Dell Technologies (DELL) isn’t operating in an easy enterprise spending environment right now. IT budgets are still tight in some pockets, a messy tariff situation keeps everyone guessing, and the company is trying to manage explosive growth in AI servers while margins in that part of the business stay thin.

Now Dell’s stock just got a fresh Street-high price target. Bank of America raised its target to $246 from $205, pointing to agentic AI as the next big demand driver. That’s not automatically a reason to buy hand over fist, but it does add another layer of conviction around a stock that does not need much more of it.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Why This Analyst Upgrade Matters for Dell

Dell is a massive infrastructure company that sells everything from AI-optimized servers to storage arrays and commercial laptops. Its agentic AI workloads are still in their early innings, and a lot of the hype has not yet turned into steady, high-margin recurring revenue. Bank of America believes that the wave is coming.

The firm’s analysts see agentic AI as the catalyst that will keep orders flowing deep into fiscal 2027. That matters because Dell already closed $64 billion in AI-optimized server orders in its last fiscal year and is sitting on a $43 billion backlog. If the thesis plays out, the current valuation could end up looking modest.

How Did Dell Stock Perform?

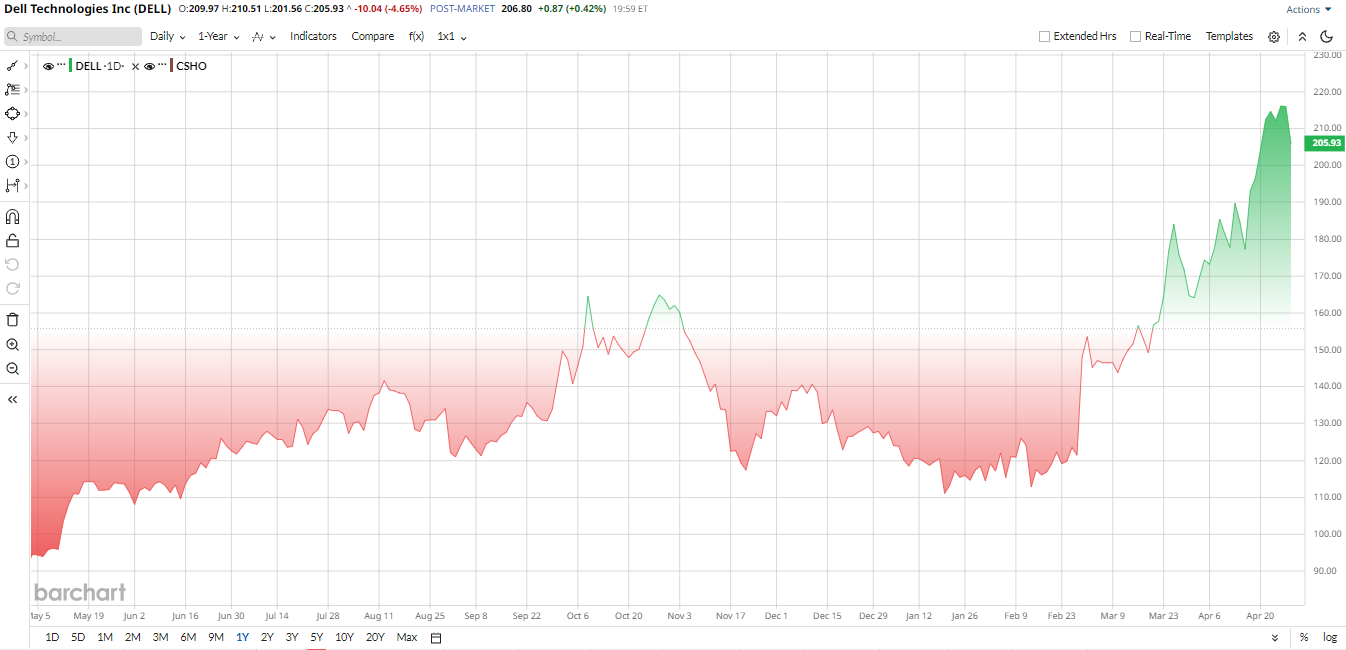

After a choppy 2025, DELL shares have roared higher in 2026, up 63% year-to-date (YTD) as of late April. The rally has been fueled by record AI server orders, improving enterprise demand, and a string of analyst upgrades. Investors who held through the volatility are now sitting on a 12-month gain of over 117%.

Despite the huge run, DELL stock does not look extreme in either direction. Dell has a market capitalization of roughly $150 billion. The stock trades at roughly 24 times trailing earnings, which sits below the median for many high-growth technology hardware names.

The thing is that the market is not treating Dell as a high-flying software name, but it is also not pricing in a severe slowdown. You are not getting a deep bargain, but you are also not paying an absurd premium for a business generating record free cash flow.

www.barchart.com

www.barchart.com Dell’s Business Is Soaring, Backed by AI Infrastructure

It is important not to downplay the momentum here. Dell’s latest quarter was neither clean nor easy to parse, but the headline numbers were staggering.

