Monday’s trading was lower on concerns about the troubles in the Middle East and the Strait of Hormuz flaring up.

The Dow took the hardest hit, down 1.13% on the day, followed by the S&P 500 (-0.41%) and the Nasdaq Composite (-0.19%).

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

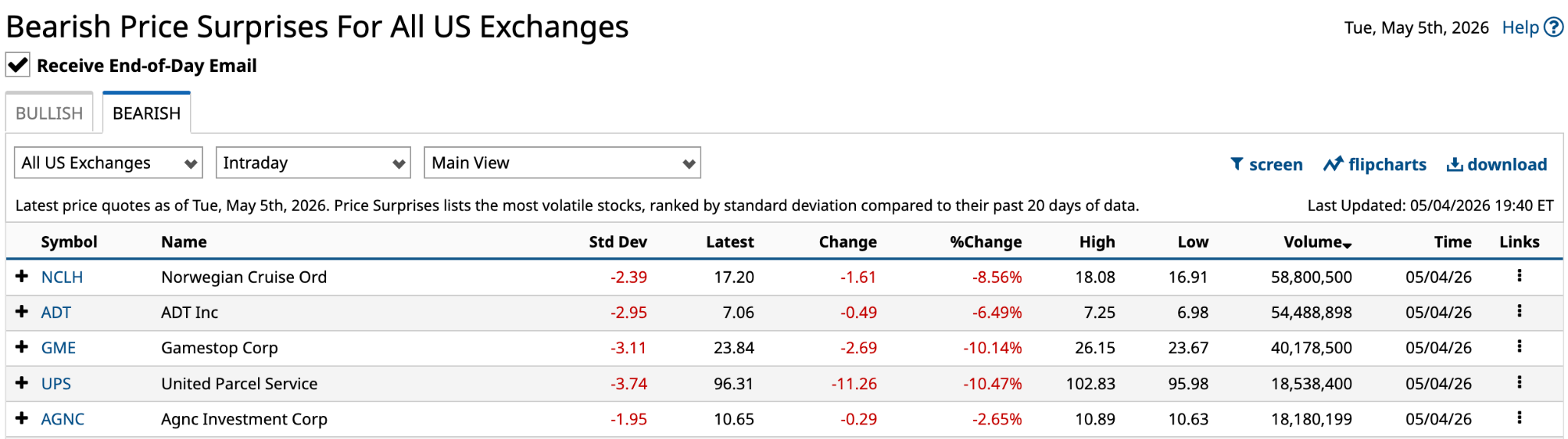

The resulting red across the board led many well-known names to make Barchart’s top 200 bearish price surprises. Ranked by volume, the five names appearing below all experienced significant declines on the day.

Of the five, GameStop (GME) got the most press yesterday after it made an unsolicited $56 billion cash-and-stock offer to buy eBay (EBAY). The $125-a-share bid for the e-commerce marketplace is a 20% premium to Friday’s closing price.

Is GameStop or any of the other four names worth buying at current prices? I’ll consider each of these bearish price surprises.

Norwegian Cruise Line Holdings (NCLH)

Norwegian Cruise Line Holdings (NCLH) lost 8.56% on Monday on volume of nearly 59 million, 2.7 times its 30-day average. Its shares are down 22.9% in 2026.

You don’t have to be a rocket scientist to know why the cruise operator’s shares are down nearly 23% in 2026. The Strait of Hormuz and the war in the Middle East have sent oil prices rocketing higher. Cruise ships aren’t exactly Honda Civics when it comes to fuel consumption. And their tanks require fill-ups of more than $100 at the local gas station.

Its two largest publicly traded competitors -- Carnival (CCL) and Royal Caribbean Cruises (RCL) -- have lost 16% and 7%, respectively, year to date. They’re all struggling with higher fuel prices.

NCLH reported Q1 2026 results yesterday. The part that killed the share price was the 32% downward revision in its 2026 earnings per share guidance to $1.62 from $2.38 previously.

The Barchart Technical Opinion is a 100% Strong Sell. Meanwhile, of the 23 analysts covering NCLH, 11 rate it a Buy (3.96 out of 5), with a $24.19 target price.

While the upside is appealing, I would buy RCL if you’re seeking exposure in this area of the travel market.

ADT (ADT)

ADT (ADT) lost 6.49% on Monday on volume of 54.5 million, 5.5 times its 30-day average. Its shares are down 12.5% in 2026.

I didn’t even know ADT still existed. Just kidding, I see the security company’s ads all the time on legacy TV.

ADT reported its Q1 2026 earnings on April 30 before the markets opened. They were solid, beating analyst expectations, pushing ADT stock up 5% on the day.

However, that all got taken back and a bit more yesterday, after it announced plans for a secondary offering of 102 million shares. These shares represent the remaining stake in Apollo Global Management (APO), the alternative asset manager that acquired ADT for $7 billion in 2016 and took it public in 2018.

