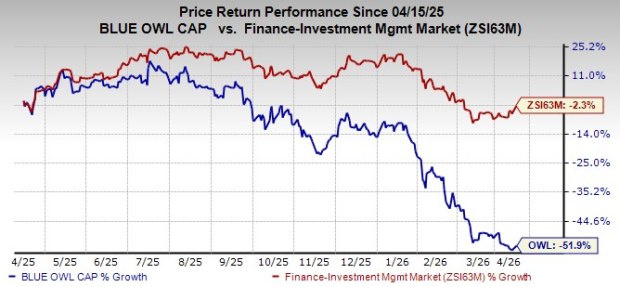

Blue Owl Capital Inc. OWL has suffered a sharp selloff, leaving the stock well behind both its industry and the broader market. Over the past year, shares have declined 51.9%, compared with a 2.3% decline for the industry.

Image Source: Zacks Investment Research

That gap comes as the Financial - Investment Management industry sits in a weak cohort, with a Zacks Industry Rank in the bottom 14% (210 out of 244). At the same time, OWL’s earnings estimates for 2026 and 2027 have moved lower over the past month, reinforcing cautious sentiment around the name.

With the stock carrying a Zacks Rank #5 (Strong Sell), the setup reflects weak revision momentum and a skeptical market tone.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Blue Owl’s Near-Term Issue: Private Credit Liquidity

The primary near-term overhang is private-credit liquidity and sentiment risk, particularly in retail-oriented, semi-liquid structures. Toward the end of 2025, non-traded business development companies experienced slower flows and elevated redemption requests, with spillover continuing into 2026.

Within that backdrop, Blue Owl restricted withdrawals at Blue Owl Capital Corporation II (OBDC II) after redemption requests hit the 5% threshold. The company also sold assets across affiliated funds to meet liquidity needs. This is a critical point because it ties directly to confidence in semi-liquid private-credit products.

If trust in these vehicles erodes across the sector, it can weigh on fundraising momentum, fee growth, and valuation multiples. That is the channel through which liquidity strain turns into broader pressure on fee-related earnings revenue growth in the near term.

OWL Fee Visibility Exists, but Timing Risk Matters

Blue Owl has meaningful “embedded” fee growth, but the timing is the issue. At 2025-end, $28.4 billion of assets that were not yet fee-paying, underscoring significant fee earnings upside as deployment progresses. Per management, that capital will likely generate more than $325 million of annual management fees once fully deployed.

Nonetheless, the fee ramp depends on when capital is put to work across strategies. The deployment and closing cadence spans credit, digital infrastructure, a large net lease backlog, and GP-led continuation activity, and the pace of those levers determines when revenue shows up.

That timing sensitivity creates a clear risk: if deployment elongates or activity clusters into the back half of 2026, fee recognition is likely to be deferred and near-term upside compressed. In a market already focused on liquidity optics, delayed fee realization can keep valuation support from stabilizing quickly.

Blue Owl’s Portfolio Risk: Borrower Quality Questions

Investor concerns are not limited to flows. There is rising caution around private-credit borrower quality, with particular focus on software and AI-adjacent borrowers. The worry is that earnings durability can be harder to assess in mid-sized technology companies, and competitive positions can shift quickly as disruption accelerates.

For Blue Owl, weaker borrower fundamentals can translate into practical portfolio risks. These include higher downgrade risk, tighter covenant cushions, and elevated restructuring or loss risk across the portfolio. Even without a broad credit event, that mix can weigh on confidence in the credit book’s risk-adjusted returns.

The issue is also about perception. When investors become more selective toward certain borrower pockets, fundraising conversations can turn from growth to risk controls, which can limit incremental enthusiasm for the platform’s credit expansion until the narrative improves.

OWL Expenses Are Still a Drag on the Bottom Line

Costs remain another sticking point. Blue Owl’s total expenses posted a four-year compound annual growth rate of 8.4% from 2021 to 2025, driven primarily by higher general, administrative and other expenses, as well as compensation and benefits.

Management’s operating posture suggests only modest operating leverage in 2026, which means expense discipline is not likely to provide a quick margin unlock. Ongoing investments in the franchise and distribution, combined with revenue-related compensation, are expected to keep expenses elevated.

That matters because profitability has already shown sensitivity to spending. In 2025, OWL’s fee-related earnings margin was 58.3%, down 110 basis points from 2024, reflecting higher compensation and non-compensation expenses tied to investment in new platforms and distribution.

What Could Improve the Setup for Blue Owl

Some stabilizers are expected to support a better setup over time. Blue Owl’s model is anchored by permanent capital vehicles and long-dated funds, and about 85% of management fees were earned from permanent capital vehicles as of Dec. 31, 2025. That structure is designed to provide predictable fee streams and earnings stability.

Fundraising momentum is also a constructive offset. OWL raised $42 billion in 2025, up from $27.5 billion in 2024, and management expects 2026 fundraising to look similar to 2025. More broadly, a return to normalized deployment would help convert the embedded fee opportunity into realized revenue and support margin leverage beyond near-term volatility.

Blue Owl Capital Inc. Price and Consensus

Blue Owl Capital Inc. price-consensus-chart | Blue Owl Capital Inc. Quote

For context, larger alternative managers such as Apollo Global Management, Inc. APO and Blackstone Inc. BX currently carry a Zacks Rank #3 (Hold), reflecting a more balanced estimate picture than OWL. Though both Apollo Global and Blackstone faced redemption requests from investors, the problem is less severe for them, mainly attributable to their diversified business.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Blackstone Inc. (BX): Free Stock Analysis Report

Apollo Global Management Inc. (APO): Free Stock Analysis Report

Blue Owl Capital Inc. (OWL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).