Taiwan Semiconductor Manufacturing Company (TSM), headquartered in Hsinchu, Taiwan, is the world’s largest and most vital pure-play semiconductor foundry. Founded in 1987 by Morris Chang, TSMC controls over 70% of the advanced foundry market share, serving as the sole manufacturer for tech giants like Apple (AAPL), Nvidia (NVDA), Advanced Micro Devices (AMD), and Qualcomm (QCOM). As the industry transitions into the artificial intelligence era, TSMC’s state-of-the-art silicon fabrication facilities serve as the foundational bedrock for cutting-edge microchips, powering everything from advanced generative AI data centers to smartphones and autonomous vehicles.

Taiwan Semiconductor Stock Rallies

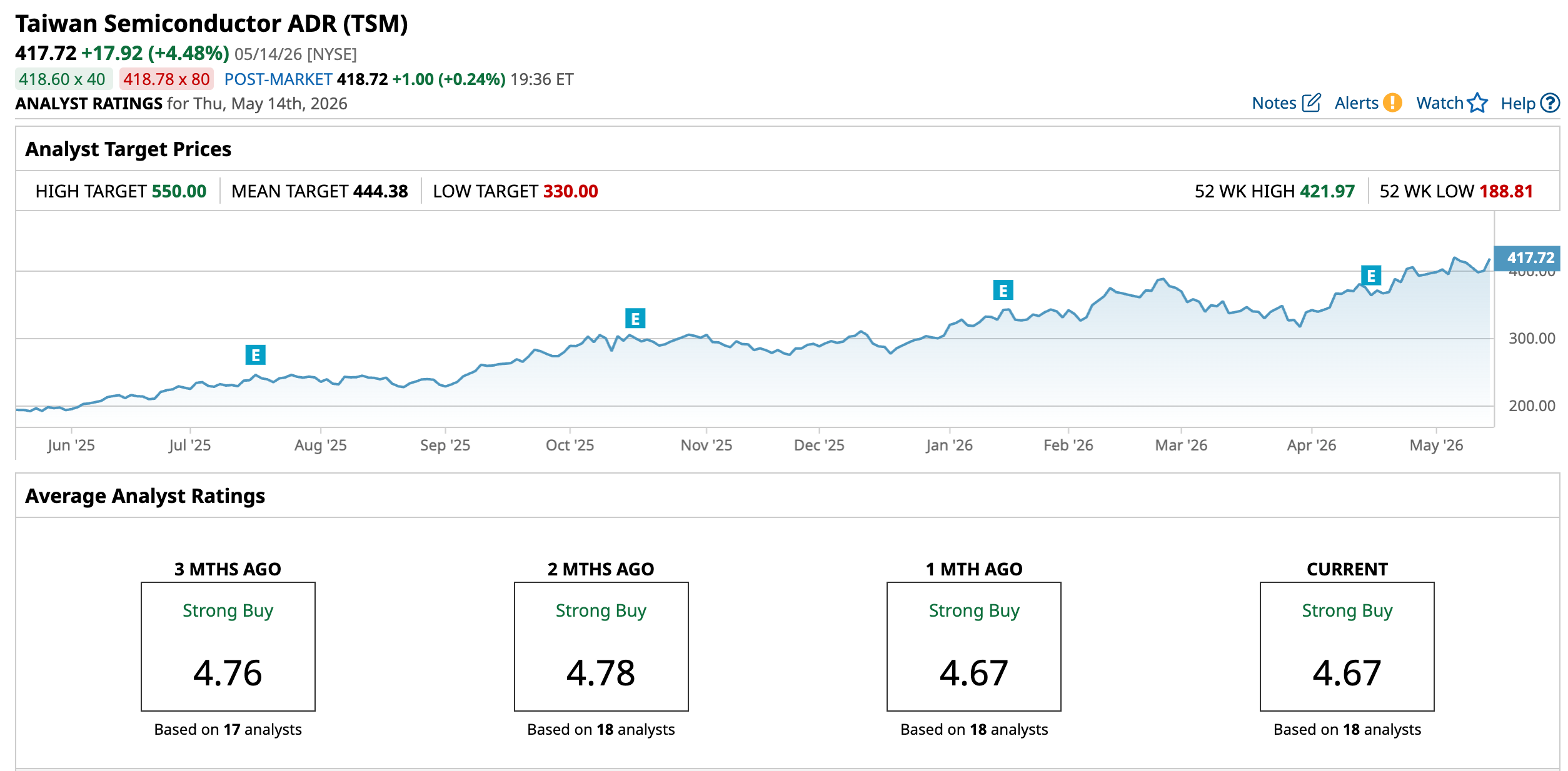

Taiwan Semiconductor stock has staged an historic, AI-fueled bull run, delivering an impressive 37.46% gain year-to-date (YTD) and skyrocketing 114.48% over the past twelve months. Investors have heavily accumulated shares, driving the price to its all-time high of $421.00. This structural re-rating reflects Wall Street’s immense confidence in TSMC’s unrivaled pricing power and absolute monopoly over leading-edge chip production, comfortably offsetting broader macroeconomic fluctuations and localized geopolitical concerns.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In comparison to the broader market, TSM has delivered staggering alpha over the past year, significantly outperforming the Nasdaq Composite Index. Driven by the relentless accumulation of high-performance computing (HPC) leaders, TSM’s 115% annual return nearly tripled the healthy double-digit gains of the tech-heavy benchmark.

www.barchart.com

www.barchart.com TSMC Results

TSMC delivered an exceptional financial performance for the first quarter of 2026, fueled by an unstoppable surge in AI accelerator demand. Total revenue reached $35.90 billion, representing a massive 35.1% increase year-over-year (YOY) and beating analyst estimates.

