has high operating leverage as content and technology costs are largely fixed and revenues from new members help expand margins — characteristics that are similar to the software industry.

What Do Analysts Think of Netflix Stock?

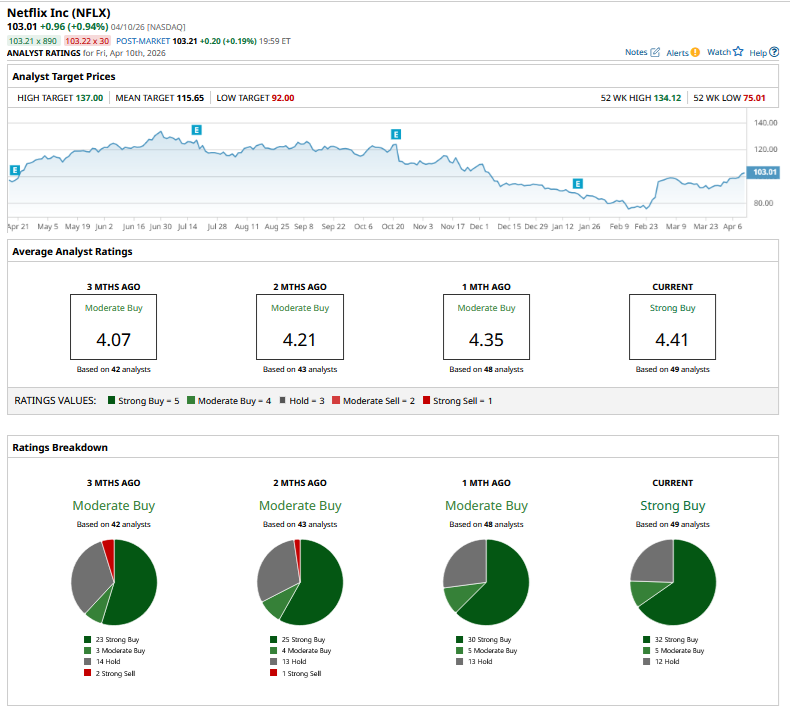

Sell-side analysts have been getting incrementally bullish on Netflix. Earlier this month, Goldman Sachs upgraded NFLX stock from “Neutral” to “Buy” while raising its target price from $100 to $120. Wedbush, HSBC, Morgan Stanley, and Rosenblatt have also raised their price targets heading into the Q1 report.

Overall, NFLX stock has a consensus “Strong Buy” rating. Out of 49 analysts with coverage, 32 have a “Strong Buy” rating, five have a “Moderate Buy” rating, and 12 analysts have a “Hold” rating. The mean target price is $115.65, which represents roughly 12% potential upside from current price levels. Analysts should revise their price targets after the upcoming earnings report, and I expect most to raise their forecasts.

www.barchart.com

www.barchart.comShould You Buy Netflix Stock Before Q1 Earnings?

Netflix trades at a forward price-to-earnings (P/E) multiple of 32.17 times while the 2027 P/E is roughly 27 times. These multiples look reasonable, albeit not mouthwateringly cheap. Given Netflix’s strong moat in the streaming industry as well as the structural topline growth and margin expansion story, I remain bullish on NFLX stock heading into the Q1 earnings report.

On the date of publication, Mohit Oberoi had a position in: NFLX . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Ignore the Anthropic Panic and Keep Buying Palantir Stock, Says Wedbush Is Netflix Stock a Buy Ahead of Its Q1 Earnings Report on April 16 Is Nvidia Acquiring Dell? Why DELL Stock Is Up Today. On Semiconductor Pops on Analyst Upgrade. Should You Buy ON Stock Here?