Accenture ACN, through Accenture Ventures, has invested in General Robotics, an AI-native company specializing in general-purpose robotic intelligence. This technology enables organizations to deploy and adapt robots of any type, powered by diverse AI systems, to perform a wide range of tasks. As part of this collaboration, both companies will work together to help manufacturers, logistics providers and other asset-intensive industries accelerate autonomous operations using physical AI.

By leveraging realistic simulations of factories and warehouses, physical AI allows robots to learn and optimize tasks in environments that closely mirror real-world conditions. These simulations also help organizations determine the most efficient configurations for robotic fleets before actual deployment, reducing risks and improving operational readiness.

General Robotics contributes its GRID platform, which provides a unified intelligence layer that connects robots from different manufacturers, enabling scalable, adaptable AI-driven operations. Unlike traditional static programming, GRID emphasizes modular AI capabilities, cloud-based orchestration and simulation-led training while maintaining control over data and intellectual property. Accenture complements this with its deep domain expertise across industries such as manufacturing, logistics, utilities, energy and aerospace. This investment strengthens Accenture’s position in the rapidly evolving physical AI space, enabling it to deliver more advanced automation solutions, enhance operational efficiency for clients and unlock new revenue opportunities through next-generation robotics-driven transformation.

Given this investment, investors may be questioning whether ACN is a buy at present. Let’s take a closer look to address this question.

Factors Supporting ACN

GenAI Growth Outlook Remains Strong

Accenture is experiencing robust growth fueled by AI and is enabling clients to shift their focus from efficiency-driven applications to initiatives centered on growth. A Grand View Research report projects the Generative AI market to grow significantly — from $22.21 billion in 2025 to $324.68 billion by 2033. The phenomenal growth reflects a CAGR of 40.8% in the 2026-2033 timeframe. Strategic alliances with organizations such as OpenAI and Sanctuary AI have reinforced ACN’s standing in the GenAI space. These partnerships grant access to cutting-edge AI models and solutions, allowing ACN to craft tailored offerings suited to specific enterprise requirements.

Apart from the general robotics investment, Accenture recently acquired Keepler Data Tech, a Spanish cloud-native AI and data company. This move enhances Accenture’s ability to support clients across industries in transforming their core business operations through AI-driven solutions built on strong data foundations. More than 240 Keepler professionals will join Accenture as part of the acquisition.

With offices in Madrid, London and Lisbon, Keepler’s team includes technical architects, data scientists, analysts and software engineers. Their expertise will further enhance Accenture’s capacity to scale AI solutions for clients in Spain and across international markets. This acquisition aligns with Accenture’s continued investments in AI to support client transformation.

Accenture also recently acquired Faculty, a prominent UK-based AI firm. This acquisition strengthens its ability to help clients transform key business processes using secure, outcome-oriented AI solutions.

Shareholder-Friendly Approach Is Noteworthy

Dividend-paying stocks are often valued for their ability to provide consistent income and relatively lower volatility compared with non-dividend-paying counterparts. They are widely regarded as reliable tools for long-term wealth generation, particularly during periods of economic uncertainty — conditions that persist today. As such, income-focused investors may find this stock attractive.

Accenture’s solid financial health is evident in its fiscal 2025 free cash flow of $10.9 billion, representing a 26.2% increase year over year. This growth was driven by strong double-digit operating cash flow expansion and disciplined capital expenditure. Such financial strength enables the company to reward shareholders while maintaining strategic flexibility.

During fiscal 2025, Accenture returned $8.3 billion to its shareholders, including approximately $4.6 billion through share buybacks and $3.7 billion in dividends. Last year, the company announced a quarterly dividend of $1.63 per share, marking a 10% increase from the previous rate of $1.48. Over the past five years, Accenture has raised its dividend five times, with a current payout of 49% of earnings.

