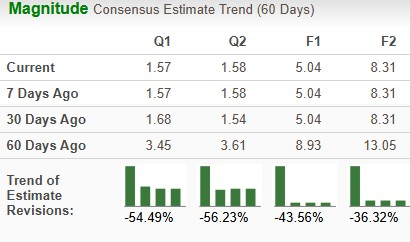

Molina Healthcare, Inc. MOH, a healthcare plan provider, is set to report first-quarter 2026 results on April 22, after the closing bell. The Zacks Consensus Estimate for earnings is currently pegged at $1.57 per share and the same for revenues is pinned at $10.95 billion.

The bottom-line projection indicates a year-over-year decrease of 74.2% and the top-line estimate implies a decline of 1.7%. The first-quarter earnings estimate has witnessed three downward revisions and no upward movement over the past 60 days.

Image Source: Zacks Investment Research

For full-year 2026, the Zacks Consensus Estimate for revenues is pegged at $43.98 billion, implying a decline of 3.2% year over year. Also, the consensus mark for 2026 earnings per share is pegged at $5.04, indicating a decrease of 54.3%.

Molina Healthcare beat the consensus estimate in one of the trailing four quarters and missed in the other three, delivering an average negative surprise of 197.5%. This is depicted in the figure below.

Molina Healthcare, Inc Price and EPS Surprise

Molina Healthcare, Inc price-eps-surprise | Molina Healthcare, Inc Quote

Q1 Earnings Whispers for MOH

Our proven model does not conclusively predict earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat, which is not the case here.

MOH has an Earnings ESP of +22.69% but a Zacks Rank #5 (Strong Sell) at present. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

What’s Shaping MOH’s Q1 Results?

The Zacks Consensus Estimate for premiums indicates a decline of 4.1% year over year, while our model estimate suggests a 2.8% decrease, due to lower contribution from Medicaid and Marketplace. Yet, the consensus estimate for Medicare premiums is pinned at $1.5 billion, up 5.3% year over year.

The consensus mark indicates a 5% year-over-year decrease in Medicaid membership, while MOH’s Medicare membership is projected to witness 8% drop. The Zacks Consensus Estimate for Marketplace membership suggests a 57.7% year-over-year decrease.

The consensus mark for the medical care ratio (MCR) in Marketplace is pegged at 82.3%, up from 81.7% a year ago. The consensus mark for total MCR is pinned at almost 91.5%, up from 89.2% a year ago. The Zacks Consensus Estimates for Medicaid MCR is pegged at 92.3%, up from the year-ago figure of 90.3%.

Moreover, the Zacks Consensus Estimate for investment income indicates a 6.6% decline year over year. The factors mentioned above are expected to make earnings beat uncertain.

Stocks That Warrant a Look

While an earnings beat looks uncertain for Molina, here are some companies from the broader Medical space that can be considered, as our model shows that these have the right combination of elements to post an earnings beat this time around:

Agenus Inc. AGEN has an Earnings ESP of +7.69% and a Zacks Rank #1 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Agenus’ bottom line is pegged at $1.95, indicating 289.3% year-over-year growth. AGEN has witnessed one upward revision against no downward movement over the past 60 days. The consensus mark for Agenus’ revenues is pegged at $ 129.50 million, implying an approximate 483% increase from that posted a year ago.

The Ensign Group, Inc. ENSG has an Earnings ESP of +1.12% and a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Ensign’s bottom line is pegged at $1.79, calling for 17.8% year-over-year growth. ENSG has witnessed one upward revision against no downward movement over the past 60 days. The consensus mark for Ensign’s revenues is pegged at $1.39 billion, implying an 18.5% increase from the year-ago level.

Centene Corporation CNC has an Earnings ESP of +18.89% and a Zacks Rank of 3.

The Zacks Consensus Estimate for Centene’s bottom line has remained stable over the past 60 days. CNC has beaten earnings estimates in three of the last four quarters and missed once. Revenues for the upcoming reported quarter are projected to be around $47.47 billion.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Molina Healthcare, Inc (MOH): Free Stock Analysis Report

Centene Corporation (CNC): Free Stock Analysis Report

Agenus Inc. (AGEN): Free Stock Analysis Report

The Ensign Group, Inc. (ENSG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).