Costco Wholesale Corporation (COST) essentially has geopolitical chaos doing its marketing for it right now, amid the U.S-Iran war. The bulk retail warehouse giant came out swinging on Wednesday, May 6, posting net sales of $23.92 billion for the retail month of April, the four weeks ended May 3, a 13% year-over-year (YOY) jump that had Wall Street doing a double take.

Shoppers loaded their carts with everything in sight as Strait of Hormuz tensions rattled oil markets and stirred freight cost fears, sending anxious consumers straight into the arms of bulk retail. The Easter holiday timing threw extra fuel on the fire, lifting total and comparable sales by roughly 1.5% to 2%.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Comparable sales burned 11.6% higher across the four weeks ended May 3, with U.S. stores clocking 11.7% while Canada and other international markets each punched in at 11.5%. E-commerce pulled its weight too, surging 18.8% as households stocked up digitally.

Stripping out foreign exchange noise and gasoline prices, comparable sales still grew a healthy 7.8%, including an 8% gain in the U.S. This shows that as long as the war keeps nerves on edge and inflation growing, shoppers would keep pushing oversized carts through those warehouse doors.

About Costco Stock

Founded in 1976 and now sitting on a market cap of approximately $441.77 billion, Costco has built a retail institution. The Issaquah, Washington-based behemoth runs 928 membership-based warehouse clubs spread across 14 countries, selling everything from bulk groceries and apparel to electronics and tires at prices that make competitors sweat.

The warehouses pull double duty by housing pharmacies, food courts, and gas stations right under the same roof, and the company rounds out its offerings with e-commerce and travel services.

On the price performance front, COST stock has had a bit of a mixed bag run. It slipped 1.05% over the last 52 weeks, yet it bounced back strongly on a year-to-date (YTD) basis, climbing 15.56% in 2026. The past month, however, threw cold water on the momentum as the stock pulled back another 1.64%.

www.barchart.com

www.barchart.com On the valuation front, COST stock is sitting at a premium. It currently trades at 50.03 times forward adjusted earnings and 1.48 times sales, both of which sail comfortably above the industry averages and the stock's own five-year average multiples.

On the income side, Costco has grown its dividend for 21 consecutive years. It pays an annual dividend of $5.88 per share, which translates to a yield of 0.58%.

On April 15, the company declared its quarterly cash dividend and bumped it up from $1.30 per share to $1.47 per share, working out to the aforementioned $5.88 per share price. Shareholders of record at the close of business on May 1 will receive the payment on May 15.

Costco Surpasses Q2 Earnings

On March 5, Costco dropped its Q2 fiscal year 2026 earnings and knocked it out of the park on both the top and bottom lines. Revenue climbed 9.2% YOY to $69.6 billion, clearing the analyst estimate of $69.06 billion. EPS landed at $4.58, up 13.9% from the prior year’s period and edging past the Street's forecast of $4.55.

Net sales increased 9.1% from the prior year’s quarter to $68.2 billion. Comparable sales grew 7.4%, or 6.7% adjusted for gas price deflation and FX. The digital side of the business stole the show, with digitally enabled comparable sales surging 22.6%, or 21.7% on an FX-adjusted basis.

Membership fee income hit $1.355 billion, a jump of $162 million or 13.6% YOY and 12.2% on an FX-adjusted basis. Costco closed Q2 with 40.4 million paid executive memberships, up 9.5% from the prior year. Total paid members reached 82.1 million, up 4.8% YOY, while total cardholders climbed to 147.2 million, a 4.7% increase.

Operating income rose 12.5% from the prior year’s quarter to $2.6 billion while net income rose 13.8% from the year-ago value to $2 billion. On the balance sheet, cash and cash equivalents stood at $17.4 billion as of Feb. 15, a healthy step up from $14.1 billion on Aug. 31, 2025.

Looking forward, the company expects full-year capital expenditures of approximately $6.5 billion, money it plans to put to work expanding its new warehouse pipeline, remodeling existing locations to squeeze more out of high-volume buildings, growing its depot network, and sharpening the member digital experience.

Looking ahead, analysts see Q3 fiscal year 2026 EPS at $4.88, a 14% YOY increase. Full-year fiscal 2026 EPS estimates sit at $20.32, pointing to 13% annual growth, and fiscal year 2027 estimates push that figure to $22.36, adding another 10% on top.

