Insulet Corporation PODD is leaning on Omnipod 5 momentum to open 2026 with a faster growth profile than most medical products peers. Demand across Type 1 diabetes and early Type 2 diabetes is the key driver, supported by a recurring pod model that naturally scales with usage.

With broad pharmacy access helping reach more patients, execution now hinges on product upgrades, international expansion and disciplined spending. Investors also have to weigh near-term quality, cost and reimbursement risks that can shape results over the next few quarters.

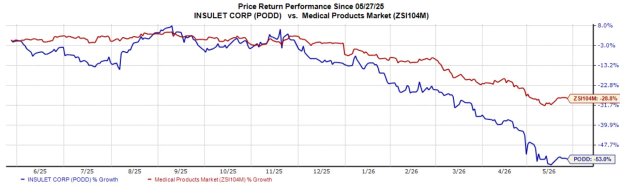

In the past year, Insulet’s shares have plunged roughly 53% compared with the industry’s decline of 28.8%.

Image Source: Zacks Investment Research

Insulet’s Q1 Beat and Higher 2026 Growth Outlook

First-quarter 2026 results came in ahead of expectations. Revenue reached $761.7 million, up 33.9% year over year, and up 30.1% in constant currency. Adjusted earnings per share were $1.42, up 39.7% from the prior-year quarter.

Both the top and bottom lines cleared consensus, with the revenue surprise at 4.6% and the adjusted earnings per share surprise at roughly 24.8%.

After the quarter, management raised full-year 2026 constant-currency revenue growth guidance to 21% to 23%. The company continues to target roughly 100 basis points of adjusted operating margin expansion, signaling an intent to grow while still capturing scale benefits.

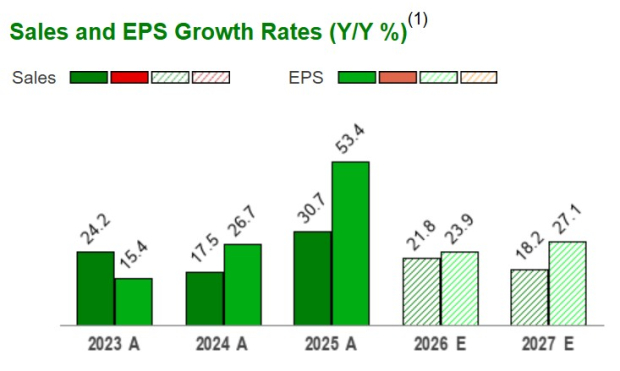

Estimates for PODD Heading North

The Zacks Consensus Estimate for Insulet’s 2026 sales and EPS implies a year-over-year improvement of 22.4% and 29.4%, respectively. The bottom-line estimates have moved northward in the past 60 days.

Image Source: Zacks Investment Research

PODD Upgrades Add 100 mg/dL Target, Libre 3 Plus

A near-term catalyst is the latest Omnipod 5 algorithm update. The enhancement adds a new 100 mg/dL target glucose option, giving users another way to personalize automated insulin delivery settings.

On sensor connectivity, Insulet completed a limited U.S. launch of Omnipod 5 integrated with Abbott Laboratories (ABT) FreeStyle Libre 3 Plus. A broader rollout of Libre 3 Plus integration is planned in the coming weeks, expanding sensor choice within the Omnipod 5 ecosystem.

Insulet Expands Internationally as Omnipod 5 Hits 19 Markets

International growth remains an important lever in 2026. Management highlighted that global customer base growth was nearly 25% year over year, supported by higher new customer starts and retention trends similar to the prior year.

Outside the United States, growth is being driven by new customer starts and conversions from Omnipod DASH to Omnipod 5. Omnipod 5 is now available in 19 countries, while Omnipod products are available overall in 25 countries.

The outlook reflects that momentum. Management expects international Omnipod revenue is projected to increase 26% to 28%, supported by both volume expansion and mix benefits.

Insulet’s Margin Plan Meets Correction and Cost Risks

Investors also need to balance the growth narrative with near-term risks. In March 2026, Insulet issued a voluntary medical device correction for certain lots of Omnipod 5 pods and accrued an estimated $11.7 million liability in the quarter. Management estimates total correction and related costs of about $30 million, with more than half expected in 2026 and the remainder in 2027 due to incremental manual inspections until automation is implemented.

Product transitions and supply-chain variability can also pressure gross margin. Management cited incremental raw material and shipping costs tied to the ongoing conflict in the Middle East as an offset to its 2026 margin outlook.

Large diabetes technology peers like Medtronic PLC MDT and DexCom, Inc. DXCM add to the competitive backdrop as adoption expands.

PODD Takeaways for the Next Few Quarters

For the next few quarters, investors can track three signposts. First is the pace and breadth of the broader Libre 3 Plus integration rollout and uptake of the latest Omnipod 5 algorithm update.

Second is adoption momentum across U.S. Type 1 and Type 2 markets, alongside international new customer starts and the conversion cycle from Omnipod DASH to Omnipod 5.

Third is progress against 2026 targets, including 21% to 23% constant-currency revenue growth and roughly 100 basis points of operating margin expansion, while monitoring correction-related costs and reimbursement friction. With a Zacks Rank #3 (Hold), execution on these signposts is likely to shape sentiment through the year. You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Medtronic PLC (MDT): Free Stock Analysis Report

DexCom, Inc. (DXCM): Free Stock Analysis Report

Insulet Corporation (PODD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).