The artificial intelligence (AI) boom created one of the most extraordinary stock market winners in history. Nvidia (NVDA) has evolved from just a gaming/niche GPU company into the backbone of the AI revolution, now holding the “AI King” crown firmly. It delivered massive gains of 22,648% over the last decade that many investors now regret missing. But markets do not only provide one chance. Investors who believe they arrived late to the Nvidia boom may get a second shot with Advanced Micro Devices (AMD). While it is not comparable to Nvidia, it has the potential to be very strong in its own way.

Valued at $448.2 billion, AMD stock is up 33% year-to-date (YTD), compared to the tech-led Nasdaq Composite Index ($NASX) gain of 4.7% YTD.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Is AMD Where Nvidia Was a Few Years Ago?

AMD is not the dominant player today. But it is growing, gaining adoption, and expanding its product lineup, and is still in the process of scaling its AI business. This is very similar to where Nvidia stood before its explosive growth phase. In 2025, AMD’s revenue grew 34% year-over-year (YoY) to $34.6 billion, driven by growth in data centers, AI, PCs, gaming, and embedded systems. Adjusted earnings rose 26% to $4.17 per share. The data center segment, which is directly tied to AI infrastructure, grew 39% YoY to $5.4 billion. Even for Nvidia, the data center segment is what powered its meteoric rise.

AMD’s MI350 series are the chips that are designed specifically for AI workloads, including training and running large models. It is also expanding its software ecosystem using ROCm, which allows millions of AI models to operate efficiently on its hardware. AMD expects its AI business to grow substantially, with yearly revenue reaching tens of billions by 2027. This forecast indicates that AMD is still early in its AI monetization cycle.

The Power of Being the “Second Player”

Unlike Nvidia in its early AI days, AMD is entering an industry where demand is already established and fast-growing. Nvidia had to prove the AI market. But AMD does not have to. Being the second player could work in AMD's favor. The global AI infrastructure opportunity is anticipated to be $498 billion by 2034. Hyperscalers and enterprises are rapidly expanding their infrastructure to support the massive AI workloads. AMD claimed that cloud providers significantly increased deployments, with over 500 AMD-based instances built in 2025 alone and approximately 1,600 EPYC cloud instances currently operational.

Notably, AMD’s EPYC CPUs are increasingly seen as the processor of choice for modern data centers due to their performance and efficiency. Furthermore, rising CPU prices across the industry could act as a meaningful tailwind for AMD. According to reports, AMD is planning a 10% to 15% price hike, which will give it pricing power at a time when demand for high-performance computing and AI infrastructure is surging.

AMD is also deepening its partnerships, including its recent multi-generation partnership with OpenAI and Meta (META) involving large-scale GPU deployments. These types of contracts create predictable demand and recurring revenue. Additionally, its new platforms, like Helios and future MI400 and MI500 series chips, are already generating strong customer interest. These new products are expanding its reach with major cloud providers, enterprise customers, and system manufacturers.

This is probably why AMD trades at a relatively high multiple compared to Nvidia. Currently, AMD is valued at 38 times forward earnings, compared to Nvidia at 23x forward earnings. However, this premium also reflects expectations for AMD’s future growth. Analysts project AMD’s earnings to increase by 60.4% in 2026, followed by 61.9% in 2027. While AMD might be the cheaper option to buy now, the AI market is highly competitive and evolving rapidly. In its path to success, the stock could face volatility.

Why AMD Could Be the Second Chance?

While Nvidia still holds the crown, it probably has already delivered its biggest gains. It is now a dominant, mature AI leader with expectations priced into its stock. However, AMD is still in the early stages of scaling its AI business. AMD expects its data center segment to grow more than 60% annually over the next three to five years. At the same time, it is targeting overall revenue growth of more than 35% annually over that period. The company also has a long-term goal of generating more than $20 in annual earnings per share. It is gearing itself for sustained multi-year growth powered by AI. But it could take time for the company to reach the level of dominance or market saturation that Nvidia has.

Investors willing to accept some risks along the way, AMD could indeed be the second chance to participate in the next stage of the AI revolution while the story is still unfolding.