In fiscal Q4 2026, which ended Jan. 30, net revenue came in at $33.4 billion, up 39% year-over-year (YoY). The Infrastructure Solutions Group drove the bus, posting revenue of $19.6 billion, a 73% jump. Within that silo, AI-optimized server revenue hit $9 billion, up a breathtaking 342%. The Client Solutions Group, the PC business, grew 14% to $13.5 billion, proving that even the legacy part of the company is finding its footing.

That is clearly the kind of growth investors want to see, and it shows the business is generating enormous scale. Adjusted earnings per share of $3.89 beat expectations and rose 45% YoY. The company generated $4.7 billion in free cash flow during the quarter alone.

For the full year, operating cash flow hit $11.2 billion. In short, Dell is a functioning infrastructure giant with the financial firepower to return capital to shareholders while still investing aggressively.

Management Is Pushing an Aggressive Growth and Capital Return Plan

The more interesting part of the story is what management is doing next.

Earlier this year, Dell announced a 10 billion share buyback program and committed to raising its dividend by at least 10% annually through 2030. That multi-year pledge is a loud signal of confidence in free cash flow generation.

The company also deepened its partnership with Nvidia (NVDA), launching new AI-ready desktops, the AI Data Platform, and becoming the first OEM to ship the Nvidia GB300 desktop superchip for autonomous AI agents. To keep the organization streamlined, Dell cut about 10% of its workforce, a move aimed at rightsizing without sacrificing the growth engines.

Vice Chairman and COO Jeff Clarke framed the year in confident terms, calling it a defining chapter. He pointed to record full-year revenue of $113.5 billion, record EPS, and record cash generation, and stressed that the AI opportunity is transforming the company.

Management guided for fiscal 2027 revenue of around $140 billion at the midpoint, with EPS growing about 25%. That outlook lines up with the building consensus on Wall Street and gives analysts a reason to stay bullish.

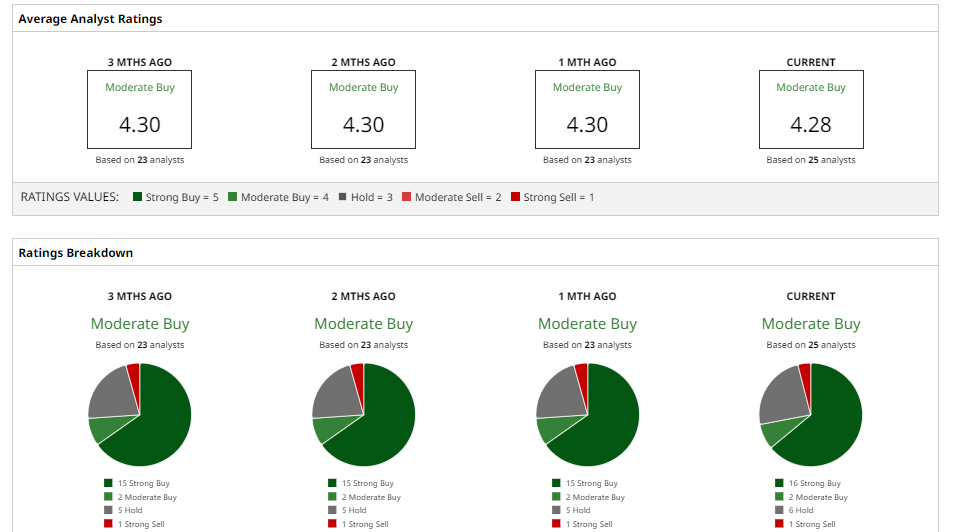

What Do Analysts Think of DELL Stock?

Wall Street is leaning heavily positive, though one notable name remains cautious. Bank of America’s $246 target is the new high-water mark, carrying a “Buy” rating. Evercore ISI raised its target to $240 with an “Outperform” rating, citing a $1.4 billion AI infrastructure deal with Boost Run as proof that enterprise demand is turning into longer-term commitments.

On the other side, Citigroup lifted its target to $235 and also rated the stock a “Buy.” Morgan Stanley is the outlier, raising its target to just $110 but maintaining an “Underweight” rating, citing concerns about margins and the sustainability of the current mix shift.

The overall analyst view, when you average it all together, lands at a consensus "Moderate Buy" rating. The mean price target stands at roughly $184, which DELL has already surpassed. At the current share price near $207, the new Street-high target from Bank of America implies about 19% upside. So if you believe agentic AI is the next real infrastructure wave, DELL stock still looks like a name worth owning.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Your Smartphone Could Soon Be an AI Agent, and Qualcomm Stock Is Positioned to Profit Big Dell Stock Just Got a New Street-High Price Target. Should You Buy Shares Here? Broadcom Just Hit $2 Trillion Market Cap. Is AVGO Stock a Buy Now? Should You Buy the Dip in Robinhood Stock Today?