Artificial intelligence (AI) is expanding rapidly, but a key challenge is making those capabilities work in secure, restricted environments where data cannot leave. Many government and regulated organizations need cloud and AI tools that operate securely in closed, controlled environments. And that’s becoming a big deal.

NetApp (NTAP), a company that businesses store, manage, and move massive amounts of data smoothly across systems and the cloud, is back in the spotlight, thanks to a deeper partnership with Alphabet's (GOOGL) Google Cloud.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The two companies have signed a four-year deal to bring NetApp’s storage solutions into Google Distributed Cloud (GDC), a sovereign cloud platform. The partnership aims to bring enterprise-grade AI and storage capabilities directly to where data resides, supporting secure and compliant operations. With Google also expanding AI features on GDC, including advanced models, the opportunity looks promising.

As NetApp deepens its role in this evolving space, investors are left weighing the potential. So, does this partnership strengthen the long-term case, or is caution still warranted around NTAP stock?

About NetApp Stock

Founded in 1992 and based in San Jose, California, NetApp has evolved from a traditional storage provider into an intelligent data infrastructure company. It helps organizations manage, protect, and use data seamlessly across on-premise systems and multiple clouds. At the core is its ONTAP platform, which powers a unified data environment with built-in automation, security, and scalability.

Operating through Hybrid Cloud and Public Cloud segments, NetApp helps businesses run applications efficiently while maintaining consistent performance and control. With a growing focus on AI and data-driven innovation, the company plays a key role in helping enterprises turn data into a strategic asset. Its market capitalization currently stands at $20.6 billion.

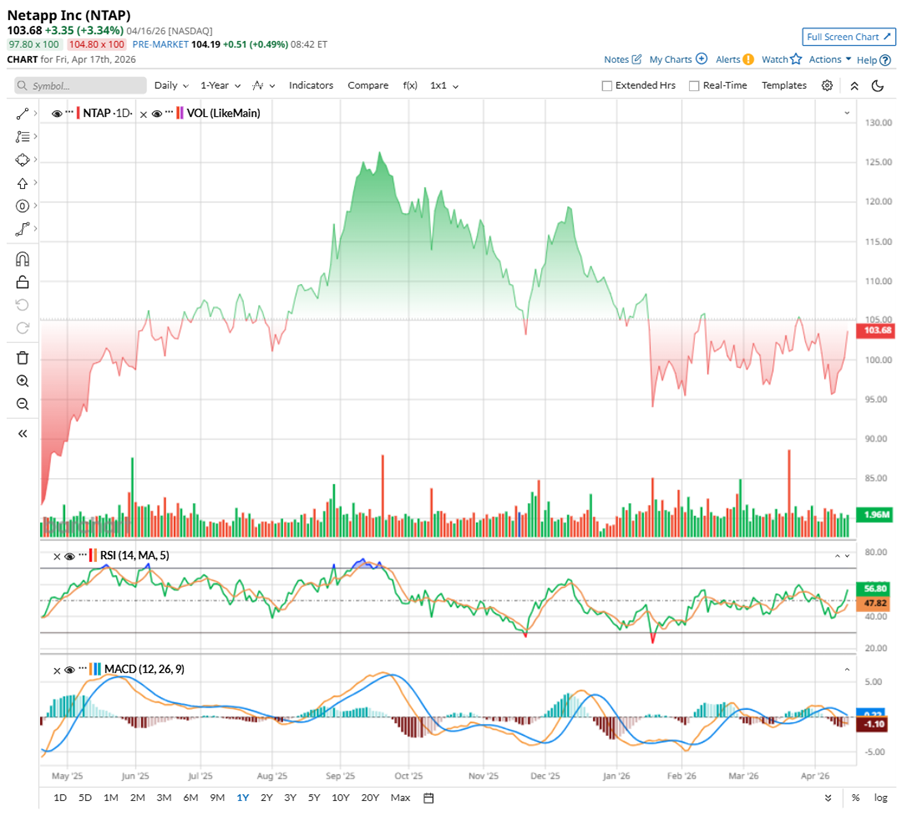

Shares of the intelligent data infrastructure company have had a mixed but evolving run, telling a story of resilience with signs of a turnaround. Over the past 52 weeks, the stock has gained about 27%, climbing nearly 30% from its last year’s April low of $80.64. Nevertheless, the journey has not been smooth. Over the past six months, shares slipped 12.2%, and 2026 started on a slightly weak note, with the stock down 2.39% year-to-date (YTD).

