CoreWeave (CRWV) will release its first-quarter financial results on Thursday, May 7. CRWV stock has witnessed a sharp rally this year, rising by more than 70% in the past month alone. The significant jump ahead of CoreWeave's earnings release is being driven by growing confidence that the company is well-positioned to capitalize on accelerating demand for artificial intelligence (AI) infrastructure — and on recent large-scale, long-term commercial agreements with Meta Platforms (META) and Anthropic.

CoreWeave recently expanded its partnership with Meta, committing to provide AI cloud capacity through the end of 2032. Valued at roughly $21 billion, the deal significantly deepens its partnership with the tech giant and provides long-duration revenue visibility.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In parallel, the firm has secured a multi-year agreement with Anthropic, a leading developer of advanced AI models. This partnership will support the training and deployment of Anthropic’s Claude model family, with compute capacity expected to come online later this year.

These deals are likely to materially expand CoreWeave’s contracted backlog, adding visibility to future revenue growth. Moreover, the operating environment remains highly favorable for CoreWeave. The rapid expansion of AI compute is driving significant demand for CoreWeave’s high-performance computing infrastructure. This suggests that the company will likely deliver significant revenue growth in Q1, supporting the ongoing stock rally. However, margins could be a concern. Here's what investors should know.

www.barchart.com

www.barchart.com AI Infrastructure Demand to Boost CoreWeave’s Q1 Performance

CoreWeave’s Q1 will reflect solid top-line growth as demand for its high-performance computing infrastructure remains solid. Moreover, CoreWeave’s top-line growth will likely be driven by its diversified customer base, which positions it to capture growth across multiple layers of the expanding AI ecosystem.

CoreWeave generated more than $5.1 billion in revenue in 2025, up 168% year-over-year (YOY). Its contracted revenue backlog also reached $66.8 billion, offering substantial visibility into future demand and reducing uncertainty around growth.

The momentum is likely to sustain in Q1 and beyond. Management expects Q1 revenue between $1.9 billion and $2 billion. This implies both strong sequential growth and YOY expansion likely to exceed 100%, reflecting sustained demand for its infrastructure.

CoreWeave’s customer engagement trends further strengthen the outlook. The number of clients spending at least $1 million annually on CoreWeave Cloud rose almost 150% in 2025, indicating deeper adoption among high-value users. At the same time, CoreWeave is broadening its platform, evolving beyond GPU infrastructure into a more integrated offering that includes storage, software, and developer tools. The strategy is working, with increased cross-selling momentum and rising adoption of storage products, helping to boost customer lifetime value.

With much of its new capacity already committed, the company is scaling infrastructure to meet demand. However, this aggressive expansion comes at a cost. Profitability is expected to remain under pressure in the near term, with margins starting in the low single digits in Q1 before gradually improving through the year, potentially reaching low double digits by Q4 as scale efficiencies begin to materialize.

Is CoreWeave Stock a Buy, Sell, or Hold?

CoreWeave is expected to benefit from surging demand for its AI compute infrastructure, with a growing backlog of orders and expanding partnerships strengthening its investment case.

Thanks to the strong demand and solid growth, management expects an annualized revenue run rate of $17 billion to $19 billion by the end of 2026. Moreover, the company plans to surpass $30 billion as it exits 2027. These projections are likely to be supported by long-term customer agreements, strategic partnerships, and ongoing expansion of its infrastructure footprint.

Overall, CoreWeave is a solid long-term investment. However, near-term margin pressures remain a concern, and shares have already seen a notable jump. CRWV stock has also dropped after reporting earnings in the past three quarters, which warrants caution.

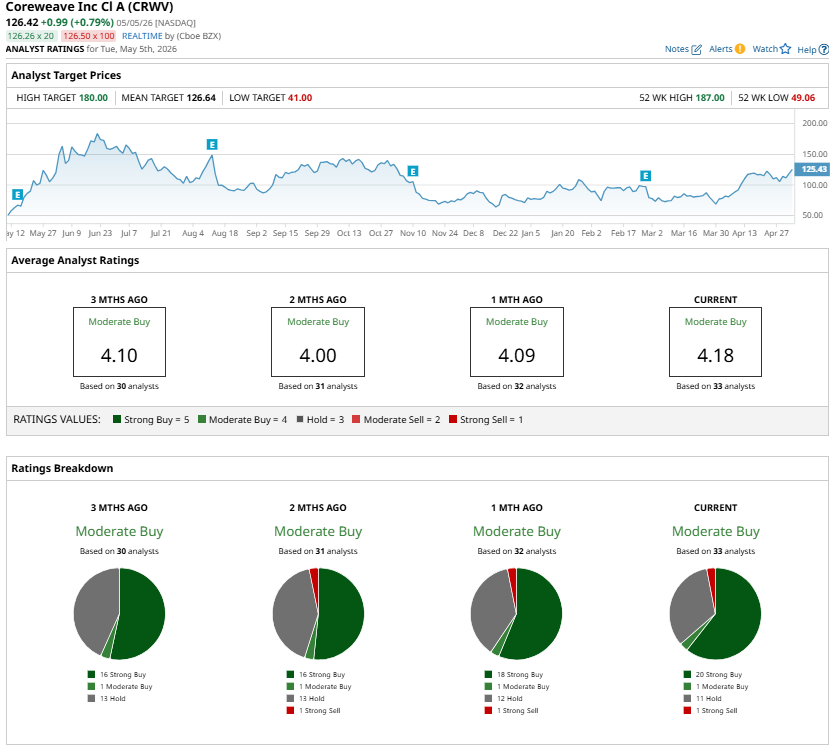

While analysts currently maintain a “Moderate Buy” consensus rating ahead of the upcoming earnings report, investors should wait for a dip before considering an entry.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing. The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze 7 Stocks Worth Buying the Dip in Now... Or At Least Adding to Your Watchlist