Tesla’s (TSLA) first-quarter results exceeded consensus expectations, but the market reaction suggests that near-term operational strength is not enough to sustain the stock’s bullish narrative. While the company showed growth across its core automotive and ancillary segments, investor attention remains firmly anchored on longer-term growth catalysts, areas with limited visibility.

In Q1, Tesla reported revenue of $22.4 billion, a 16% year-over-year (YoY) increase that surpassed analysts’ estimates. Its adjusted earnings per share (EPS) rose 52% YoY to $0.41, exceeding expectations.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Tesla’s Q1 benefited from an increase in vehicle deliveries, improved average selling prices, and continued expansion in the Services segment. Additionally, lower material costs contributed to a decline in average production costs per vehicle, supporting its bottom line during the quarter.

Demand indicators were also encouraging. Tesla exited the quarter with its strongest Q1 order backlog in more than two years, suggesting resilient underlying demand. External macro factors, particularly rising gasoline prices, have boosted order momentum, strengthening the value proposition of electric vehicles (EVs) in a higher fuel-cost environment.

Despite these positives, the investment narrative for Tesla extends well beyond its automotive business. The company’s valuation premium is driven by its emerging technology verticals, including AI, energy storage solutions, autonomous driving software, and humanoid robotics. These segments offer the potential for higher-margin revenue streams and could significantly diversify Tesla’s earnings profile over time. However, they remain largely developmental and offer no near-term financial contribution.

While Tesla continues to invest aggressively in these growth initiatives, meaningful revenue from them is unlikely before 2027 at the soonest. In the interim, elevated capital expenditure is expected to pressure free cash flow.

As a result, even strong quarterly execution wasn’t enough to support Tesla’s bull case.

www.barchart.com

www.barchart.com Robotaxi Rolling Out and FSD Penetration Improving, But...

Tesla continues to position its Robotaxi initiative as a long-term growth driver, with recent developments indicating steady operational progress. The company is investing in supporting infrastructure required to scale autonomous ride-hailing while gradually expanding both fleet size and geographic coverage.

Operational metrics are improving, with paid Robotaxi miles nearly doubling sequentially. At the same time, Tesla has expanded its unsupervised driving footprint by broadening service areas in Austin and initiating unsupervised rides in Dallas and Houston as of April. These moves indicate growing confidence in the underlying autonomous stack.

Adoption of Full Self-Driving (FSD) software is also gaining traction. Tesla now reports approximately 1.3 million paid FSD users globally, with subscription uptake driving the majority of recent growth. Regulatory momentum is building as well, highlighted by newly secured approvals in the Netherlands, which could serve as a stepping stone toward broader EU authorization in the near term. Parallel efforts in China remain ongoing, and successful clearance there would represent a meaningful catalyst given the size of Tesla’s installed base in the region. Increased regulatory acceptance should enable deeper software penetration across existing vehicles while also supporting incremental demand for new units.

Despite this progress, the Robotaxi segment still remains in the investment phase. Revenue contribution is expected to be immaterial in the near term, as the company continues to refine its technology, expand operational domains, and navigate regulatory frameworks.

While operational metrics and adoption trends are improving, the market will likely require more concrete evidence of scalable deployment of these offerings.

Optimus Humanoid Robot Has Solid Potential

Tesla continues to position its Optimus humanoid robot as a long-term growth driver, with CEO Elon Musk emphasizing its potential to become the company’s most significant product line. Musk has previously outlined an ambitious production target of up to 100,000 units per month within five years.

While the opportunity is substantial, investors should temper expectations regarding near-term financial impact. The project remains in early development, with no meaningful contribution to revenue or margins expected in the foreseeable future.

TSLA Stock: The Valuation Concern

Tesla’s valuation is another limiting factor. Tesla currently trades at 286.6 times its forward earnings, reflecting an enormous premium relative to peers. Even with analysts projecting strong 38% EPS growth for 2027, the valuation suggests that much of the optimism is already priced in.

The Bottom Line

Tesla delivered a solid Q1 performance. Solid automotive demand, cost efficiencies, and early traction in software adoption are encouraging.

However, these near-term positives fall short of substantiating the magnitude of expectations priced into the stock. Much of Tesla’s valuation remains anchored in its prospective leadership across autonomy, AI, energy storage, and robotics. While these segments offer substantial long-term growth opportunities, they are still in early stages of commercialization and lack consistent, material financial contribution.

Until clearer evidence emerges that Tesla’s future initiatives can translate into sustainable revenue and margin expansion, its bull case lacks fuel.

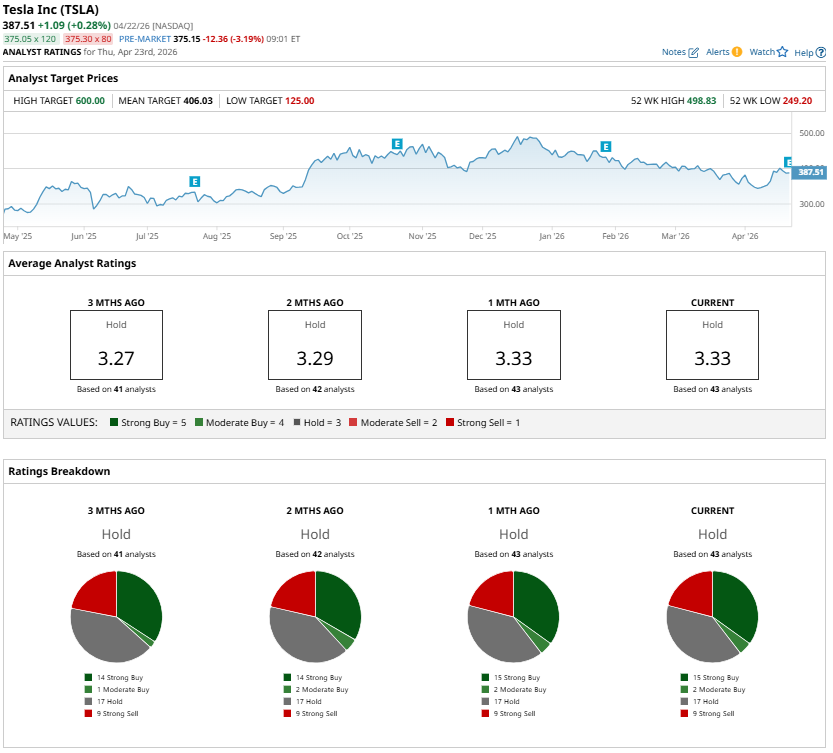

Analysts maintain a cautious stance, with a “Hold” consensus rating on TSLA stock.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Is Arm Stock a Buy at New All-Time Highs? Should You Buy the Dip in IBM Stock Today? Uber Has an 11.52% Stake in Lucid. Does That Make LCID Stock a Buy? Wall Street Can’t Seem to Get Enough of Intel Stock