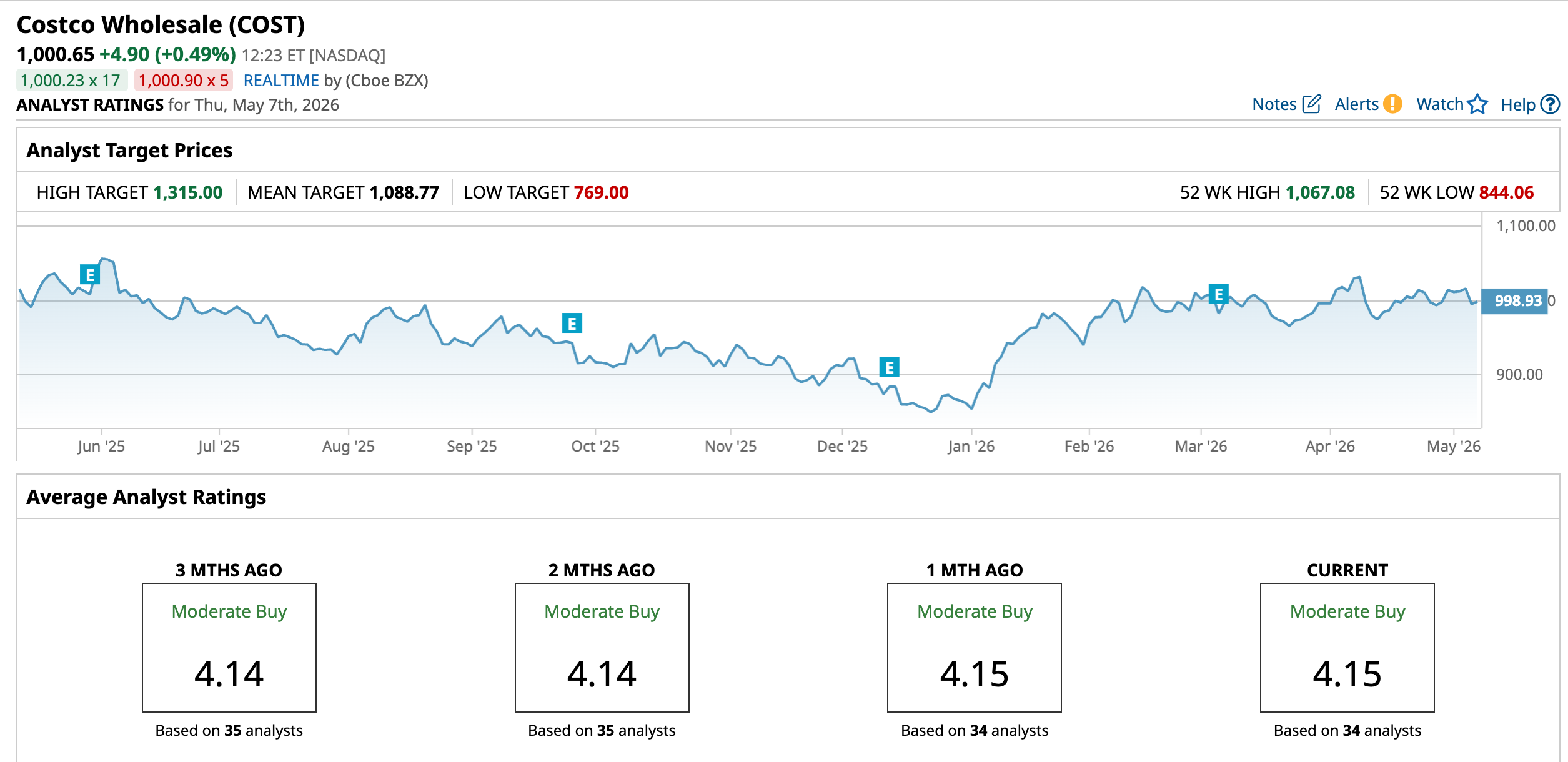

What Do Analysts Expect for Costco Stock?

