GE Aerospace’s GE investors have been witnessing impressive gains from the stock of late. Shares of the leading designer and producer of jet engines have surged 35.7% in the past year, outpacing the industry and the S&P 500 composite’s growth of 7.5% and 31.9%, respectively. The company has also outperformed other industry players like RTX Corporation RTX and Textron Inc. TXT, which have returned 34.8% and 18.5%, respectively, over the said time frame.

GE Outperforms the Industry, S&P 500 & Peers

Image Source: Zacks Investment Research

Closing at $297.15 on Friday, the stock is trading below its 52-week high of $348.48 but significantly higher than its 52-week low of $211.15.

What’s Behind GE Stock’s Momentum?

GE Aerospace is benefiting from a growing installed base and higher utilization of engine platforms, driven by strong momentum across the commercial & defense sectors. Solid demand for LEAP, GEnx & GE9X engines and services has been proving beneficial for the Commercial Engines & Services business.

In first-quarter 2026, the company received orders for more than 650 commercial engines, including commitments from American Airlines, United Airlines and Delta Airlines. It also entered into a long-term materials agreement to support Ryanair’s fleet of about 2,000 CFM56 and LEAP engines. Also, in 2025, it inked a deal with Qatar Airways to supply more than 400 GE9X and GEnx engines. It represents the largest widebody engine deal in GE Aerospace’s history. The Commercial Engines & Services business’ revenues and orders jumped 34% and 93%, respectively, on a year-over-year basis in the first quarter.

Solid demand for GE’s propulsion & additive technologies, critical aircraft systems and aftermarket services in the defense sector is driving the Defense & Propulsion Technologies business’ performance. In first-quarter 2026, it clinched a $1.4 billion deal for T408 engines to support the U.S. Marine Corps’ CH-53K helicopter fleet. Also, in 2025, the company secured a $5 billion contract from the U.S. Air Force to supply F110 engines, parts and support services as part of a Foreign Military Sales (FMS) program. In the first quarter, the Defense & Propulsion Technologies business’ revenues increased 19% year over year and orders grew 67% in the year.

For 2026, GE Aerospace expects adjusted revenues to increase in the low-double-digit range, including mid-teens growth in the commercial engines and services unit and mid-to-high single-digit growth in the defense and propulsion technologies unit.

GE remains committed to rewarding shareholders with dividends and share repurchases. In first-quarter 2026, it bought back shares for $2.2 billion. In the same period, the company paid dividends of $381 million, up 26.2% year over year, to its shareholders.

Despite the positives, the rising debt level is concerning for the company. Exiting the first quarter, GE Aerospace’s total borrowings were $20.3 billion. The figure comprised of $2.1 billion of short-term borrowings and $18.2 billion of long-term borrowings.

GE has also been dealing with the adverse impacts of the high cost of sales and operating expenses. In the first quarter, its cost of sales surged 32% year over year to $7.9 billion, while selling, general and administrative expenses increased 23.7% to $1.08 billion. Research and development expenses also rose 22.6% to $440 million. In the quarter, GE’s operating profit margin contracted 200 basis points to 21.8%.

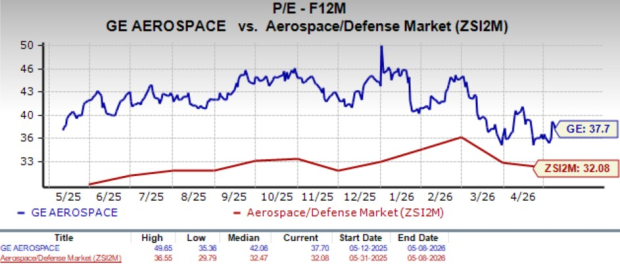

Valuation Remains an Overhang

GE Aerospace is trading at a forward 12-month price-to-earnings (P/E) ratio of 37.70X, higher than the industry average of 32.08X. This elevated valuation could make the stock vulnerable to further pullbacks if market sentiment sours.

Image Source: Zacks Investment Research

In comparison with GE’s valuation, its peers, RTX Corp. and Textron, are trading cheaper. Notably, RTX Corp. and Textron are currently trading at 24.70X and 13.27X, respectively.

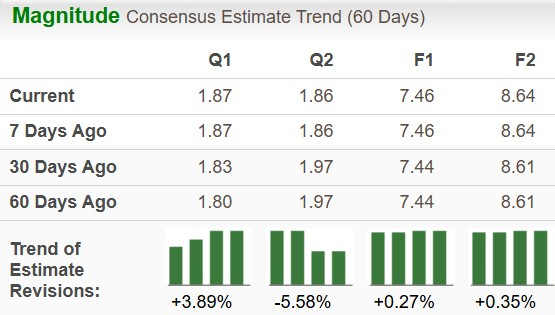

Earnings Estimate Revision

The Zacks Consensus Estimate for GE’s 2026 earnings has inched up 0.3% to $7.46 per share over the past 60 days, indicating year-over-year growth of 17.1%. The consensus mark for 2027 earnings increased 0.4% to $8.64 per share, indicating a year-over-year increase of 15.7%.

Image Source: Zacks Investment Research

Should You Buy GE Stock Now?

GE Aerospace’s strong foothold and persistent strength in the commercial and defense aerospace markets, driven by solid build rates and a robust defense budget, bode well for growth. However, escalating operating expenses, high debt level and premium valuation are limiting this Zacks Rank #3 (Hold) company’s near-term prospects.

While current shareholders should hold their positions, new investors should wait for the stock to retract some of its recent gains and provide a better entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

GE Aerospace (GE): Free Stock Analysis Report

Textron Inc. (TXT): Free Stock Analysis Report

RTX Corporation (RTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).