Abercrombie & Fitch Co. ANF continues to navigate a challenging cost environment as tariff pressures emerge as a central factor influencing profitability. While the company has demonstrated resilience through disciplined cost management and strategic sourcing adjustments, rising trade-related expenses remain a key concern for investors. With tariffs affecting product costs and supply-chain dynamics, the company’s ability to sustain its track record of double-digit operating margins is now under close scrutiny.

The financial impact of tariffs is already evident in the company’s recent performance. In fourth-quarter fiscal 2025, ANF reported an operating margin of 14.1% despite facing approximately 360 basis points of tariff pressure during the period. For the full year, operating margin stood at 12.5%, reflecting a 250-basis-point decline year over year, largely due to around $90 million in tariff-related expenses. Looking ahead to fiscal 2026, management expects an additional $40 million in incremental tariff costs, equivalent to roughly 70 basis points of margin pressure, underscoring the persistent nature of this headwind.

To mitigate these pressures, ANF has implemented a series of strategic actions across its sourcing and pricing functions. The company has diversified its sourcing network across more than a dozen countries, negotiated supplier terms and selectively adjusted pricing in certain fashion-focused categories. These initiatives, combined with disciplined inventory control and improved freight efficiencies, are expected to offset part of the tariff burden. Notably, management highlighted that modest average unit retail expansion and lower freight costs could help stabilize gross margins as the year progresses.

Despite ongoing challenges, ANF’s operating model has historically demonstrated durability across shifting macroeconomic environments. The company has delivered double-digit operating margins for multiple consecutive years, even amid inflationary pressures and supply-chain disruptions. However, maintaining this performance will depend on effective execution, continued demand strength and the successful implementation of cost-mitigation strategies. If tariffs remain elevated longer than anticipated, sustaining double-digit profitability could become increasingly difficult, making this a critical metric for investors to monitor in upcoming quarters.

ANF’s Zacks Rank & Share Price Performance

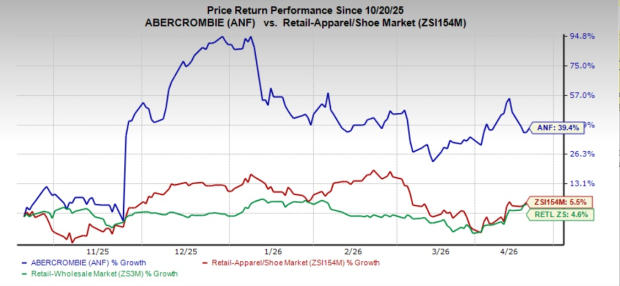

Shares of this Zacks Rank #2 (Buy) company have gained 39.4% in the past six months compared with the industry and the broader Retail-Wholesale sector, which rose 5.5% and 4.6%, respectively.

ANF Stock's Past Six-Month Performance

Image Source: Zacks Investment Research

Is ANF a Value Play Stock?

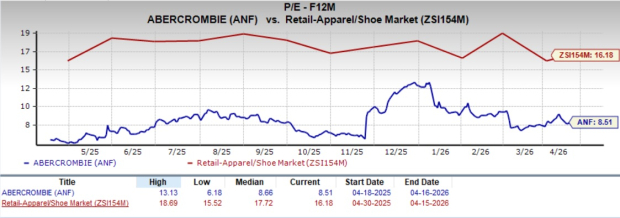

ANF currently trades at a forward 12-month P/E ratio of 8.51X, which is lower than the industry average of 16.18X and notably below the sector average of 25.38X. This valuation positions the stock at a modest discount relative to both its direct peers and the broader consumer staples sector.

ANF P/E Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Other Stocks to Consider

We have highlighted three other top-ranked stocks in the retail space, namely, FIGS Inc. FIGS, Deckers Outdoor Corporation DECK and Tapestry, Inc. TPR.

FIGS is a direct-to-consumer healthcare apparel and lifestyle brand, and it currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FIGS’ current financial-year sales indicates growth of 11.8% from the year-ago reported number. The company delivered a trailing four-quarter earnings surprise of 187.5%, on average.

Deckers is a leading designer, producer and brand manager of innovative, niche footwear and accessories. It carries a Zacks Rank #2 at present. DECK delivered a trailing four-quarter average earnings surprise of 36.9%.

The Zacks Consensus Estimate for Deckers’ current fiscal-year earnings and sales indicates growth of 8.5% and 8.9%, respectively, from the year-ago actuals.

Tapestry, which was formerly known as Coach, Inc., is the designer and marketer of fine accessories and gifts for women and men in the United States and internationally. It currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for Tapestry’s current fiscal-year earnings and sales implies growth of 26.5% and 11.2%, respectively, from the year-ago actuals. TPR delivered a trailing four-quarter average earnings surprise of 12.8%.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF): Free Stock Analysis Report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

FIGS, Inc. (FIGS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).