Taiwan Semiconductor Manufacturing Company Limited (TSM) has once again demonstrated solid proof of sitting at the center of the global AI boom. The chipmaking giant delivered a blockbuster first quarter, with net profit surging 58% year-over-year (YOY) and comfortably beating expectations as demand for advanced semiconductors continues to accelerate.

The strength was driven by an insatiable appetite for cutting-edge chips, particularly 3nm nodes used in artificial intelligence (AI) workloads, where demand is not only strong but also still exceeding available supply. Major customers, including hyperscalers and AI leaders, are locking in capacity months in advance, reinforcing Taiwan Semi’s pricing power and long-term visibility.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Importantly, management signaled that this momentum is far from peaking. The company raised its 2026 outlook and now expects revenue growth of more than 30%, while committing to elevated capital spending to expand capacity and capture the next leg of AI-driven demand.

Still, the market response has been more muted than the headline numbers suggest. Despite record earnings and bullish guidance, the stock dipped following the release, highlighting investor concerns around capacity constraints, heavy capital spending, and the sustainability of AI-driven growth.

About Taiwan Semiconductor Manufacturing Company Stock

Founded in 1987, TSMC pioneered the pure-play foundry model and has since grown into the world’s leading dedicated semiconductor foundry, supplying advanced logic, specialty, and packaging services to a wide range of global customers. Headquartered in Hsinchu, Taiwan, TSM operates multiple fabs both in Taiwan and overseas, including in the U.S., China, and other parts of Asia and Europe. TSM’s market cap is around $1.92 trillion, placing it among the world’s most valuable technology companies.

