Iridium Communications IRDM reported earnings per share (EPS) of 20 cents for the first quarter of 2026, missing the Zacks Consensus Estimate by 25.9%. The bottom line also compared unfavorably with the prior-year quarter's figure of 27 cents.

Quarterly revenues reached $219.1 million, representing a 2% increase from the previous year, driven by rising demand for Iridium’s mission-critical services. Management emphasized that the company is investing in next-generation IoT platforms, PNT, aviation safety and national security—all high-value segments with long growth runways. The Zacks Consensus Estimate was pegged at $220.2 million.

The standout element remains Service revenue, which contributed $158 million (72% of total revenue), a strong indicator of the company’s recurring revenue model. This recurring nature is critical. Satellite communications businesses benefit from long-term contracts and the use of embedded infrastructure, making their revenue streams more predictable. Iridium’s consistent service growth highlights resilience in a competitive and capital-intensive industry.

The commercial segment remains Iridium’s main source of revenue, accounting for 60%. Commercial service revenue increased 2% to $130.4 million, meeting IRDM’s forecast, driven by growth in commercial IoT along with voice and data services during the quarter. Government service revenue increased slightly in the first quarter to $27.6 million, primarily due to the final phase of the EMSS contract, which was implemented last September.

Iridium Communications Inc Price, Consensus and EPS Surprise

Iridium Communications Inc price-consensus-eps-surprise-chart | Iridium Communications Inc Quote

Commercial broadband declined 5% year over year, reflecting ongoing customer migration to backup services. Revenue from hosting and other data services decreased about 1% to $14.8 million, primarily because of the timing of payments from an existing non-PNT customer. Our estimates for total commercial and government service revenues were $129.9 million and $26.4 million, respectively.

Subscriber equipment sales totaled $20.2 million in the first quarter, broadly in line with expectations, down 12.6% year over year. The drop in equipment sales reflects cyclical demand, which management expects to normalize over the full year. We projected the figure to be $21.5 million.

Engineering and support revenues surged 9% to $40.8 million, led by Iridium’s expanding work with the Space Development Agency, reinforcing its emphasis on growth driven by national security programs. Our estimate was $42.4 million.

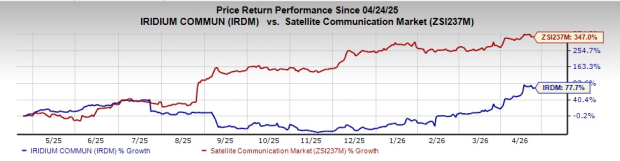

In the past year, shares have gained 77.7% compared with the Zacks Satellite and Communication industry's growth of 347%.

Image Source: Zacks Investment Research

Other Details

Total operating expenses were $168.3 million compared with $154.5 million in the prior-year quarter, primarily due to higher depreciation and amortization costs and selling, general and administrative expenses.

Operational EBITDA (OEBITDA) decreased 5% year over year to $116.3 million. The decline was largely due to a change in compensation structure, shifting to fully cash-based incentives. This added about $4.2 million in expenses for the quarter.

Operating income came in at $50.7 million compared with $60.4 million reported in the year-ago quarter.

Iridium ended the first quarter with 2,555,000 billable subscribers, up 5% year over year, driven primarily by commercial IoT growth. Commercial IoT now represents 83% of commercial subscribers, reinforcing Iridium’s strategy of serving industrial, maritime, aviation, oil & gas, mining and asset-tracking markets.

Liquidity

As of March 31, 2026, total cash and cash equivalents were $111.6 million, with $1.7 billion of net debt. Capital expenditures were $30 million in the quarter under review.

On March 31, 2026, Iridium paid a 15-cent dividend per share, continuing its track record of annual dividend increases since 2023, a positive signal for income-focused investors.

2026 Outlook: Stability With Strategic Investments

Iridium reiterated its full-year guidance. For 2026, service revenue is expected to be flat to up 2%, reflecting continued IoT growth offset by moderation elsewhere, following 2025 service revenue of $634 million.

Iridium expects 2026 OEBITDA of $480–$490 million compared with $495.3 million reported in 2025. The guidance includes a roughly $17 million hit from paying incentive compensation fully in cash rather than a mix of cash and equity. Excluding this accounting change, 2026 OEBITDA is likely to be $497–$507 million, indicating no underlying operational deterioration.

IRDM projects a pro forma free cash flow of about $318 million for 2026.

IRDM’s Zacks Rank

Iridium currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Recent Performance of Other Companies

Badger Meter, Inc. BMI reported EPS of 93 cents for first-quarter 2026, which missed the Zacks Consensus Estimate by 22.5%. The bottom line compared unfavorably with the year-ago quarter’s EPS of $1.30. Quarterly net sales were $202.3 million, down 9% from $222.2 million in the year-ago quarter due to delayed project deployments and weaker-than-expected short-cycle order activity. The Zacks Consensus Estimate was pegged at $230.1 million.

Simulations Plus, Inc. SLP reported second-quarter fiscal 2026 adjusted earnings of 35 cents per share, surpassing the Zacks Consensus Estimate by 29%. The bottom line also compared favorably with the prior-year quarter’s 31 cents. Simulations Plus reported quarterly revenue of $24.3 million, marking an 8% year-over-year increase. This growth reflects continued demand for its core offerings, especially in drug discovery and development.

BlackBerry Limited BB reported fourth-quarter fiscal 2026 non-GAAP earnings per share (EPS) of 6 cents. The figure beat the company’s estimate of 3-5 cents. In the year-ago quarter, it reported a non-GAAP EPS of 3 cents. The Zacks Consensus Estimate was pegged at 5 cents per share. BlackBerry reported quarterly revenue of $156 million, surpassing the top end of its guidance ($138-$148 million), driven by stronger-than-expected sales across both its QNX and Secure Communications divisions. Revenue also increased 10% year over year.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Badger Meter, Inc. (BMI): Free Stock Analysis Report

Simulations Plus, Inc. (SLP): Free Stock Analysis Report

Iridium Communications Inc (IRDM): Free Stock Analysis Report

BlackBerry Limited (BB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).