Sandisk Corporation (SNDK) is a memory player built for the data-hungry world, designing NAND flash storage that powers everything from consumer devices to hyperscale data centers. But in 2026, it is not just supplying storage. Rather, it is embedded within the artificial intelligence (AI) boom itself. As data-heavy AI workloads scale rapidly, demand for faster, efficient storage is surging, placing the company firmly at the core of this shift.

That positioning has translated into blistering growth. From cloud infrastructure to edge computing, its high-performance storage is seeing strong adoption. The data center segment is leading the charge as AI and cloud spending ramps up, while a richer enterprise customer mix and better pricing continue to strengthen revenue and overall business momentum. Plus, a shift toward long-term supply agreements – Sandisk’s so-called new business models – is bringing more predictability to revenues and margins, quietly strengthening the foundation beneath the growth story.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The stock, however, has not been a straight line up. There was a wobble in March, when uncertainty around future memory demand surfaced after new developments like Alphabet's (GOOGL) Google TurboQuant. But that dip didn’t last long. Since then, Sandisk has staged a stunning comeback, and now SNDK stock is in the spotlight as one of the best-performing names in the S&P 500 Index ($SPX) this year, with gains that have turned heads across the market.

The real spark came after Sandisk’s third-quarter results last week, where the data center business revenue more than tripled. That clearly showed how fast AI demand is reshaping its growth. Now, with that momentum still going strong, this is no longer just a rally story. It is shaping up into a steady, long-term growth play driven by AI demand.

About Sandisk Stock

Headquartered in Milpitas, California, Sandisk is a leading global provider of NAND flash memory solutions. The company designs and manufactures SSDs, memory cards, and embedded storage used in consumer electronics, enterprise systems, and data centers. With a market capitalization of $207.6 billion, Sandisk plays a key role in modern digital infrastructure. It benefits from strong demand driven by AI, cloud computing, and big data, where hyperscalers increasingly rely on high-performance, scalable storage to support growing data workloads and advanced computing needs.

SNDK stock has been one of the most closely watched market stories since its separation from Western Digital (WDC) last year. The move gave Sandisk a sharper focus and a clearer path to value creation. Tighter NAND supply and rising prices have supported earnings visibility. Plus, its vertically integrated model, from wafer fabrication to SSD assembly, enhances efficiency and innovation. With higher R&D and advances in TLC and QLC NAND, Sandisk is well-positioned for the next phase of enterprise storage growth, driven by AI and cloud demand.

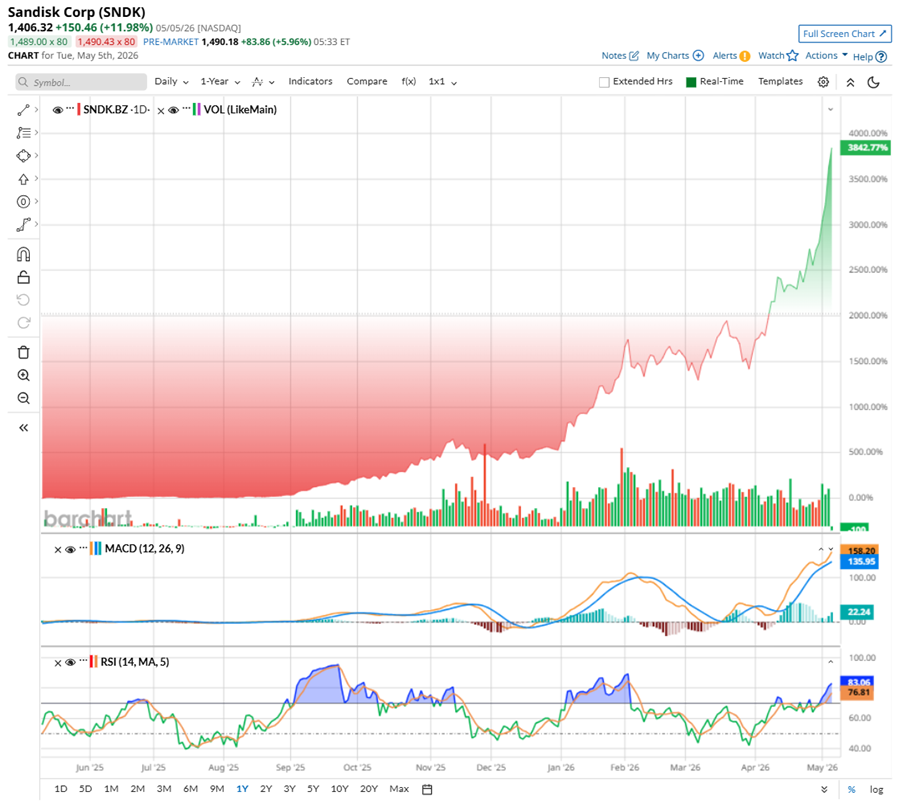

Shares of the memory chip maker have delivered a dramatic performance over the past 52 weeks, up 4,043%. In fact, in 2026, SNDK stock has surged 490.5%, making it one of the standout momentum names in the broader market.