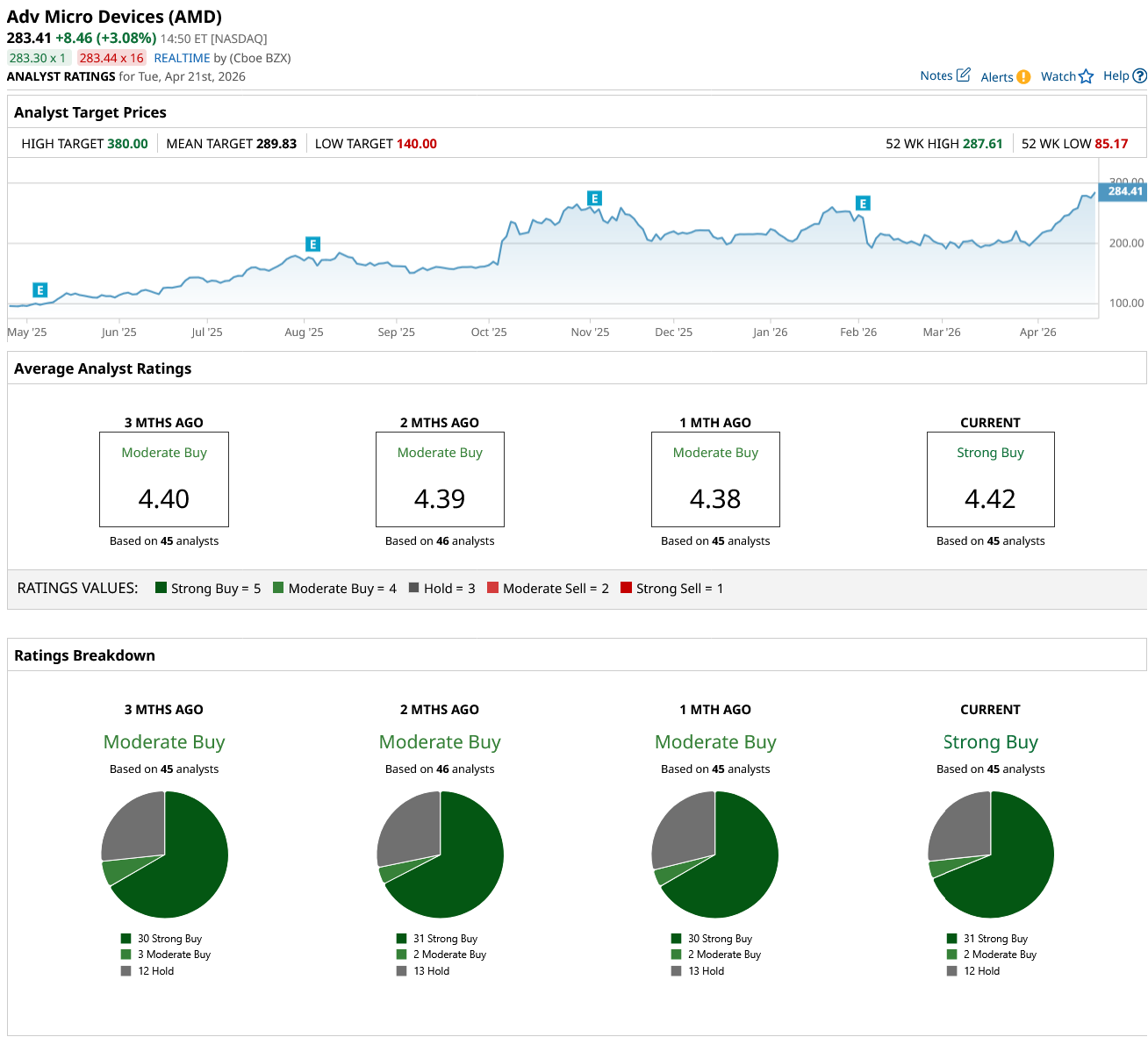

Overall, Wall Street says AMD stock is a “Strong Buy.” Of the 45 analysts covering the stock, 31 rate it a “Strong Buy,” two rate it as a “Moderate Buy,” and 12 rate it a “Hold.” The stock has an average target price of $288.83, which it is just shy of. Plus, the high price estimate of $380 suggests the stock has an upside potential of 34% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Missed Nvidia? AMD Could Be Your Second Chance to Earn Massive AI Gains TSLA Stock Catalyst: Get Ready for a Larger Model Y After the Blue Origin Satellite Failure, Is It Time to Sell AST SpaceMobile Stock? As Lam Research Joins the Tesla Terafab, Should You Buy, Sell, or Hold LRCX Stock?