Profitability blew past expectations, with the company achieving a stellar 66.2% gross margin and a 58.1% operating margin, driven by exceptional capacity utilization and structural cost improvements. High-Performance Computing (HPC) remained the primary growth catalyst, now accounting for a staggering 61% of total revenue, while advanced nodes (3nm, 5nm, and 7nm) made up 74% of total wafer revenue.

Looking ahead, management provided a highly bullish outlook, raising full-year 2026 revenue guidance to above 30% growth in U.S. dollar terms. To support this massive multi-year capital cycle, TSMC is shifting its 2026 capital expenditure budget toward the absolute high end of its $52 billion to $56 billion range. The company expects Q2 2026 revenue to climb sequentially to between $39.0 billion and $40.2 billion. While the near-term deployment of its 2-nanometer (N2) node and international fab expansions will introduce a slight 2% to 3% margin dilution, TSMC's massive $106 billion cash reserve and absolute technological leadership ensure it remains perfectly positioned to dominate the global AI infrastructure wave.

TSMC Boosts Global Chip Estimates

Taiwan Semiconductor has aggressively raised its 2030 global semiconductor market forecast to exceed $1.5 trillion, up from its prior $1 trillion estimate. According to presentation materials from its tech symposium, high-performance computing (HPC) and AI will command a dominant 55% share of this market, followed by smartphones at 20% and automotive at 10%. To meet this explosive demand, including an 11-fold surge in AI accelerator wafer demand from 2022 to 2026, TSMC is accelerating its global footprint, planning nine phases of wafer fabs and advanced packaging facilities in 2026 alone.

Technologically, the foundry projects a massive 70% CAGR from 2026 to 2028 for its advanced 2-nanometer and next-generation A16 chip capacity. Furthermore, its crucial CoWoS advanced packaging capacity is forecast to grow at an 80% CAGR between 2022 and 2027.

Regionally, TSMC is expanding rapidly. Its first Arizona fab is operational with a second slated for 2026 tool move-in. Its second Japan fab has been upgraded to 3-nm nodes due to intense demand, and construction on its automotive-focused German facility remains on schedule.