However, the path has not been smooth. At one point, the stock faced pressure after the expiry of a lock-up period that released over two million insider and Western Digital’s shares, raising concerns of potential selling. Broader macro headwinds, including geopolitical tensions and rising energy costs, also triggered phases of profit booking. In addition, a controversial $1 billion investment in Nanya Technology raised questions around capital allocation, while Google’s TurboQuant announcement briefly sparked worries about future memory demand.

Despite these interruptions, investor sentiment remained largely confident. SNDK stock has been printing new highs recently after its Q3 update on April 30, and from there, it just kept climbing. Investors stayed glued to the story, betting that the massive buildout of AI data centers would keep memory demand running hot. Plus, as analysts turned more upbeat on the flash memory supplier, confidence started trickling in more broadly, almost feeding the momentum further.

Technically, Sandisk’s trading volumes are picking up with stronger green bars, showing steady buying interest. The 14-day RSI of 80.61 has climbed into overbought territory, hinting the stock has been moving very strongly. Even so, momentum has not faded yet. The MACD oscillator remains supportive, with the MACD line holding above the signal line and continuing to trend higher, while the positive histogram suggests bulls are still firmly in control of the move.

www.barchart.com

www.barchart.com After such a sharp rally, it would be easy to assume Sandisk is stretched on valuation, but that picture is not really extreme. SNDK stock is currently priced at 21.79 times forward adjusted earnings, which sits below the sector average.

Sandisk’s Rally After an Impressive Q3 Report

Sandisk’s Q3 2026 report was impressive, demonstrating how sharply its business model is scaling in the AI era. Revenue skyrocketed 251% year-over-year (YOY) to $5.95 billion, powered by strong momentum across its core segments. Management attributed this acceleration to a clear shift in customer mix toward higher-value enterprise and cloud buyers, alongside a firmer pricing environment that better reflects the value of its technology.

The data center business emerged as a standout, jumping 645% YOY to $1.46 billion, while the edge segment climbed 295% YOY to $3.66 billion.

A key driver behind the quarter’s growth was strong demand for TLC-based enterprise SSDs, which are widely used in latency-sensitive, performance-heavy computing workloads. Sandisk also noted rising storage needs in premium PCs and smartphones, as on-device AI capabilities continue to expand memory requirements.

The profitability leap was even more striking. Non-GAAP gross margins expanded dramatically to 78.4%, compared to 22.7% a year earlier. Non-GAAP EPS swung sharply into positive territory at $23.41, versus a loss of -$0.30 per share in Q3 2025, highlighting a strong bottom-line turnaround.

Meanwhile, the company’s operating cash flow rose to $3.04 billion from just $26 million a year ago, while adjusted free cash flow reached $2.955 billion, translating into a 49.7% margin. Sandisk ended the quarter with $3.74 billion in cash and no short-term debt, reinforcing balance sheet strength. Additionally, it announced a $6 billion share repurchase program.

Strategically, the company is leaning deeper into long-term agreements. More than one-third of fiscal 2027 bit supply is now contracted under five deals, backed by over $11 billion in enforceable guarantees. Additionally, three new contracts signed during the quarter contribute to a minimum $42 billion revenue backlog, signaling strong long-term visibility.

Looking ahead to Q4, Sandisk is stepping into the next phase with even stronger expectations. The management guided revenue between $7.75 billion and $8.25 billion, alongside non-GAAP EPS in the range of $30 to $33, signaling continued earnings momentum. Margins are also expected to stay elevated, with non-GAAP gross margin projected to be between 79% and 81%, while operating expenses are guided between $480 million and $500 million, reflecting ongoing investment in innovation alongside profitability strength.

A key milestone in the quarter will be the start of revenue shipments from its QLC Stargate solutions. Management sees the data center opportunity expanding further as AI infrastructure buildouts accelerate. Rising demand for low-latency flash storage, especially as inference workloads scale and technologies like KV cache and retrieval-augmented generation gain traction, is expected to keep memory requirements structurally high, reinforcing Sandisk’s positioning at the core of AI-driven storage growth.

Meanwhile, analysts monitoring the company are upbeat, anticipating $8.15 billion in revenue, with EPS of roughly $25.32 in Q4. Fiscal 2026 EPS is anticipated to be $50.53, a significant 2,738.8% YOY jump, followed by a further 164.9% annual rise to $133.84 in fiscal 2027.

What Do Analysts Expect for Sandisk Stock?

