Dollar Tree, Inc. DLTR used its first-quarter 2026 earnings call to argue that better store execution, tighter inventory control and a broader multi-price assortment are starting to translate into more durable margin gains. Management’s tone was constructive, but it kept a cautious stance regarding the second half.

That balance mattered. The quarter topped the Zacks Consensus Estimate for earnings and net sales, but the bigger investor question was how much of the upside can hold as fuel costs, tariffs and a pressured lower-income consumer remain in the backdrop.

DLTR Leans on Better Execution

Chief executive officer Michael Creedon framed the quarter around operational progress rather than headline sales alone. He pointed to margin expansion, improving store standards and early gains in shrink control as evidence that the company’s strategy is gaining traction.

That message was backed by the reported numbers. Adjusted earnings per share rose to $1.74 from $1.26 a year ago, whereas net sales increased 7.2% to about $5 billion and comparable-store sales rose 3.5%.

The quarter also beat expectations. Based on the Zacks data, DLTR beat the Zacks Consensus Estimate for earnings by 13.5% and exceeded the revenue projection by 0.14%.

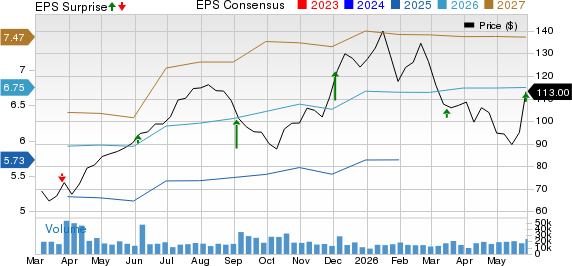

Dollar Tree, Inc. Price, Consensus and EPS Surprise

Dollar Tree, Inc. price-consensus-eps-surprise-chart | Dollar Tree, Inc. Quote

Dollar Tree Keeps Pushing Multi-Price

Creedon described multi-price as a core growth driver, especially as Dollar Tree tries to turn seasonal traffic into more everyday demand. He said that the company is using the assortment shift to build relevance in household consumables, toys and beverages, while still protecting its opening price-point value perception.

Management said that roughly 85% of sales still come from items priced at $2 and below, a figure meant to reassure investors that the chain is expanding price points without walking away from its value identity.

The same theme came up in Q&A. Executives said that recent center-store food price changes affected less than 5% of the assortment, and were intended to restore brand relevance and improve price clarity, not to broadly reprice the box.

DLTR Hikes Guidance but Stays Guarded

Chief financial officer Stewart Glendinning raised the 2026 adjusted earnings outlook to $6.70-$7.10, while maintaining a sales view of $20.5-$20.7 billion and comparable-sales growth of 3-4%. Second-quarter 2026 adjusted earnings are projected to be $1-$1.15 on sales of $4.8-$4.9 billion.

Still, Glendinning made clear that the raise was not a clean flow-through from the first-quarter beat. He said that the company is assuming higher fuel costs last through the year, current tariff rates remain in place through July and no tariff refunds are included in the guidance.

That framing left the impression of a management team willing to bank some upside but not ready to declare the back half secure.

Dollar Tree Faces Traffic Test

Traffic remains the key debate. Comparable sales were driven by a 4.5% increase in ticket, while traffic declined 1%, though management said that it marked a 20-basis-point sequential improvement from the fourth quarter.

Creedon argued that traffic should improve in the second half as Dollar Tree laps prior pricing actions, sharpens marketing and keeps lifting store conditions. He also said that the chain historically becomes more relevant when consumers turn more value-focused.

Glendinning added that all income cohorts posted positive comparable sales in the quarter, even as lower-income shoppers remained under pressure from several years of inflation and higher gas prices.

DLTR Q&A Zeroes In on Costs

A JPMorgan analyst asked what drove the first-quarter 2026 upside, and Glendinning credited better shrink, favorable freight and some merchandise margin help. He said that tariffs were a year-over-year headwind but were offset by the company’s mitigation actions and did not drive the beat.

Questions also focused on freight and fuel. Glendinning said that base freight rates have stayed manageable, but fuel surcharges and some driver-cost pressure are built into the outlook for the rest of the year.

On capital allocation, management highlighted $595 million of first-quarter buybacks, another $98 million repurchased quarter to date and $1.3 billion still remaining under the authorization.

Dollar Tree Leaves Call With Measured Confidence

The clearest takeaway from the earnings call was that management believes execution is improving faster than the market may have expected. Store standards, shrink control, inventory turns and marketing discipline were presented as company-controlled levers that can keep supporting profit growth.

At the same time, leadership did not minimize external risks. Fuel, tariffs and consumer pressure were recurring caveats, which kept the tone constructive but restrained rather than aggressive.

Zacks Signals for DLTR

DLTR currently carries a Zacks Rank #3 (Hold), alongside a Value Score of B, a Growth Score of A, a Momentum Score of F and a VGM Score of A. Under the Zacks framework, a Rank #3 can still be held, while stronger Style Scores, such as A or B, point to more attractive value or growth characteristics than weaker grades. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The combination suggests a mixed near-term signal: solid value and growth characteristics, weak momentum and an overall VGM profile that screens well. Even so, the Zacks Rank can change as earnings estimate revisions adjust after the quarter, which keeps the post-call setup more watchful than definitive.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dollar Tree, Inc. (DLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).