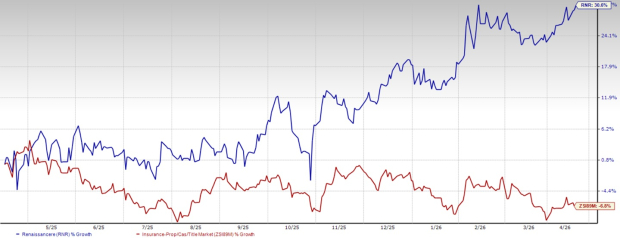

Shares of RenaissanceRe Holdings Ltd.RNR have gained 30.6% in the past year against the industry’s decline of 6.8%.

RenaissanceRe, primarily providing property-catastrophe reinsurance to insurers and reinsurers globally based on excess of loss. RNR is well poised for growth driven by its disciplined underwriting, expanding fee-based income, resilient investment returns and strong capital management. RenaissanceRe's strong cash generation ability and strategic acquisitions further support its long-term expansion.

Image Source: Zacks Investment Research

The insurer has a market capitalization of $13.5 billion. The average volume of shares traded in the last three months was 0.4 million.

RNR's shares have outperformed those of a few other players from the industry. American Financial Group, Inc. AFG has gained 2.6%, while Kinsale Capital Group, Inc. KNSL and Selective Insurance Group, Inc. SIGI have lost 26% and 9.3%, respectively, in the past year.

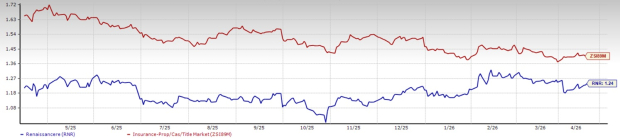

Attractive Valuation of RNR

RNR’s shares are trading at a discount compared with the industry. Its trailing 12-month price-to-book value of 1.24X is lower than the industry average of 1.40X, the Finance sector’s 4.06X and the Zacks S&P 500 composite’s 8.19X. The company has a Value Score of A.

Image Source: Zacks Investment Research

RNR’s Growth Projection

The Zacks Consensus Estimate for RNR’s 2026 earnings per share is pinned at $38.38 indicating, a year-over-year decrease of 1.8%. The consensus estimate for revenues is pegged at $11.4 billion, implying a year-over-year decrease of 1.5%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 10.4% and 0.7%, respectively, from the corresponding 2026 estimates.

Earnings of RNR grew 58.4% in the past five years, better than the industry average of 22.5%. The expected long-term earnings growth rate is 11.4%. It delivered an earnings surprise in the past three reported quarters.

Average Target Price for RNR Suggests Upside

Based on short-term price targets offered by 16 analysts, the Zacks average price target is $328.69 per share. This average suggests a potential 6.6% upside from the last closing price.

RNR Holdings’ Favorable Return on Capital

Return on equity in the trailing 12 months was 18.29%, which compared favorably the industry’s 7.3%. This reflects its efficiency in utilizing shareholders’ funds.

The return on invested capital ("ROIC") has been increasing over the last few quarters as the company raised the capital investment over the same time frame, reflecting its efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 8.8%, better than the industry average of 5.7%.

RNR’s Growth Drivers

A diversified business model, growing fee income and disciplined portfolio management continue to act as key catalysts supporting RNR’s growth trajectory. RenaissanceRe has been witnessing steady premium growth over the past few years, propelled by growth in the Property and Casualty segments. RNR delivered strong premium growth over 2021-2024. However, the metric declined 1.9% in 2025, due to reductions in the general casualty line.

RenaissanceRe's acquisition of Validus Re and related businesses from AIG enhanced the scale of its global property and casualty reinsurance business and improved diversification, underwriting reach and earnings power. Management doesn’t shy away from divesting non-core assets to streamline its operations. This enhanced diversification improves resilience to large loss events and supports more consistent long-term returns.

Management emphasized disciplined underwriting, retaining targeted lines at key renewals and building a portfolio designed to generate returns well above the cost of capital. RNR has been getting rid of low-return, high-risk businesses. The company sold off the U.S.-based weather and weather-related energy risk management unit to shield itself from the associated uncertainties.

RenaissanceRe plans to drive shareholder value through several strategic levers, including expanding its property business, growing fee income through third-party capital partnerships, increasing invested assets and maintaining active share repurchases. Combined with ongoing technology investments to enhance underwriting analytics, these initiatives position the company to continue growing book value and delivering strong returns over time.

RNR’s robust cash generation abilities have enabled it to continue enhancing shareholder value through share buybacks and dividend payouts. In the fourth quarter of 2025, the company rewarded its shareholders with share buybacks of $650.5 million. From Jan. 1 to Jan. 30, 2026, it repurchased shares worth $113.4 million.

Risks for RNR Stock

There are some factors that investors should keep a careful eye on.

RenaissanceRe has witnessed a significant increase in operating expenses, driven by higher claims, acquisition costs and operational outlays. Total expenses surged 44.4% in 2024 and rose a further 1.5% in 2025, while the combined ratio changed from 77.9% in 2023 to 87.2% in 2025, indicating a shrinking share of premiums retained after covering claims.

As of Dec. 31, 2025, RenaissanceRe carried $2.3 billion in debt, with a total debt-to-capital ratio of 16.7, above the industry average of 15.4. Elevated debt levels have increased interest expenses, which rose 28.1% year over year in 2024 and 35% in the fourth quarter of 2025. This growing interest burden could weigh on margins

Conclusion

RNR is well-poised for growth, driven by its diversified earnings structure across underwriting income, fee income and investment income. The company's strong cash generation ability and strategic acquisitions and partnerships further support its long-term expansion. But rising expenses and continued high debt load are the concerns.

RNR has a VGM Score of A. Stocks with a favorable VGM Score are those with the most attractive value, best growth and most promising momentum compared with peers.

RenaissanceRe should continue to benefit from an impressive dividend history, strategic acquisitions and attractive valuations, as well as favorable return on capital. It is, therefore, wise to hold on to this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

RenaissanceRe Holdings Ltd. (RNR): Free Stock Analysis Report

American Financial Group, Inc. (AFG): Free Stock Analysis Report

Selective Insurance Group, Inc. (SIGI): Free Stock Analysis Report

Kinsale Capital Group, Inc. (KNSL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).