But the tone is beginning to shift. Over the past month, NTAP has edged up 2.56%, and in just the last five days, it has jumped 8.96%, signaling renewed momentum. Part of this rebound came after NetApp announced a strategic partnership with Commvault last month, combining AI-driven ransomware detection with advanced recovery tools. At the same time, the company rolled out its next-gen EF-Series storage systems, delivering a sharp 250% performance boost for AI and high-performance workloads. A deeper collaboration with Google Cloud also helped lift sentiment.

Technically, the mood is shifting. The 14-day RSI, which had slipped into oversold territory back in January, has now climbed to 58.33 and is steadily moving higher, suggesting the selling pressure that weighed on the stock is beginning to fade. Meanwhile, trading activity is flashing more green, pointing to a pickup in buying interest.

However, it is not a full green light yet. The MACD oscillator suggests caution, with the MACD line slipping below the signal line and the histogram dipping into negative. Even so, this looks more like a transition phase than a reversal breakdown.

www.barchart.com

www.barchart.com When we look at NTAP’s valuation, it feels quite grounded. The stock is priced at around 15.49 times forward earnings and about 3.02 times sales, both sitting below peers and even its own historical levels, which makes it look relatively inexpensive.

What really adds a layer of comfort here is consistency. NetApp has been paying dividends for over a decade, and right now, it offers about $2.08 per share annually, translating to a 1.99% annualized yield – well above the State Street SPDR S&P 500 ETF Trust’s (SPY) 1.04% yield.

Plus, with a payout ratio of 33.68%, there is still plenty of room to grow, making it a reliable pick for passive income seekers looking for steady returns alongside long-term value.

NetApp Beats Q3 Numbers

On Feb. 26, NetApp reported its fiscal third-quarter 2026 results. While revenue came in at $1.7 billion, up 4.4% year-over-year (YOY), non-GAAP EPS rose 11% annually to $2.12 – both ahead of expectations. Growth was consistent, driven by strong demand for all-flash storage, solid traction in cloud services, and increasing relevance in enterprise AI.

Digging a little deeper, the core business looks healthy. The Hybrid Cloud segment grew 5% YOY to $1.54 billion, while the Public Cloud segment revenue held steady at $174 million. All-Flash Array revenue stood out, rising 11% annually to $1 billion, now running at a $4.2 billion annual pace. Meanwhile, total billings increased 10% to $1.89 billion, marking nine straight quarters of growth.

Also, future visibility improved, with deferred revenue hitting $4.63 billion and remaining performance obligations climbing 14% annually to $5.11 billion.

Financially, NetApp stayed disciplined. It ended the quarter with $3 billion in cash and cash equivalents, generated $317 million in operating cash flow, and delivered $271 million in free cash flow. In addition, it returned $303 million to shareholders via dividends and share repurchases, showing confidence in its steady, cash-generating model.

Looking ahead, the outlook remains solid. For the fourth quarter of fiscal 2026, management expects revenue to land between $1.795 billion and $1.945 billion, with non-GAAP EPS in the range of $2.21 to $2.31. For the full year, the company has raised its expectations, now guiding revenue between $6.772 billion and $6.922 billion. Non-GAAP EPS is projected to be between $7.92 and $8.02, reflecting stronger confidence in growth compared to earlier estimates.

Meanwhile, analysts tracking NetApp estimate Q4 fiscal year 2026 EPS to grow 20.5% YOY to $1.88. For the full fiscal year 2026, the bottom line is expected to surge 11.9% annually to $6.48 per share, followed by another 9.4% YOY increase in fiscal 2027 to $7.09 per share.

What Do Analysts Expect for NetApp Stock?

NetApp is seeing a more cautious view from Samik Chatterjee at JPMorgan, who recently downgraded the stock to “Neutral” from “Overweight” and cut the target to $110 from $125. The concern is simple – growth drivers are slowing while costs are rising.

NetApp’s earlier boost from its All-Flash products is losing momentum, and newer offerings may take time to scale. At the same time, sharp increases in memory prices are expected to pressure margins, potentially trimming profitability. JPMorgan now sees mid-single-digit revenue growth ahead, with earnings growth moderating, even though the company still maintains strong margins and cash flow.