After Sandisk’s Q3 report, analysts basically came out even more bullish, and the tone on the Street has clearly shifted higher. Susquehanna doubled its price target on SNDK from $1,000 to $2,000 and kept a “Positive” rating. What stood out for them was not just the earnings beat, but the visibility.

They pointed out that nearly a third of fiscal 2027 revenue is already contracted, which gives a rare sense of predictability in a typically cyclical memory business. Plus, a similar contract momentum is anticipated to continue into fiscal 2028 and beyond. On top of that, Sandisk’s plan to allocate 50% of FCF toward buybacks over the next two years is expected to add around 10% earnings accretion, which Susquehanna sees as a strong tailwind for shareholder returns.

Bernstein also turned optimistic after the results, believing stock prices could go up as much as $1,700 and maintaining an “Outperform” rating. The brokerage firm described the quarter as a strong beat with robust guidance, driven largely by firm NAND pricing and healthy demand trends. According to Bernstein, pricing strength is the key driver behind its upward revision to earnings estimates, with continued near-term momentum feeding into higher forecasts.

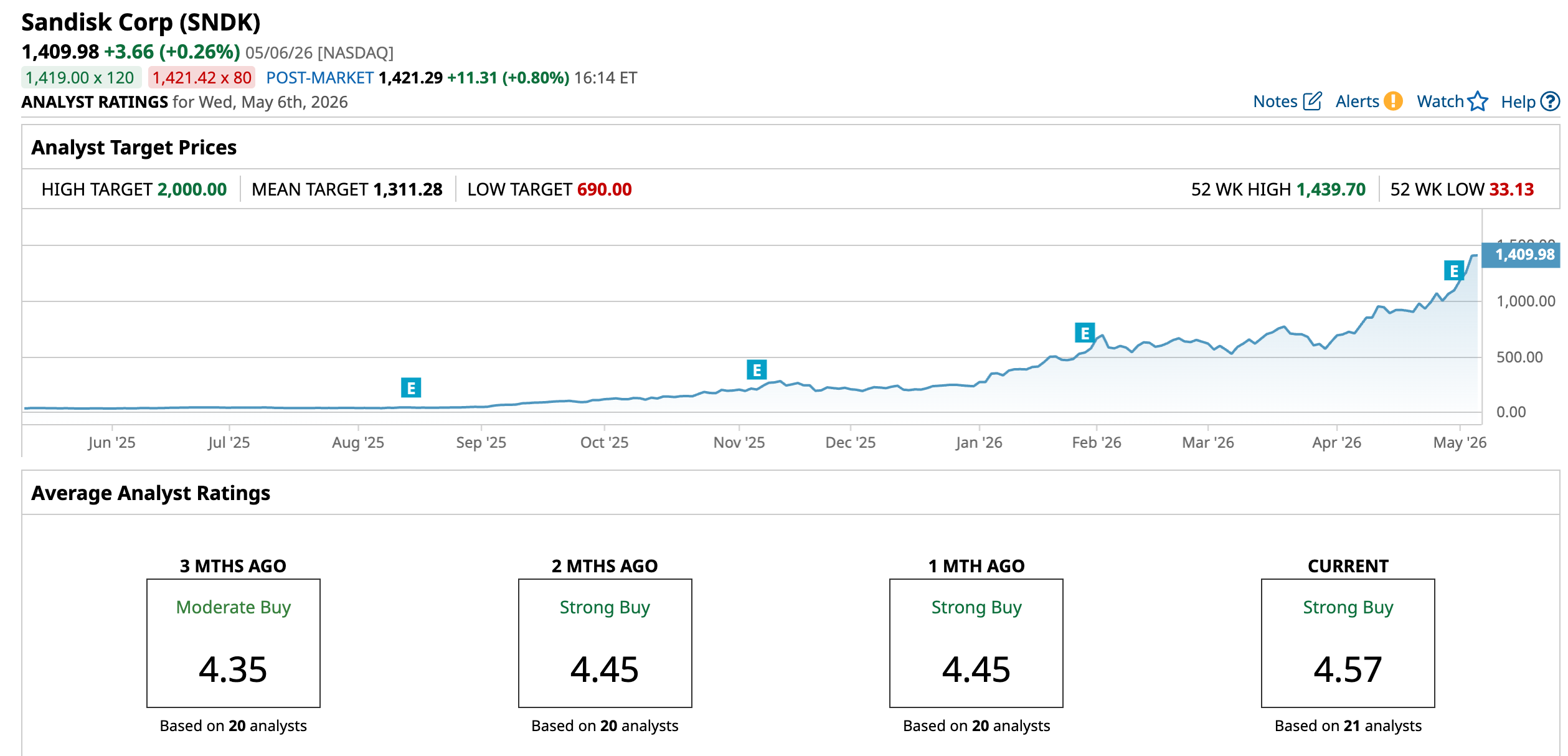

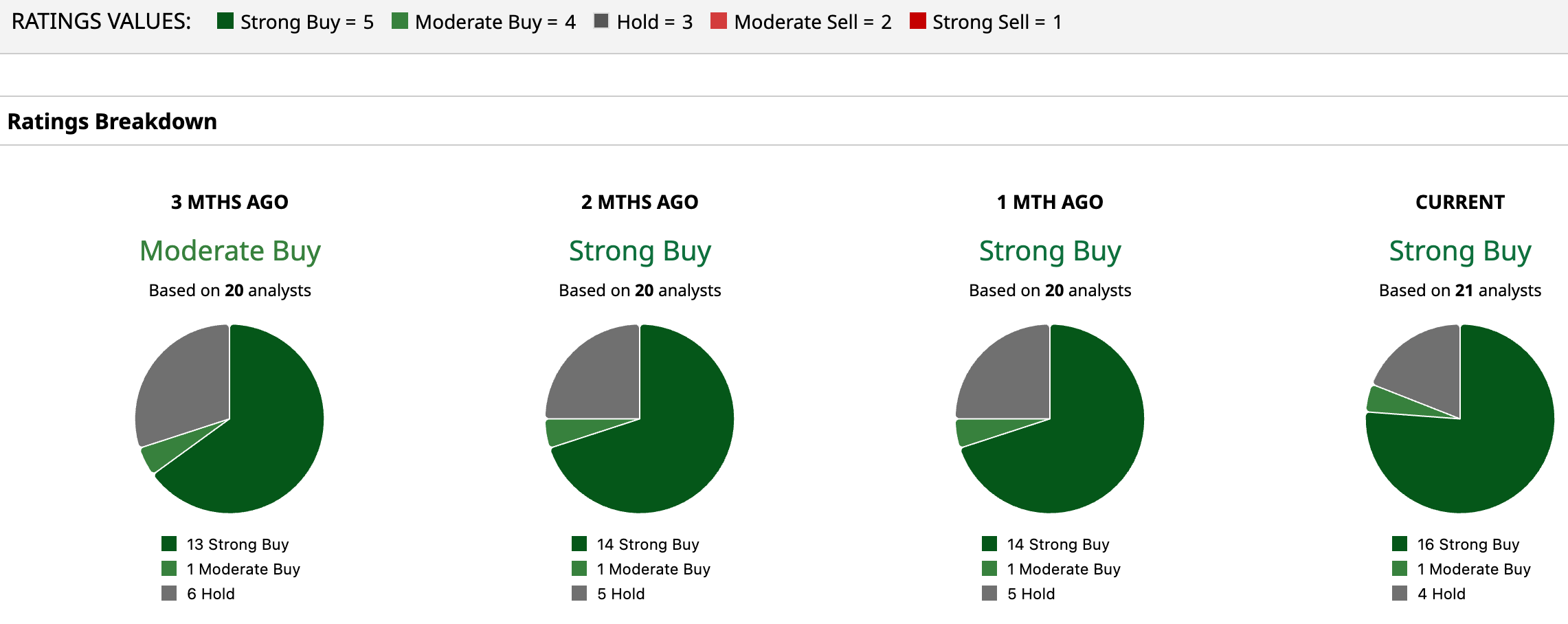

Overall, SNDK has a consensus “Strong Buy” rating now, and that’s an upgrade from the “Moderate Buy” rating three months ago. Of the 21 analysts covering the stock, 16 advise a “Strong Buy,” one suggests a “Moderate Buy,” and the remaining four analysts are on the sidelines, giving it a “Hold” rating.