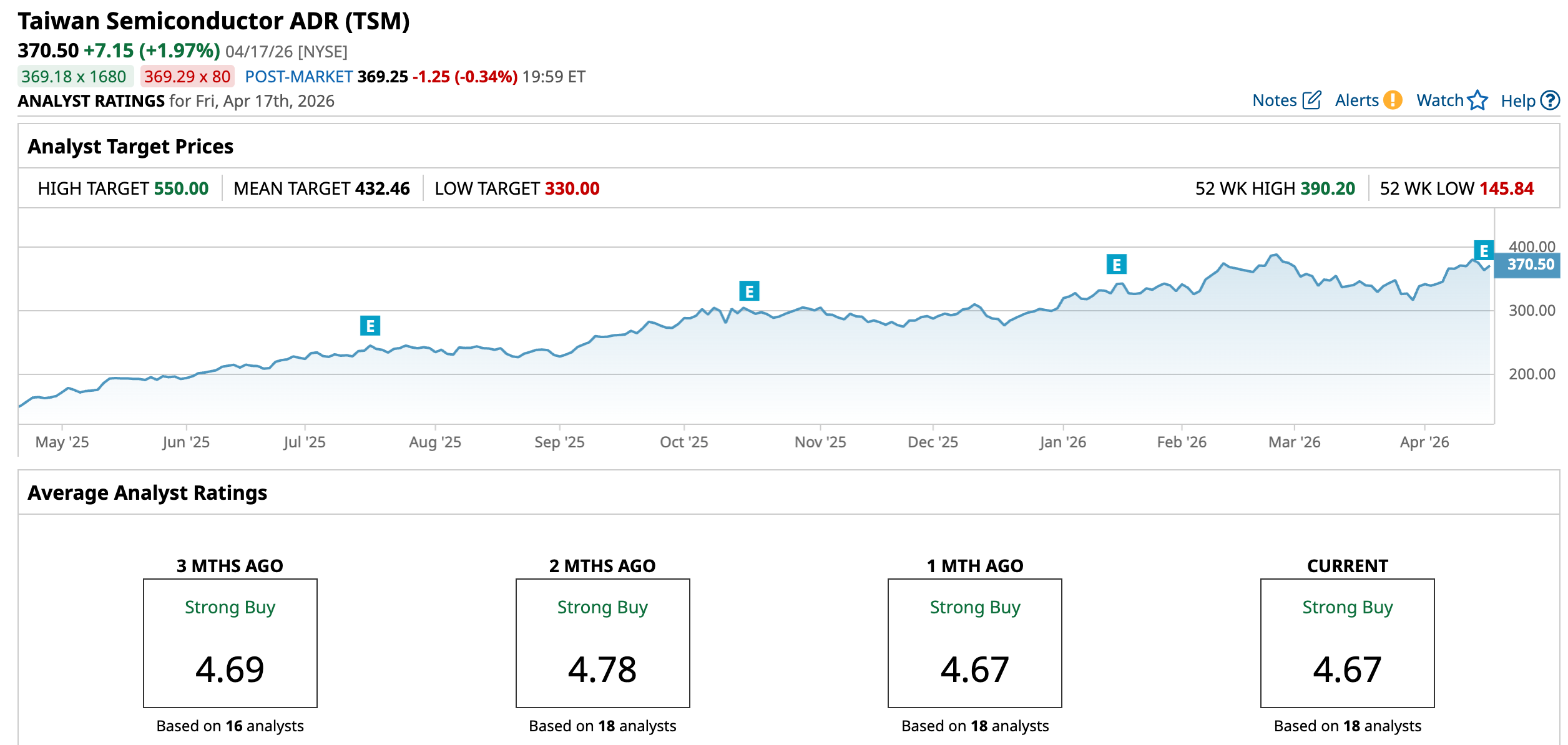

Taiwan Semiconductor’s stock has been a standout performer over the past year, but the recent price action highlights a growing tension due to elevated expectations.

The stock is up 144.17% over the past 52 weeks, reflecting its central role in the AI supply chain and sustained demand for advanced-node chips. The stock is just 5% below its 52-week high of $390.20, reached on Feb. 25.

Year-to-date (YTD), momentum remains firmly positive, though less explosive. TSM is up 21.92% in 2026, supported by continued AI-driven optimism.

More recently, the post-earnings reaction tells a more nuanced story. Despite reporting a 58% profit surge and raising its outlook, TSM shares fell about 3.1% intraday on Apr. 16, following the results, reflecting concerns around capacity constraints, heavy capex, and whether AI demand is already fully priced in.

www.barchart.com

www.barchart.com Regarding valuation, TSM now trades at a discount, with its forward price-to-earnings ratio of 25.79 times.

On the other hand, its stature is further boosted by a consistent history of paying quarterly cash dividends. Its current payout equates to $0.95 with an annual dividend forward of $2.97, which works out to a yield of 0.79%.

Robust Bottom Line Growth

Taiwan Semiconductor Manufacturing Company reported its first-quarter 2026 results on Apr. 16. The company generated revenue of $35.9 billion, representing a 40.6% YOY increase, a sharp acceleration from the prior-year base as AI and high-performance computing demand scaled meaningfully.

Net income rose even faster, reaching NT$572.5 billion, up 58.3% YOY, marking a record level. Its EPS reached NT$22.08 ($3.49 per ADR unit), up 58.3% YOY from NT$13.94.

Gross margin reached 66.2%, while operating margin was at 58.1%, supported by stronger utilization and pricing power in leading-edge nodes.

The mix of revenue continues to tilt heavily toward these advanced technologies, with 3nm, 5nm, and 7nm nodes accounting for roughly 74% of wafer revenue, a significantly higher contribution than in prior years, while AI-driven high-performance computing now represents the majority of total revenue.

Furthermore, management provided robust guidance that reinforces the durability of its growth. For the second quarter of 2026, TSMC expects revenue in the range of $39 billion to $40.2 billion, implying continued strong growth both sequentially and on a YOY basis. More importantly, the company raised its full-year 2026 outlook, now guiding for revenue growth of over 30%, supported by sustained AI demand and continued expansion in advanced-node capacity.

Analysts remain optimistic as they predict EPS to be around $14.62 for fiscal 2026, up 37.28% YOY, before surging by another 25.10% annually to $18.29 in fiscal 2027.

Wall Street’s Bullish Bet on Taiwan Semiconductor Manufacturing

DA Davidson reiterated a “Buy” rating on Taiwan Semiconductor Manufacturing with a $450 price target following a strong Q1 2026 report that beat expectations.

