On May 6, Uber Technologies UBER announced its first-quarter 2026 results, reporting better-than-expected earnings per share. Moreover, management gave a bullish outlook for bookings, noting that demand remains strong despite geopolitical tensions in the Middle East.

Before analyzing the factors driving this positive outlook, let’s first review the first-quarter results.

UBER’s Q1 Earnings Snapshot

Uber’s earnings per share of 72 cents beat the Zacks Consensus Estimate of 70 cents. The reported figure matched the higher end of the company's guided range of 65-72 cents per share.

Total revenues of $13.2 billion missed the Zacks Consensus Estimate of $13.3 billion. The top line jumped 14.4% year over year on a reported basis and 10% on a constant currency basis.

Despite the crisis in the Middle East, UBER’s Mobility business saw impressive demand, with segmental revenues increasing 5% year over year on a reported basis and 1% on a constant currency basis to $8.2 billion.

Gross bookings from the unit were highly impressive, aiding the first-quarter results. Gross bookings from the Mobility segment in the March quarter increased 20% year over year on a constant-currency basis to $26.4 billion.

Uber’s Delivery business also performed well in the quarter, with segmental revenues growing 23% year over year on a constant-currency basis. Gross bookings from the Delivery segment in the first quarter rose 23% year over year on a constant-currency basis to $26 billion. Total gross bookings jumped 25% to $53.7 billion, ahead of the Zacks Consensus Estimate of $52.9 billion.

Uber saw a 17% increase in its monthly active platform consumers to 199 million in the March quarter. The platform recorded 3.64 billion trips, marking a 20% year-over-year rise, driven by both ride-hailing and delivery services.

Why Uber Stock Gained Post Q1 Release

Uber shares have been on the rise since the release of the March quarter results, gaining 5.2%. Even though revenues missed expectations, the top line increased 14.4% year over year on a reported basis and 10% on a constant currency basis.

More than the first-quarter numbers, it was the second-quarter gross bookings forecast that pleased investors. Despite the ongoing tensions in the Middle East and the resultant fuel price spike, gross bookings are projected in the range of $56.25 billion-$57.75 billion, highlighting growth of 18% to 22% year over year on a constant-currency basis. The outlook assumes a roughly 2 percentage-point currency tailwind to total reported year-over-year growth.

Adding to the bullishness, management expects June quarter earnings to grow in the 31-38% band year over year. As a result, second-quarter earnings per share are expected in the 78-82 cents band. The Zacks Consensus Estimate is currently pegged at 79 cents per share.

UBER’s Overall Price Performance Is Unimpressive

Despite the first-quarter earnings beat, shares of UBER have declined in double digits (% wise) over the past six months. UBER’s shares have also underperformed the Zacks Internet-Services industry over the same time frame. Rival Lyft’s LYFT shares have performed even worse.

6-Month Price Comparison

Uber’s shares have dropped primarily on concerns regarding competition in the robotaxi and autonomous driving space.

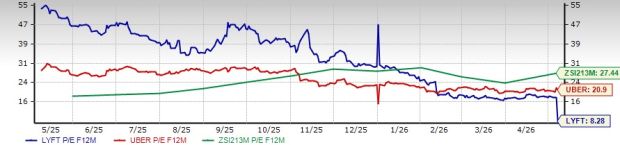

Valuation Picture

From a valuation perspective, Uber’s shares are cheaper compared with its industry. The company has a Value Score of C. Shares of Lyft are cheaper and the company has a Value Score of B.

UBER’s P/E F12M Vs. Industry & LYFT

How to Play Uber Post-Q1 Earnings

Despite Uber’s weak stock performance, elevated debt burden and persistent macroeconomic pressures creating short-term headwinds, the long-term outlook for the ride-hailing leader remains encouraging.

The company’s emphasis on strategic diversification and shareholder-oriented initiatives continues to serve as a major strength. Backed by a robust market capitalization of $161.74 billion, Uber remains well-positioned to navigate the current economic uncertainty. Its diversification strategy — spanning acquisitions, international expansion and innovative service offerings — has played a vital role in reducing risks and reinforcing its competitive standing.

Earlier this month, Uber Eats, its online food ordering and delivery arm, broadened its collaboration with Ahold Delhaize USA, a leading grocery retailer, to improve on-demand grocery delivery services for customers across the Northeast and Mid-Atlantic regions. Last year, Uber partnered with retailer Best Buy BBY to offer on-demand delivery services. Through this agreement, consumer electronics from more than 800 Best Buy stores became available on the Uber Eats platform. As a result, customers throughout the United States can order a broad selection of electronics, appliances and technology essentials via Uber Eats and have them delivered directly to their homes. The partnership further enhances customer convenience by making cutting-edge technology products more accessible.

Within the rapidly expanding autonomous vehicle (AV) market, Uber is adopting a partnership-focused strategy to capitalize on emerging opportunities. By working alongside multiple technology leaders, the company has been able to avoid the substantial research and development costs associated with building in-house AV capabilities, while still progressing toward its automation ambitions.

Overall, Uber’s large-scale operations, strategic investments and diversification efforts create a strong platform for long-term growth. Maintaining positions in this Zacks Rank #3 (Hold) stock, despite the recent decline, appears to be a sensible approach at present, while potential investors may prefer to wait for a more attractive entry opportunity.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Best Buy Co., Inc. (BBY): Free Stock Analysis Report

Lyft, Inc. (LYFT): Free Stock Analysis Report

Uber Technologies, Inc. (UBER): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).