Plus, after SNDK’s rally over the past couple of weeks, the stock has surged past the average analyst price target of $1,311.28. Yet, the Street-high target price of $2,000 suggests that the stock could rally as much as 41.9%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Final Thoughts on SNDK Stock

If I look back at when I last covered SNDK stock in March, I was reacting to the noise around Google’s TurboQuant update. At that time, SNDK was hovering near $603. Since then, it has more than doubled from those levels, and honestly, is now one of the sharper moves in the semiconductor space this year.

What stood out then, and still stands out now, is that AI demand was clearly building, earnings were improving, and the bigger picture was shifting toward stronger storage intensity. That view has basically played out with more force than expected.

The Q3 numbers, especially growth in the data center business, along with upbeat guidance from management and analysts, drove sentiments and price performance.

Still, we know how semiconductors work. These are cyclical businesses at their core. When pricing is strong, supply eventually responds. That’s how the cycle resets. The difference right now is that the AI-driven demand shock is strong enough to potentially stretch this up-cycle further than usual.

For now, SNDK feels less like a traditional chip cycle trade and more like a momentum-plus-AI demand story still with upside, although some strong trends never move straight and usually pause before the next leg higher.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing. The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze 7 Stocks Worth Buying the Dip in Now... Or At Least Adding to Your Watchlist