To mitigate the flood of shares into the market, ADT is repurchasing about 30% of Apollo’s stake as part of its $1.5 billion share repurchase plan.

Based on an enterprise value of $13.14 billion and free cash flow of $1.50 billion as of March 31, it has a FCF yield of 11.4%. I consider anything above 8% to be in value territory.

With its shares trading about half the $14 IPO price, value investors ought to consider it.

GameStop (GME)

GameStop lost 10.14% on Monday, on volume of 40.2 million shares, 4.2 times its 30-day average. Its shares are up 18.7% in 2026.

Ryan Cohen did as he promised investors he would yesterday by taking a massive swing at eBay. The $56 billion offer is 50% cash and 50% GME stock. If the company uses all $9 billion of its cash for the cash component, it then needs $19 billion in debt and equity funding. That’s a big chunk for a company whose current enterprise value is a tad over $6 billion.

Investors clearly had problems with the announcement and strategy.

GameStop’s big attraction today is the $9 billion in cash and marketable securities on its balance sheet. Subtract out the $4.2 billion in long-term debt, and it has nearly $5 billion in cash to invest in any deal to acquire another company.

That doesn’t include the positive cash flow the existing business is generating; it has had five consecutive quarters of operating income thanks to Cohen's cost-cutting at GameStop over the last couple of years.

So, when he says he can cut $2 billion in annual costs from eBay’s business within 12 months of closing a transaction, he has a recent track record of delivering on cost cuts.

The problem, as GME’s share price suggests, is that there is too much debt to pile on the combined entity to make it feasible.

While I like the idea of monetizing eBay’s business through its existing retail network, I personally don’t see this acquisition making it across the finish line.

I’d wait to see how everything shakes out before committing to Cohen’s hopes and dreams. As my mom used to say, “If it was meant to be, it will be.” No need to rush this.

United Parcel Service (UPS)

United Parcel Service (UPS) lost 10.47% on Monday, on volume of 18.5 million shares, 3.1 times its 30-day average. Its shares are down 2.9% in 2026.

Personally, I think it’s those god-awful brown uniforms that have done UPS in. Hardly anybody looks good in brown. But I digress.

Amazon (AMZN) is coming for UPS through its new Amazon Supply Chain Services logistics business. Yesterday, the $3 trillion behemoth announced the new service. It enables outside parties to utilize its massive transportation and logistics network, which includes a fleet of more than 80,000 trailers, 24,000 intermodal containers and over 100 aircraft operated in conjunction with its aviation partners. With customers such as Procter & Gamble (PG) on board, it’s sure to make a stir.

While this is a new and powerful competitor for UPS, it’s not as if Amazon's desire to leverage its logistics infrastructure to keep the supply chain fully primed hadn't been known for some time.

It’s the reason its stock is at or near a five-year low. UPS went public in November 1999 at $50 a share. If you bought shares in the IPO and hold them today, if not for dividends, you’ve not even doubled your money over 26 years.

As much as I don’t love Amazon as a company, if it’s a choice between it and UPS, you have to go with the former.

AGNC Investment (AGNC)

AGNC Investment (AGNC) lost 2.65% on Monday, on volume of 18.2 million shares, 1.2 times its 30-day average. Its shares are down 0.7% in 2026.

Of the five companies, AGNC is one I’m least familiar with. The real estate investment trust invests in Agency residential MBS (mortgage-backed securities). These are pools of residential MBS issued by government agencies such as Freddie Mac and Fannie Mae.

Investing in AGNC stock is primarily for income-focused investors. It went public as American Capital Agency Corp. in May 2008 at $20 a share. It yields a whopping 13.4% at current prices.

In Q1 2026, its economic return -- defined as the quarterly dividend per share plus the increase/decrease in tangible book value per share divided by tangible book value per share at the beginning of the quarter or period -- was -1.6%. Since the beginning of 2024, it’s been negative in four of nine quarters.

It’s not the be-all and end-all stat for AGNC, but it does indicate whether it’s operating in healthy mortgage market conditions. For example, AGNC’s economic return in 2025 was 22.7%, resulting in net income of $1.67 billion. As a result of the positive economic return, the stock’s total return was 34.8%.

AGNC uses significant leverage to amplify its returns. If you’re a risk-averse investor, even though it invests in MBS backed by government agencies, you are better off steering clear of this stock.

If you’re more aggressive, recent history (since 2020) suggests buying below $10 is likely to produce good long-term total returns.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

PayPal Shares Are Sliding Despite Earnings Beat. Here's Why. A $6 Billion Reason to Buy SanDisk Stock Here Cathie Wood Remains Convinced on CoreWeave After 78% YTD Rally in CRWV Stock Ahead of AMD Earnings, Here Is What Barchart Options Data Shows for AMD Stock