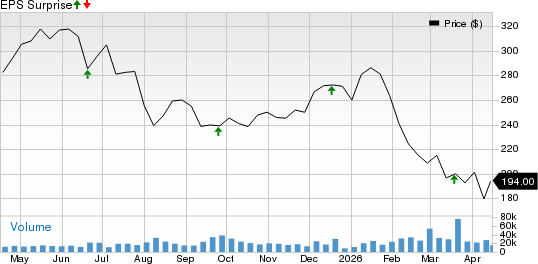

Strong Earnings Track Record

Accenture’s earnings have surpassed the Zacks Consensus Estimate in each of the past four quarters, with an average beat of 3.9%.

Accenture Price and EPS Surprise

Accenture price-eps-surprise | Accenture Quote

Compelling Stock Valuation

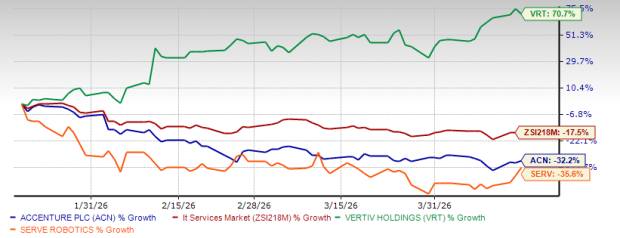

From a valuation perspective, Accenture is trading cheaper than the Zacks Computers – IT Services industry’s average. Going by its price/sales ratio, the company is trading at a forward sales multiple of 1.69, much lower than the industry average of 7.53. ACN’s shares look cheap compared with those of fellow Computers IT Services players like Vertiv Holdings VRT and Serve Robotics SERV. Accenture has a Value Score of B. Vertiv Holdings and Serve Robotics each have a Value Score of F.

ACN's P/S F12M vs. VRT, SERV and the Industry

Key Headwinds That Merit Attention for ACN Stock

Weak Stock Performance

Accenture’s shares have recorded a double-digit decline over the past three months, due to factors like cautious client spending on large-scale IT transformation initiatives, and investor concerns that generative AI may disrupt the traditional consulting business model. The stock has lagged both its industry and Vertiv Holdings. Serve Robotics’ shares have performed worse than Accenture’s in the past three months.

3-Month Price Comparison

Rising Cost Pressures

Elevated talent expenses, caused by a highly competitive labor market, are weighing on consulting firms like Accenture. The sector remains labor-intensive and reliant on global talent pools. Additionally, while automation and AI present significant growth opportunities, they also empower clients to independently adopt performance-enhancing solutions, introducing a degree of uncertainty for consulting providers.

Mature ERP Market

The Enterprise Resource Planning (“ERP”) space has reached a level of saturation, with leading players already capturing the bulk of demand. This environment creates challenges for Accenture by exerting pressure on discretionary IT spending, reducing opportunities for high-margin implementation projects and shifting focus toward lower-margin maintenance services. Furthermore, as clients adopt a more cautious spending approach — delaying or scaling back high-risk or low-return digital initiatives — consulting demand may weaken.

Not the Ideal Entry Point for ACN Stock

Although Accenture is facing short-term challenges such as weak share performance, rising labor costs, ERP market saturation and geopolitical uncertainties, its long-term outlook remains reasonably stable. The company focuses on long-term growth through building a digital core with the help of cloud, data and AI, technology evolution and investment in talent.

Accenture has consistently strengthened its capabilities through acquisitions, particularly in digital technologies and capital projects. Its strong cash position provides flexibility to explore new growth avenues, while its shareholder-friendly policies and solid liquidity offer additional support.

Given these dynamics, holding onto this Zacks Rank #3 (Hold) stock appears prudent at present. However, prospective investors may prefer to wait for a more favorable entry point before initiating a position.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Accenture PLC (ACN): Free Stock Analysis Report

Serve Robotics Inc. (SERV): Free Stock Analysis Report

Vertiv Holdings Co. (VRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).