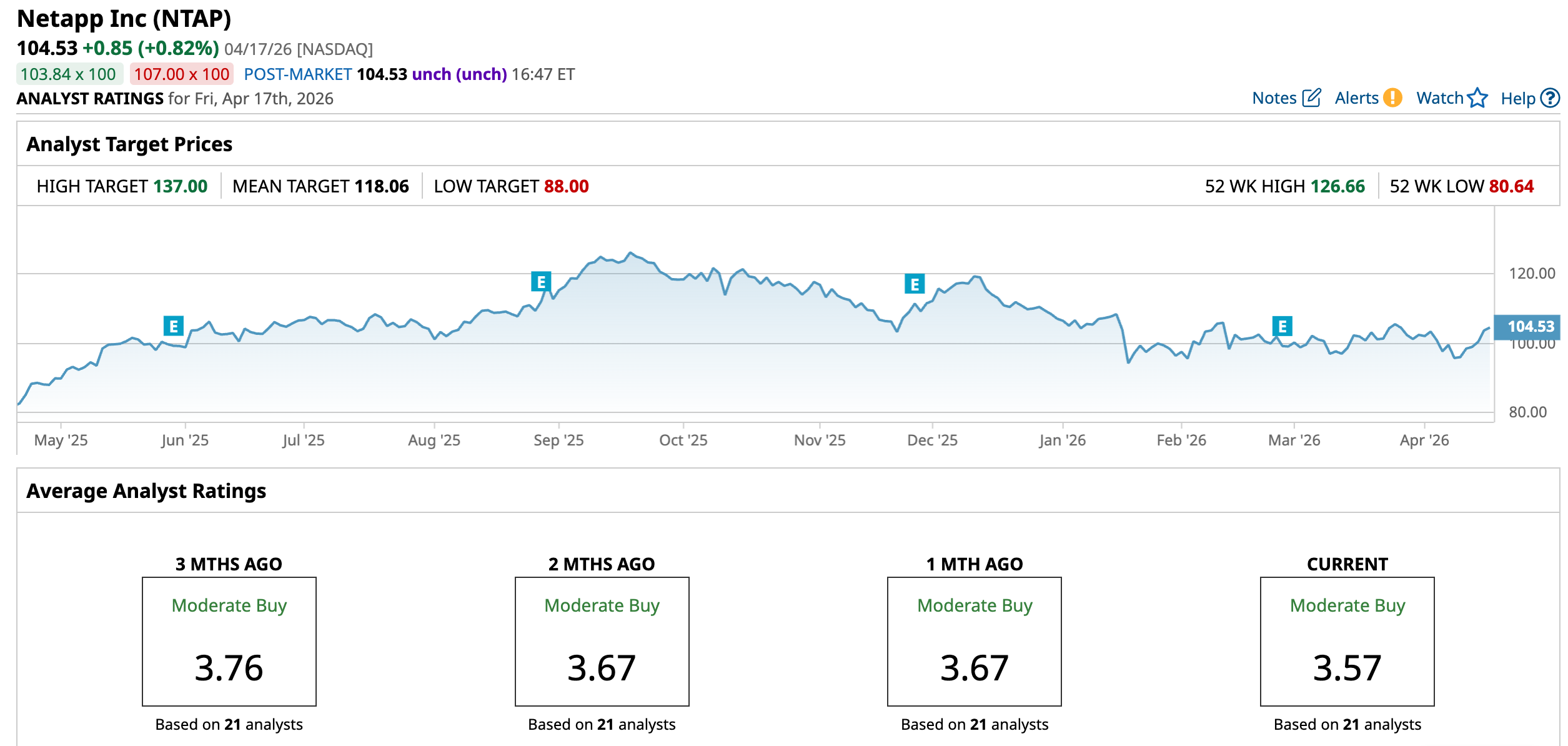

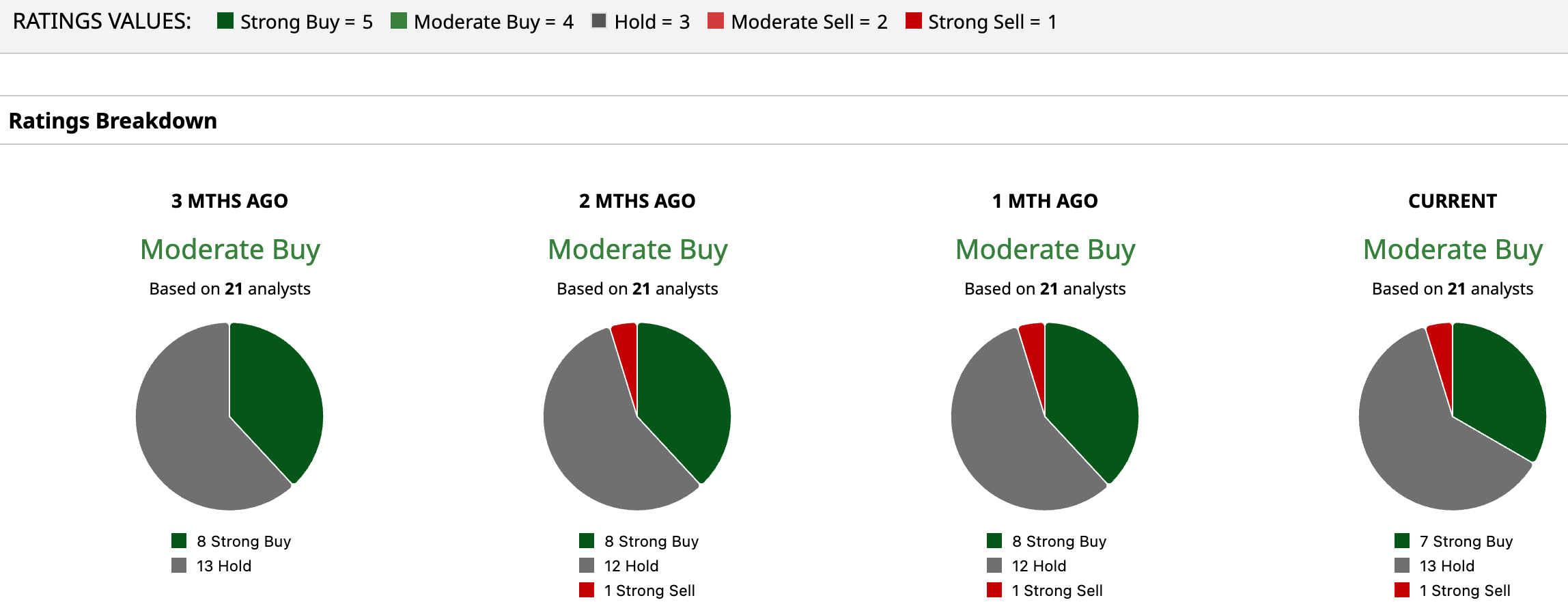

Overall, analysts are upbeat about NTAP’s growth potential with a dash of caution, giving the stock a consensus rating of “Moderate Buy.” Of the 21 analysts covering the stock, seven advise a “Strong Buy,” 13 recommend a “Hold,” and only one suggests a “Strong Sell.”

The average analyst price target for NTAP is $118.06, indicating potential upside of 12.9%. The Street-high target price of $137 suggests that the stock could rally as much as 36.1% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Final Thoughts on NTAP Stock

NetApp’s story right now feels balanced. On one side, the company continues to execute well – steady quarterly growth, improving backlog visibility, strong cash flows, and a disciplined capital return strategy all highlight solid operational strength. Its reach is also hard to ignore, with roughly 84% of Fortune 500 companies relying on its solutions, reinforcing its relevance in enterprise data infrastructure.

Plus, NTAP stock trades at relatively modest multiples, while its dividend yield offers a steady income cushion, something not always common in tech. Plus, the expanded tie-up with Google Cloud strengthens its AI positioning.

Yet, there are a few watch points. Analysts like the JPMorgan flag cautions.

Overall, NTAP sits at an interesting point – supported by strong fundamentals and long-term potential, but with near-term challenges that could keep expectations in check.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As NetApp Expands Its Relationship With Google Cloud, Should You Buy, Sell, or Hold NTAP Stock? Alibaba Just Launched New AI Models for Video Games. Does That Make BABA Stock a Buy? Netflix Generates Massive FCF and FCF Margins - NFLX Price Targets Are Higher Dear Seagate Technology Stock Fans, Mark Your Calendars for April 28