Jacobs Solutions Inc. (J) has grown into one of the world’s largest professional services firms, with a $13.5 billion market cap and operations spanning more than 50 countries. The company provides engineering, technical consulting, and project management services across infrastructure, water, environmental, energy, and defense markets globally.

While the business keeps busy on all fronts, shares of the Dallas, Texas-based company have been telling a very different story in the market. The stock slid 9.6% over the last 52 weeks and bled another 13.4% year-to-date (YTD) in 2026, putting the company on the wrong side of the broader market rally.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The S&P 500 Index ($SPX) posted a 27.9% gain over the same 52-week window and has already added 9.2% in 2026, making the gap between Jacobs and the index wider.

The State Street Industrial Select Sector SPDR ETF (XLI) painted an equally unflattering comparison, climbing 21.6% over the last 52 weeks while tacking on another 10.7% YTD, leaving Jacobs trailing its own sector by a wide margin.

www.barchart.com

www.barchart.com The stock briefly found its footing on May 5 when Jacobs reported Q2 FY2026 results, jumping 4.4% as investors responded to what looked like a solid quarter on the surface. However, the optimism had a very short shelf life as shares dropped 7.3% in the very next trading session once the full picture came into focus.

Revenue grew 27% year over year to $3.7 billion during the quarter, clearing the analyst estimate of $3.3 billion. The trouble, though, ran deeper in the numbers, as Jacobs posted a GAAP net loss of $43 million that the company attributed to costs tied to its recent acquisition of PA Consulting.

Adjusted EPS came in at $1.75, up 22.4% year over year and comfortably beating the analyst estimate of $1.64 and showing that the underlying business held its ground, but that strength was not enough to hold investor confidence together.

Looking ahead, the picture appears encouraging. FY2026 wraps up in September, and analysts are penciling in an 18% year over year jump in diluted EPS to $7.22, reflecting growing confidence in where the business is heading. The confidence draws further backing from the fact that Jacobs has topped EPS estimates in each of the last four consecutive quarters.

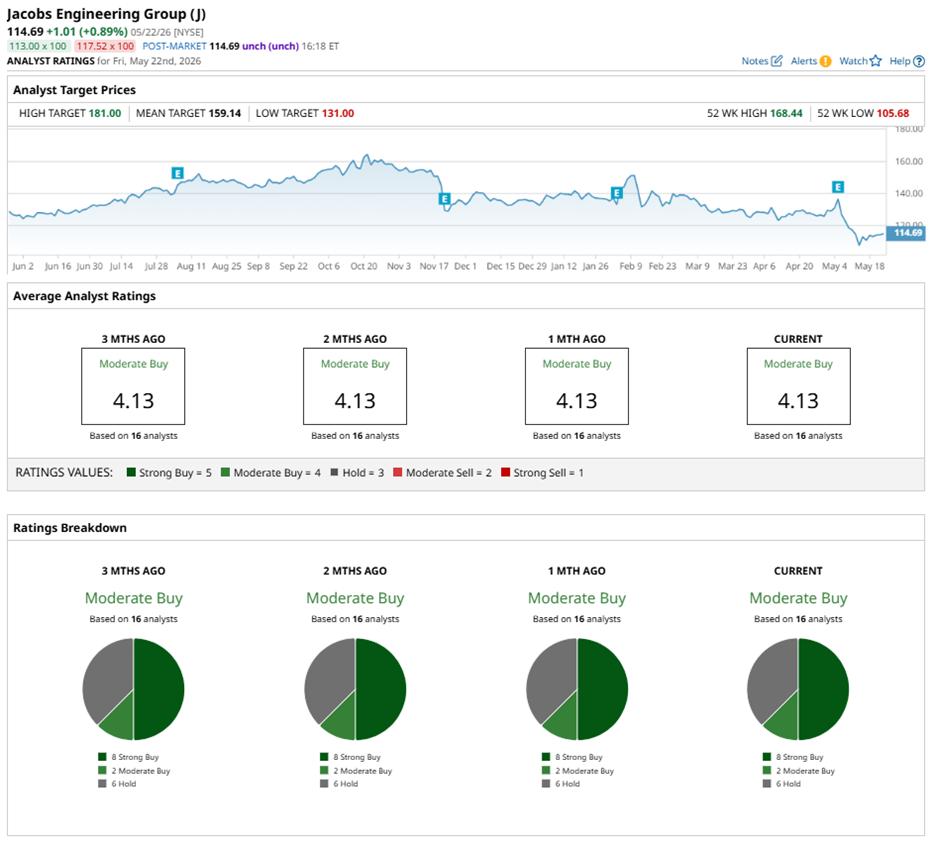

Wall Street has settled on an overall "Moderate Buy" rating for J stock, though the breakdown among analysts reveals a clear lean toward the bullish side. Out of 16 analysts currently covering the company, eight hold a "Strong Buy" rating, two go with "Moderate Buy," and six remain on the fence with a "Hold."

www.barchart.com

www.barchart.com The distribution has not shifted an inch over the last three months, when eight analysts also carried "Strong Buy" ratings on the stock.

The steady conviction only grew louder after the company’s strong second quarter showing. On May 9, RBC Capital analyst Sabahat Khan lifted his price target on J stock to $169 from $160 while maintaining an “Outperform” rating, citing impressive Q2 results and upbeat forward guidance.

J stock’s average price target of $159.14 suggests potential upside of 38.8%. However, the Street-High target of $181 set by Citigroup analyst Andrew Kaplowitz suggests a gain of 57.8% from current levels. Kaplowitz nudged his target price up to $181 from $180 and reiterated a “Buy” rating, making Citigroup the stock’s loudest cheerleader at the moment.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Qualcomm Stock Is the Sleeping Giant of the AI Revolution. It’s Starting to Wake Up. Wall Street Is Warming Back Up to CoreWeave Stock. Long-Term Demand Is Helping. Palantir’s AI Surge Meets Market Correction. Buy the PLTR Stock Dip Now. 1 Outstanding AI Stock You’ll Regret Ignoring 10 Years From Now