Service Corporation International SCI, the largest provider of deathcare products and services in North America, continues to reinforce its commitment to consistent shareholder returns through disciplined capital allocation and stable cash flow generation.

Service Corp announced a quarterly cash dividend increase to 36 cents per share from the previously declared 34 cents, marking a 6% hike. The dividend will be payable on June 30, 2026, to its shareholders of record at the close of business on June 15. The latest dividend increase reflects management’s confidence in the company’s resilient business model and long-term financial strength.

SCI has consistently prioritized returning capital to its shareholders through regular dividend increases, supported by dependable demand trends in funeral, cemetery and cremation services. The company’s broad geographic footprint and diversified service offerings continue to provide stable recurring revenues and strong cash-generation capabilities.

In first-quarter 2026, Service Corp returned $190 million in capital to its shareholders, comprising $143 million in share repurchases and $47 million in dividend payments. The company bought back nearly 2 million shares during the quarter at an average price of roughly $80 per share, bringing its outstanding share count to a little more than 130 million as of the end of March.

Management noted that while it intends to continue paying regular quarterly dividends, future declarations will remain subject to board approval following a review of financial performance and liquidity conditions. The company also highlighted potential risks, including financing restrictions, tax law changes and shifts in cash requirements, which could affect future dividend decisions.

What More Should Investors Know About SCI?

Headquartered in Houston, TX, SCI currently operates 1,487 funeral service locations and 503 cemeteries across North America under several recognized brands, including Dignity Memorial. Serving nearly 700,000 families annually, the company remains well positioned to drive long-term growth while maintaining a strong shareholder-friendly capital return strategy.

Service Corp continues to benefit from strong momentum in its preneed cemetery business, supported by healthy sales execution and expanding community outreach initiatives. In first-quarter 2026, preneed cemetery sales production increased 10% year over year, driven by robust large sales activity and improving sales velocity. Management highlighted growing success from seminar-based marketing efforts, expansion of community sales teams and improved lead generation strategies, which are helping SCI reach customers beyond traditional funeral-home channels.

The company is also strengthening its long-term growth platform through strategic investments and acquisitions. During the quarter, SCI invested $108 million across maintenance projects, cemetery development, digital initiatives and new funeral-home construction. Additionally, the company spent $24 million on acquisitions across multiple states, while management indicated continued optimism regarding its acquisition pipeline for 2026.

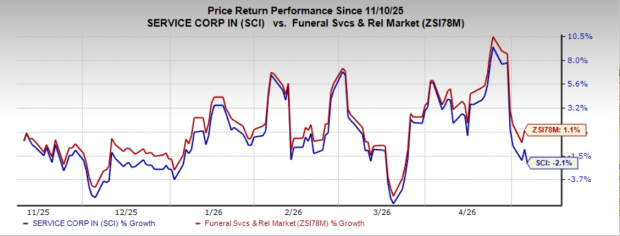

In the past six months, this Zacks Rank #4 (Sell) company has lost 2.1% against the industry’s 1.1% growth.

SCI Stock's Price Performance

Image Source: Zacks Investment Research

Stocks to Consider

Smithfield Foods, Inc. SFD produces various packaged meats and fresh pork products in the United States and internationally. It carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Smithfield Foods’ current financial-year sales and earnings indicates growth of 1.3% and 7.5%, respectively, from the prior-year reported levels. SFD delivered a trailing four-quarter earnings surprise of 12%, on average.

Tyson Foods, Inc. TSN operates as a food company through the Beef, Pork, Chicken and Prepared Foods segments. TSN currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Tyson Foods’ current fiscal-year sales calls for growth of 3.7%, while the same for earnings indicates a decline of 0.2% from the year-ago figures. TSN delivered a trailing four-quarter earnings surprise of 18.1%, on average.

Post Holdings POST operates as a consumer-packaged goods holding company. At present, POST carries a Zacks Rank of 2.

The consensus estimate for Post Holdings’ current fiscal-year sales and earnings implies growth of 2.7% and 0.1%, respectively, from the year-ago figures. POST delivered a trailing four-quarter earnings surprise of 19.6%, on average.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tyson Foods, Inc. (TSN): Free Stock Analysis Report

Smithfield Foods, Inc. (SFD): Free Stock Analysis Report

Service Corporation International (SCI): Free Stock Analysis Report

Post Holdings, Inc. (POST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).