Investors are bailing on PayPal (PYPL) shares on May 5, even though the fintech posted better-than-expected financials for its first quarter.

The post-earnings selloff saw PYPL slip below its major moving averages (20-day, 50-day, 100-day) — a technical breakdown that signals bears have taken control across multiple timeframes.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Including today’s decline, PayPal stock is down about 23% versus its year-to-date high.

www.barchart.com

www.barchart.comWhat’s Weighing on PayPal Stock Today?

PYPL shares are under pressure primarily because of the company’s disappointing Q2 outlook.

While the digital payments specialist’s $8.35 billion in first-quarter revenue on $1.34 per share of earnings beat Street estimates, CEO Enrique Lores guided for a high-single-digit decline in adjusted earnings in the current quarter.

This came in significantly worse than a modest hit Wall Street analysts had anticipated.

Moreover, PayPal’s transaction margin dollars grew only 3% in Q1, failing to silence long-standing concerns regarding competitive pressure from Apple's (AAPL) Apple Pay and weakness in the firm’s core branded-checkout volume.

Note that PYPL’s relative strength index (RSI) sits in the late 30s currently, indicating further room for downside ahead.

Should You Buy the Dip in PYPL Shares?

Despite the headline noise, PayPal shares remain worth buying on the post-earnings dip for long-term value seekers.

The financial technology behemoth is now trading at about 9x earnings — a forward multiple that represents a meaningful discount not just to peers but to its own historical averages as well.

This means that the market has already priced in the worst-case scenario.

Additionally, as part of its commitment to accelerate AI adoption under Lores, PYPL has launched a $1.5 billion cost-cutting program aimed at improving product capabilities and operational efficiency.

All in all, with Venmo volume up 14%, an aggressive stock repurchase plan in place, and a 1.22% dividend yield, PayPal’s robust free cash flow and scale offer a sturdy floor for patient investors.

PayPal May Be Undervalued at Current Levels

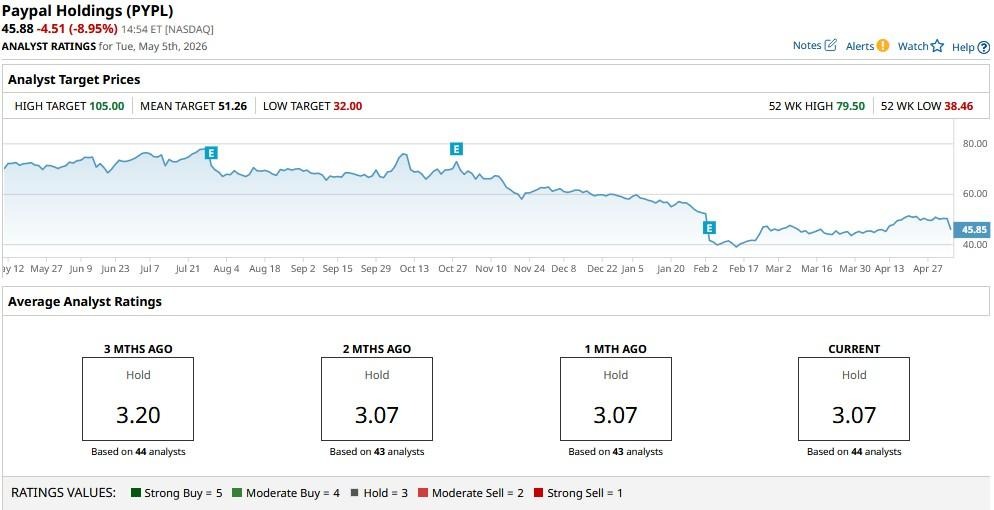

Wall Street analysts also seem to believe the sell-off in PYPL stock has gone a bit too far in 2026.

While the consensus rating on PayPal remains at “Hold,” the mean price target of about $51 signals potential upside of nearly 12% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

PayPal Shares Are Sliding Despite Earnings Beat. Here's Why. A $6 Billion Reason to Buy SanDisk Stock Here Cathie Wood Remains Convinced on CoreWeave After 78% YTD Rally in CRWV Stock Ahead of AMD Earnings, Here Is What Barchart Options Data Shows for AMD Stock