Snowflake SNOW is set to release first-quarter fiscal 2027 results on May 27.

The Zacks Consensus Estimate for first-quarter fiscal 2027 earnings has remained steady at 32 cents per share over the past 30 days, indicating a year-over-year increase of 33.33%. The consensus mark for first-quarter revenues is pegged at $1.32 billion, indicating an increase of 26.85% from the year-ago quarter’s reported figure.

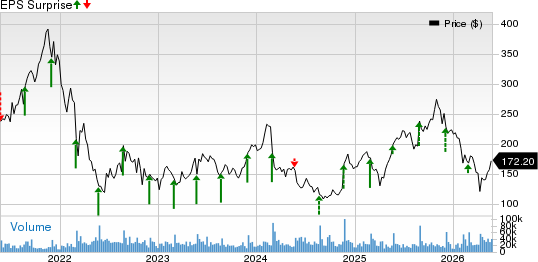

SNOW’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, with the average earnings surprise being 18.78%.

Let’s see how things have shaped up for SNOW prior to this announcement:

Snowflake Inc. Price and EPS Surprise

Snowflake Inc. price-eps-surprise | Snowflake Inc. Quote

Factors to Note for SNOW’s Q1

Snowflake’s fiscal first-quarter performance is expected to have reflected an expanding clientele, driven by strong AI capabilities and a rich partner base.

SNOW continues to benefit from strong adoption and increasing usage of its platform, as reflected by the net revenue retention rate of 125% in the fourth quarter of fiscal 2026. In the same quarter, Snowflake added 740 net new customers, up 40% year over year. The company now has 733 customers spending more than $1 million annually, up 27% year over year, and 56 customers spending more than $10 million annually, up 56% year over year. This trend is expected to have continued in the to-be-reported quarter as well.

Expanding clientele is expected to have benefited the top-line growth. For the first quarter of fiscal 2027, Snowflake expects product revenues in the range of $1.262-$1.267 billion. The projection range indicates year-over-year growth of 27%. The Zacks Consensus Estimate for fiscal first-quarter 2027 product revenues is pegged at $1.26 billion, indicating 26.88% growth from the figure reported in the year-ago quarter.

The Zacks Consensus Estimate for customers with trailing 12-month product revenues greater than $1 million is currently pegged at 758, indicating a 25.08% increase from the year-ago quarter. The consensus mark for total customers is pegged at 13,758, indicating an increase of 430 net new customers in the to-be-reported quarter.

However, lower gross margins from new AI product investments and a 150-basis point free cash flow headwind from the Observe acquisition are expected to hurt SNOW in the to-be-reported quarter.

SNOW Shares Underperform Sector

Snowflake shares have plunged 21.5% in the year-to-date period against the Zacks Computer & Technology sector’s increase of 17.5%. The company’s shares have outperformed the Zacks Internet Software industry’s decline of 11.5% over the same time frame.

SNOW Stock’s Performance

Image Source: Zacks Investment Research

SNOW Stock Is Currently Overvalued

Snowflake stock is not so cheap, as the Value Score of F suggests a stretched valuation at this moment.

In terms of forward 12-month Price/Sales, SNOW is trading at 9.4X, higher than the Internet Software industry’s 3.81X.

Valuation: SNOW Is Trading at a Premium

Image Source: Zacks Investment Research

Snowflake Rides on Strong Portfolio

SNOW’s expanding portfolio has been noteworthy. In 2026, Snowflake launched more than 430 product capabilities, including Snowflake Intelligence, Cortex Code, Snowflake OpenFlow, and Snowflake Postgres. These innovations enhanced the platform’s usability and scalability.

The company’s AI-driven products, particularly Snowflake Intelligence and Cortex Code, have been a major growth driver. In 2026, Snowflake Intelligence, which provides enterprise-grade agent capabilities, has been adopted by more than 2,500 accounts within just three months of its launch, nearly doubling quarter over quarter. Cortex Code, a transformational coding agent, has been embraced by more than 4,400 customers, enabling faster development and deployment of AI-powered applications.

SNOW Suffers From Stiff Competition

Despite Snowflake’s expanding portfolio and partner base, the company is facing stiff competition from the likes of major players like Oracle ORCL, Amazon AMZN, and Alphabet GOOGL, which are also expanding their footprint in the AI space.

Oracle’s expanding portfolio has been noteworthy. In April 2026, Oracle expanded AI capabilities in Oracle AI Database@Google Cloud, introducing Gemini-powered agents for natural language data access, enhancing enterprise insights, productivity and multicloud data innovation.

Amazon’s AI initiatives gained significant momentum during the first quarter of 2026. Amazon’s cloud computing platform, Amazon Web Services' chips business, including Graviton, Trainium, and Nitro, exceeded a $20 billion annual revenue run rate and is growing triple-digit percentages year over year.

Alphabet has been growing rapidly in the booming cloud-computing market. In the first quarter of 2026, Alphabet's cloud revenues surged 63% year over year to roughly $20 billion. This acceleration is largely fueled by enterprise adoption of generative AI offerings such as Gemini, with revenue from AI-based cloud products growing nearly 800% year over year.

Conclusion

Despite SNOW’s robust portfolio, challenging macroeconomic uncertainties, rising AI costs, and stiff competition from hyperscale cloud providers remain headwinds. The stretched valuation also makes the stock risky right now.

Snowflake currently carries a Zacks Rank #3 (Hold), which implies that investors should wait for a favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

Snowflake Inc. (SNOW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).