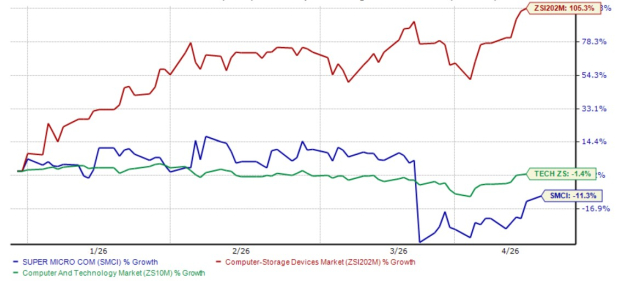

Super Micro Computer SMCI shares have plunged 11.3% year to date, underperforming the Zacks Computer- Storage Devices industry and the Zacks Computer and Technology sector. While the industry has returned 105.3%, the broader sector has declined 1.4% in the same time frame.

SMCI YTD Performance Chart

Image Source: Zacks Investment Research

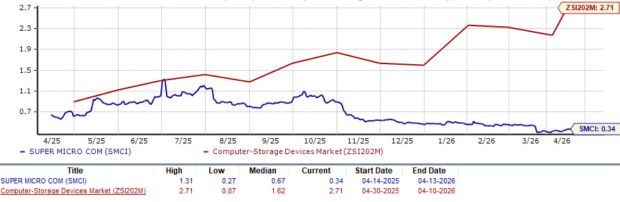

This decline in stock price has resulted in SMCI trading at a discount compared to the industry and broader sector. SMCI stock trades at a forward price to sales ratio of 0.34, much lower than the industry’s ratio of 2.71. The undervaluation of SMCI stock is further substantiated by the Zacks Value Score of B.

SMCI Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

Given these dynamics, investors are wondering if it’s the right time to buy, sell or hold the stock. Let’s delve deeper into the fundamentals to unravel what investors should do with SMCI.

Global AI Infrastructure Expansion Fuels SMCI’s Growth Momentum

SMCI is capitalizing on immense AI infrastructure demand by AI data centers, hyperscalers, AI-fabs and enterprise customers. SMCI’s rack-scale AI clusters and integrated data center systems have transformed the company into a full-stack AI infrastructure provider from just a server vendor.

In the second quarter of fiscal 2026, SMCI generated $10.7 billion in revenues from the OEM appliance and large data center segment, representing approximately 84% of the top line. This makes SMCI well-positioned to reach a $40 billion revenue goal in fiscal 2026, given its edge in the AI server and storage market.

SMCI’s DCBBS accounted for 4% of SMCI’s profit in the second quarter of fiscal 2026, and the company expects the contribution to rise to double digits by the end of 2026. SMCI’s majority of revenues is now driven by its rack-scale solutions. SMCI, in its second-quarter fiscal 2026, reported that it scaled up to an internal power capacity of 63 megawatts.

SMCI is on track to scale up its rack capacity to 6,000 units per month, including 3,000 direct liquid cooling racks by the end of fiscal 2026 as the demand for these products rises to support AI and HPC workloads with use cases like AI training, enterprise AI inference, visualization and design, content delivery and virtualization and AI edge.

Backed by these strong tailwinds, SMCI has been delivering consistently strong revenue momentum over the past several quarters, underscoring the surging demand for its solutions. In the second quarter of fiscal 2026, SMCI’s top line surged an impressive 122% year over year, highlighting the company’s exceptional growth trajectory.

Competitive and Customer Concentration Pose a Threat to SMCI

SMCI’s revenue streams are heavily dependent on the AI industry, with AI GPU platforms contributing more than 90% of revenues. This exposes SMCI to the boom and bust cycles of a single industry. Since SMCI works in a capex-heavy industry, its inventory has also surged to $10.6 billion in the second quarter of fiscal 2026 from $5.7 billion in the first quarter of fiscal 2026 and $4.7 billion at the end of fiscal 2025.

SMCI generated a negative free cash flow in the second quarter of fiscal 2026, indicating elevated working capital needs to support rapid growth. Super Micro Computer’s working capital problem further stems from the massive operational scale-up required to meet unprecedented AI rack demand. The competition from giants like Hewlett Packard Enterprise HPE and Dell Technologies DELL is adding to SMCI’s challenges.

Hewlett Packard Enterprise offers a range of servers, including HPE ProLiant, HPE Synergy, HPE BladeSystem and HPE Moonshot servers. Dell Technologies has built the Dell AI Factory in collaboration with NVIDIA. Dell Technologies also collaborated with Red Hat Enterprise Linux AI for Dell PowerEdge servers.

To escape the high competition in the server market, SMCI has entered Client, Edge and Consumer AI Markets. The venture into the newer market has brought SMCI to a crossroads with HP Inc., Lenovo LNVGY and Dell Technologies. Dell Technologies has numerous workstations that offer AI capabilities, like XPS 13, Inspiron 14 Plus, Inspiron 14, Latitude 7455 and Latitude 5455.

Lenovo has AI PCs in some versions of ThinkPad, Yoga, IdeaPad and Lenovo Legion. The rising competition across markets has pushed SMCI’s bottom line to a single-digit growth rate despite having double-digit top-line growth. The Zacks Consensus Estimate for SMCI’s fiscal 2026 earnings indicates single-digit percentage growth. Earnings estimates for fiscal 2026 have been revised downward in the past 60 days.

Image Source: Zacks Investment Research

Conclusion: Hold SMCI Stock for Now

Although SMCI is expected to gain from the rapid adoption of AI in the upcoming years, the company’s heavy reliance on a single tailwind and lack of diversification are concerns for the investors. Strong competition from the major industry leaders also poses a threat. Considering these factors, we suggest that investors should retain this Zacks Rank #3 (Hold) stock right now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dell Technologies Inc. (DELL): Free Stock Analysis Report

Super Micro Computer, Inc. (SMCI): Free Stock Analysis Report

Lenovo Group Ltd. (LNVGY): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).