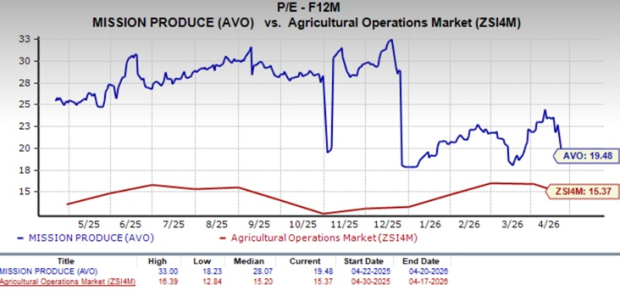

Mission Produce, Inc. AVO has recently gained momentum, supported by progress on strategic initiatives aimed at deepening customer relationships, and expanding across products and global markets. However, the company’s current forward 12-month price-to-earnings (P/E) multiple of 19.48X raises concerns about whether the stock's valuation is justified. This multiple is significantly higher than the Zacks Agricultural - Operations industry average of 15.37X, making the stock appear relatively expensive.

The price-to-sales ratio of Mission Produce is 0.79X, above the industry’s 0.56X. This adds to investor unease, suggesting that it may not be a strong value proposition at the current levels.

Image Source: Zacks Investment Research

AVO’s Premium Valuation Surpasses Peers

At 19.48X P/E, Mission Produce trades at a significant premium to its industry peers. The company’s peers, such as Archer Daniels Midland Company ADM, Dole Plc DOLE and Adecoagro AGRO, are delivering solid growth and trade at more reasonable multiples. Archer Daniels, Corteva and Adecoagro have forward 12-month P/E ratios of 15.34, 10.49X and 9.66X — all significantly lower than that of AVO.

The AVO stock currently seems somewhat overvalued, and a premium valuation may suggest that investors have strong expectations for its growth.

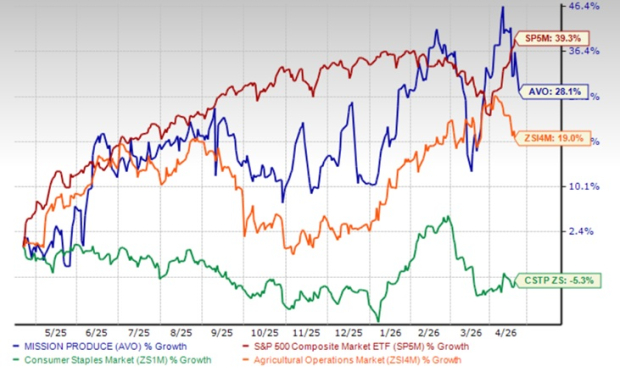

In the past year, the company’s shares have rallied 28.1%, outperforming the broader Agricultural - Operations industry’s growth of 19% and the Consumer Staples sector’s fall of 5.3%. The stock has underperformed the S&P 500’s growth of 39.3% in the same period.

AVO’s 1-Year Stock Return

Image Source: Zacks Investment Research

Mission Produce’s performance is notably stronger than its competitors. The stock has outperformed Adecoagro and Dole, which have risen 9.7% and 3.2% in the past year, respectively. However, AVO has underperformed Archer Daniels, which has rallied 41.1% in the past year.

The company’s stock momentum and a premium valuation suggest that investors have high expectations for AVO's future performance and growth potential.

The company’s capability to execute its strategy and capitalize on a favorable pricing environment is essential for ensuring profitability and consistent performance in its Marketing and Distribution segment. While success in these areas can strengthen market leadership, failure can pose serious challenges for AVO.

Mission Produce’s current share price of $13.42 is 13.6% below its 52-week high mark of $15.53 and 34.2% above its 52-week low of $10. AVO trades above its 200-day moving averages, indicating a bullish sentiment.

AVO Stock Trades Above 200-Day Moving Averages

Image Source: Zacks Investment Research

What’s Driving AVO’s Momentum?

Mission Produce’s momentum is driven by a combination of strong operational execution, favorable category trends and expansion initiatives. Despite a challenging pricing environment, the company delivered a solid performance by focusing on volume growth and per-unit margins, core drivers of its business model. Avocado volumes grew 14%, margins expanded and adjusted EBITDA increased, highlighting effective cost and supply management even as revenues declined due to lower prices.

A key contributor is the strength of AVO’s Marketing and Distribution segment, wherein improved customer relationships, disciplined pricing and higher volumes led to a 33% increase in segment EBITDA. At the same time, long-term demand tailwinds remain robust, supported by rising avocado consumption, increased household penetration and growing health-conscious trends among consumers.

Operationally, AVO is enhancing asset utilization through its International Farming segment by diversifying produce handling and improving efficiency, while its blueberries business continues to scale despite short-term yield pressures. Strategically, the pending Calavo acquisition is a major catalyst, expected to expand supply reliability, introduce product categories and generate significant cost synergies.

Together, these factors, execution discipline, structural demand growth and strategic expansion, are reinforcing AVO’s positioning and driving sustained momentum.

Mission Produce’s Estimate Revision Trend

The Zacks Consensus Estimate for AVO’s fiscal 2026 and 2027 EPS was unchanged in the last 30 days. For fiscal 2026, the Zacks Consensus Estimate for AVO’s sales and EPS implies year-over-year declines of 15.9% and 15.2%, respectively. The consensus mark for fiscal 2027 sales and earnings suggests year-over-year growth of 5.4% and 6%, respectively.

Image Source: Zacks Investment Research

AVO’s Investment Rationale

Mission Produce presents a compelling growth story, backed by strong operational execution, favorable demand trends and strategic expansion initiatives. The stock’s recent momentum and bullish technical indicators reflect investor confidence in its long-term potential. However, its premium valuation relative to peers raises concerns about limited upside at the current levels.

While initiatives like the Calavo acquisition and volume-driven growth could sustain performance, much of the optimism appears priced in. Going forward, consistent execution and margin stability will be critical. Investors may find AVO attractive for growth exposure, but should remain cautious, given its elevated valuation. The company currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Archer Daniels Midland Company (ADM): Free Stock Analysis Report

Dole PLC (DOLE): Free Stock Analysis Report

Adecoagro S.A. (AGRO): Free Stock Analysis Report

Mission Produce, Inc. (AVO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).