Moreover, Needham raised its price target on TSM to $480 from $410 while maintaining a “Buy” rating, following a strong Q1 2026 beat and improved guidance. Needham remains bullish on sustained AI demand and resilient high-end smartphone sales.

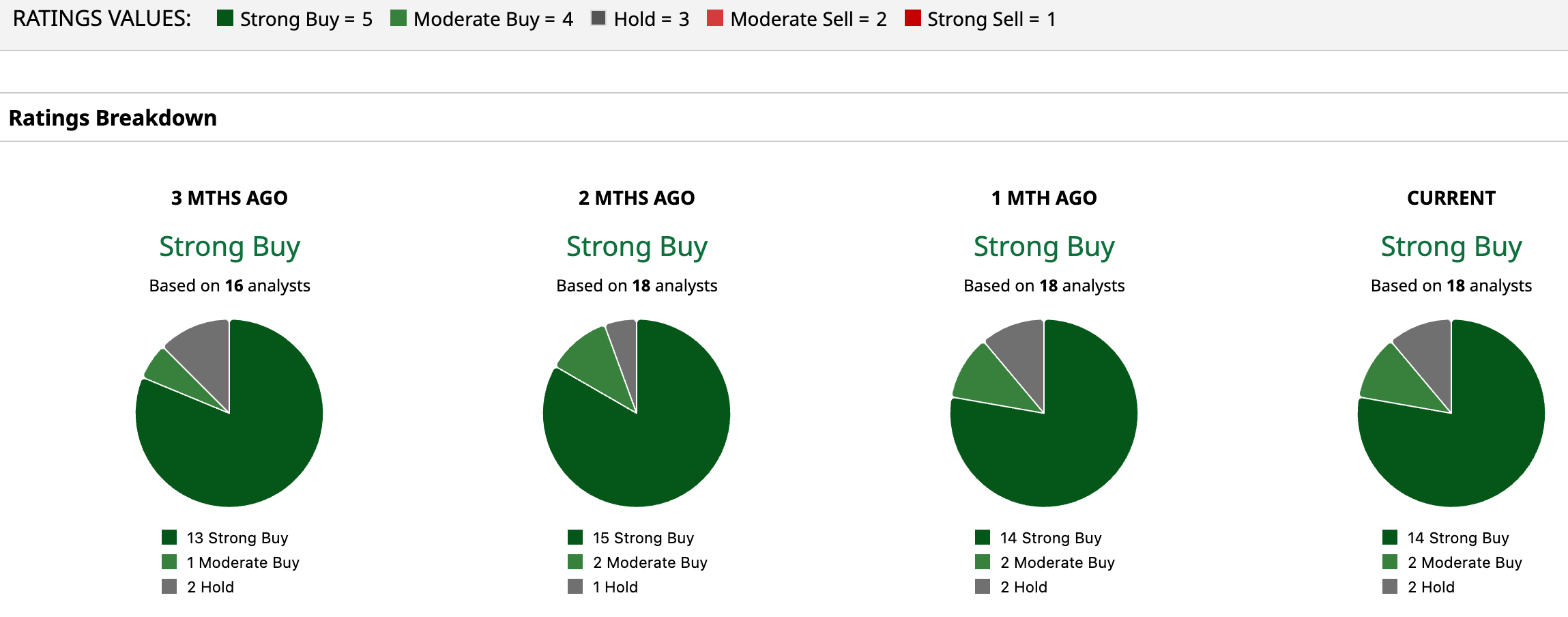

Analysts are highly bullish on TSM stock overall, with a “Strong Buy” consensus rating. Out of the 18 analysts with coverage, 14 recommend a “Strong Buy,” two advise a “Moderate Buy,” and two analysts maintain a “Hold” rating.

The mean price target of $432.46 indicates an upside of 16.7%. Meanwhile, the Street-high target of $550 indicates that the stock can rally as much as 48.5% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Profit Jumped 58% at Taiwan Semi. Does That Make TSM Stock a Buy Here? Dear Seagate Technology Stock Fans, Mark Your Calendars for April 28 Netflix’s Q1 Dip Is a Buying Opportunity—Here’s the Bull Case ANET, FN, CIEN: Why These 3 Data Center Stocks Are Top Buys This Earnings Season