Wall Street has largely made up its mind on Costco, and the verdict leans bullish. In fact, Telsey Advisory Group analyst Joseph Feldman keeps his "Outperform" rating on COST stock and has nudged the price target up from $1,125 to $1,135.

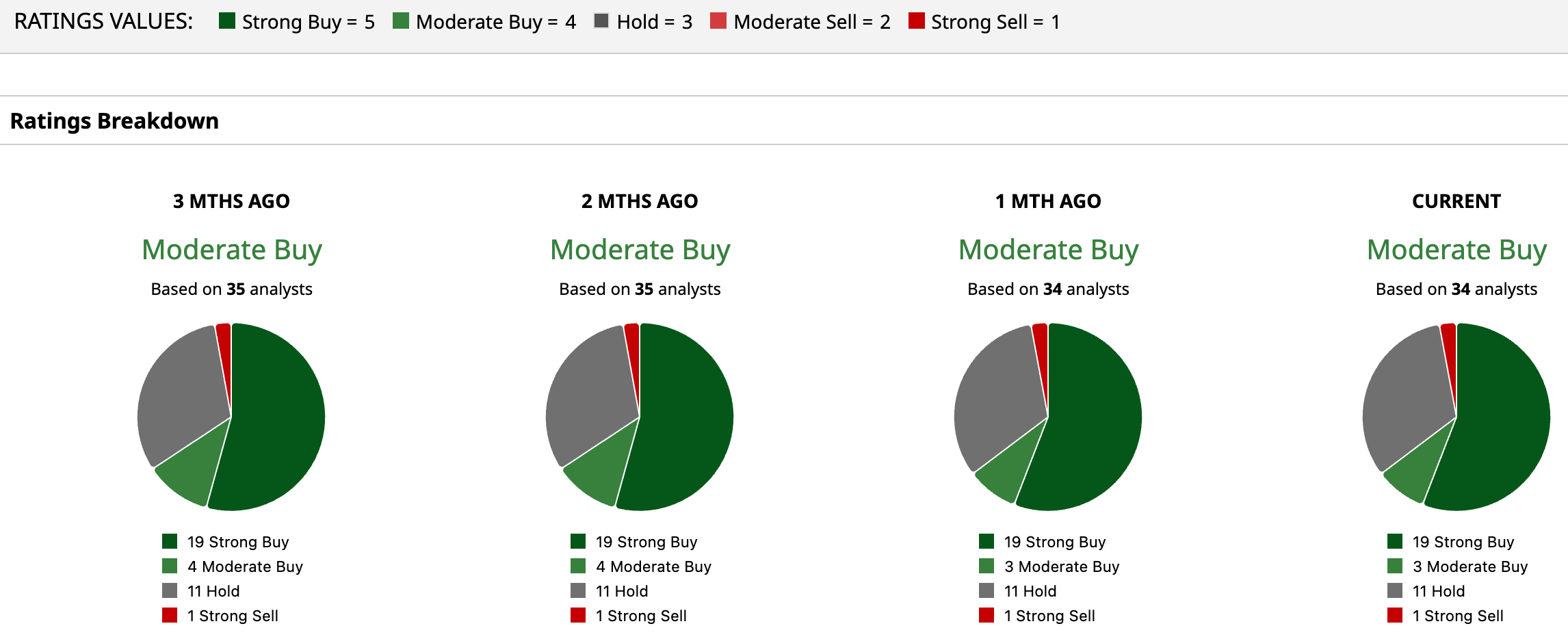

Wall Street has collectively given COST stock a "Moderate Buy" rating. Of the 34 analysts covering the stock, 19 stamp it a "Strong Buy," three hand it a "Moderate Buy," 11 sit on the fence with a "Hold," and one lone voice has thrown up a "Strong Sell."

The stock’s average price target of $1,088.77 represents potential upside of 8.8%. Meanwhile, the Street-High target of $1,315 suggests a gain of 31.42% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Costco Stock Is Benefiting from a Jump in April Sales. It Can Thank the Strait of Hormuz. JPMorgan vs. Bank of America: How the 2 Dividend-Paying Bank Stocks Stack Up in 2026 Western Digital Just Increased Its Dividend by 20% but It’s Still Not a Yield Play AbbVie Delivers Strong Q1 Earnings Beyond Humira. This Dividend King Still Shines.