As Wells Fargo & Company WFC moves beyond years of regulatory and operational restructuring, the focus is increasingly shifting toward the bank’s ability to translate efficiency gains into stronger shareholder returns. The bank has already made meaningful progress on efficiency, but first-quarter 2026 results show that the path to higher returns will depend on balancing cost discipline with investment in technology, compliance and growth initiatives.

In the first quarter of 2026, Wells Fargo reported a return on tangible common equity (ROTCE) of 14.5%, up from 13.6% in the year-ago quarter, while return on equity (ROE) improved to 12.2% from 11.5%. The company’s efficiency ratio also improved to 67% from 69% a year earlier, indicating that revenue growth outpaced expense growth despite higher absolute expenses.

Management’s 2026 expense guidance is central to the efficiency story. WFC expects non-interest expenses of $55.7 billion for 2026, suggesting a slight hike from the 2025 reported level. This target comes as the company continues to spend on technology, strategic initiatives and other investments. The company expects 2026 net interest income of $50 billion, suggesting that operating leverage could improve if revenue momentum continues while expenses remain controlled.

Wells Fargo has been pursuing cost-cutting measures since the third quarter of 2020, including streamlining its organizational structure, closing branches and reducing headcount. Importantly, headcount declined 6.5% year over year to 201,000 at the end of first-quarter 2026, marking the 23rd consecutive quarter of reductions. Branch optimization also remains part of the strategy, with retail branches down 1.5% year over year to 4,093 by the end of March 31, 2026.

These actions matter because WFC is targeting a medium-term ROTCE of 17-18%, up from its earlier 15% goal. The removal of the asset cap and closure of regulatory constraints give the bank more room to expand deposits, loans and fee-based businesses, which could make expense discipline more powerful.

Overall, Wells Fargo’s efficiency strategy appears to be delivering gradual improvements in profitability and operating leverage. Continued expense discipline, combined with stronger revenue opportunities following the removal of the asset cap, could support further gains in ROTCE over the medium term.

However, the path toward the bank’s 17-18% target will depend on management’s ability to balance cost reductions with sustained investments in technology, compliance and growth while navigating a still-uncertain operating environment.

How WFC Peers Are Expected to Fare in Terms of ROTCE

Citizens Financial Group, Inc. CFG expects a return on average tangible common shareholders’ equity of 16-18% over the medium term. The execution of the target will be supported by Citizens Financial Group’s strategic initiatives and the NII tailwinds expected between 2025 and 2027. CFG expects the CET1 ratio to be 10-10.5%, while the efficiency ratio is projected to be in the mid-50s.

Meanwhile, Citigroup, Inc. C is advancing its multi-year strategy to streamline operations and focus on its core businesses. Aligned with its goal of achieving leaner operations, Citigroup has overhauled its operating model and leadership structure, reduced bureaucracy and complexity while enhancing efficiency.Citigroup anticipates achieving $2-2.5 billion in annualized run-rate savings by 2026, reflecting the tangible benefits of its simplification and efficiency initiatives. ROTCE is expected to be 10-11% by 2026-end.

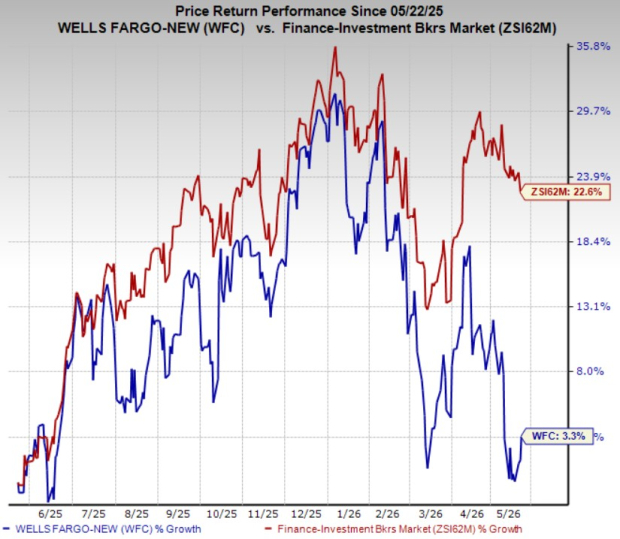

WFC’s Price Performance & Zacks Rank

Shares of Wells Fargo have gained 3.3% in the past year compared with the industry’s growth of 22.6%.

Image Source: Zacks Investment Research

Wells Fargo currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Wells Fargo & Company (WFC): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

Citizens Financial Group, Inc. (CFG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).