Analysts Take on TSM

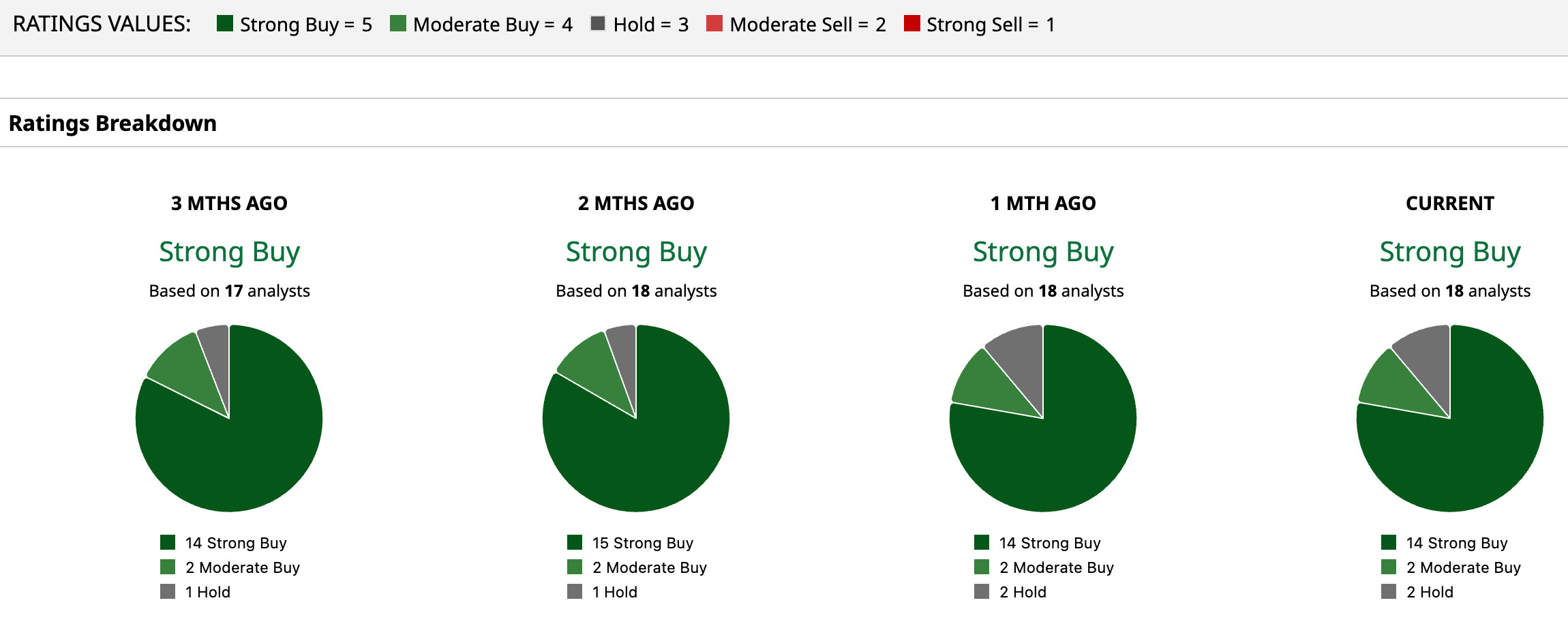

Taiwan Semiconductor’s upgraded $1.5 trillion global chip market forecast by 2030 reinforces its position as the ultimate, indispensable play on the AI revolution. The stock commands a definitive consensus "Strong Buy" rating, backed by 14 "Strong Buy" and 2 "Moderate Buy" designations across 18 analyst reviews. With a mean price target of $444.38, TSM offers a steady 6.38% projected upside from its current market price.

While its massive capital expenditure cycle and localized geopolitical risks require patience, the company's absolute monopoly over advanced node manufacturing and soaring CoWoS demand make TSM a foundational cornerstone for any long-term technology portfolio.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $1.5 Trillion Reason to Buy Taiwan Semi Stock Here Dear Dell Stock Fans, Mark Your Calendars for May 28 Nokia Shares Jumped After Cisco’s Strong Quarterly Results. NOK Could Be the Next Networking Winner. Anthropic’s Project Glasswing Could Be a Major Catalyst for Verizon Stock