Palantir Technologies (PLTR) has been the most controversial stock this year. Meanwhile, Snowflake (SNOW) has quietly grown its cloud and AI business. But while both companies are riding the AI wave, only one appears poised to dominate enterprise AI over the next decade.

The Case for Palantir

Palantir stock has been on a roller coaster ride this year, surging into the spotlight during the U.S.-Iran conflict as a critical AI and defense software provider for the U.S. government. Palantir builds software platforms that help governments and companies organize massive amounts of data, analyze it with AI, and make faster operational decisions.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

While the bulls support the rising demand for its software platforms, Foundry, Gotham, and AIP (Artificial Intelligence Platform), the bears argue that the rapid growth has pushed its valuation sky-high. PLTR stock is down 19% year-to-date, underperforming the broader market. Nonetheless, the company has steadily become an operational backbone connecting AI systems to governments, enterprises, factories, supply chains, defense systems, and critical infrastructure.

www.barchart.com

www.barchart.com In the first quarter, Palantir’s revenue surged to $1.6 billion, an 85% growth year-over-year (YOY), while adjusted earnings per share rose 153% YOY to $0.33. During the quarter, the company closed $1.3 billion in commercial total contract value bookings, including its third consecutive quarter above $1 billion in U.S. commercial bookings. Over the last 12 months, the company generated $4.7 billion in U.S. commercial TCV bookings, representing 115% growth compared to the prior year.

Commercial revenue grew 95% to $774 million from the prior-year quarter. Government demand remained equally strong, with revenue up 76% YOY to $858 million, while U.S. government revenue climbed 84% to $687 million. The company ended the quarter with $11.8 billion in total remaining deal value and $4.5 billion in remaining performance obligations, which indicates unrealized revenue.

Management is confident that AIP will gradually replace conventional enterprise software as commercial use grows across industries. GE Aerospace (GE), Ondas (ONDS), Moder, and Freedom Mortgage all provided encouraging input on how AIP has evolved into a core operational infrastructure platform for enterprises. Palantir is no longer solely a software company. If AI truly becomes embedded into every major sector over the next decade, Palantir may end up owning one of the most important layers of that entire AI stack.

Analysts expect Palantir’s earnings to increase by 95% in 2026, followed by 42% in 2027. Investors' high expectations are reflected in Palantir’s valuation, with the stock trading at 65 times forward earnings.

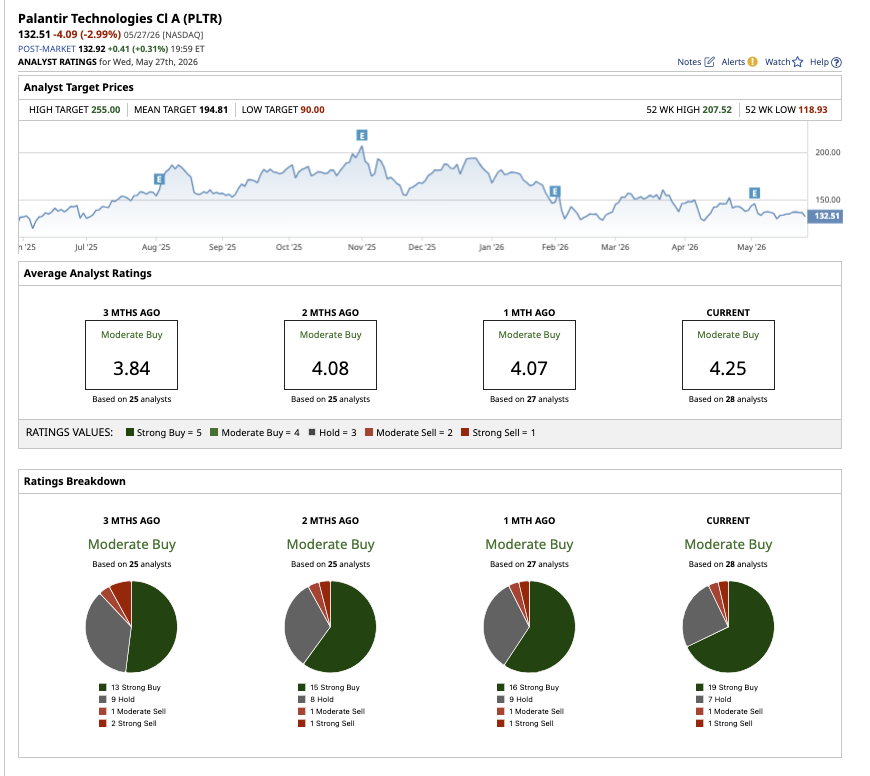

On Wall Street, PLTR stock is an overall “Moderate Buy.” Of the 28 analysts covering PLTR stock, 19 rate it as a “Strong Buy,” seven have a “Hold” rating, one analyst has a “Moderate Sell,” and one analyst has a "Strong Sell" rating. Based on the average price target of $194.81, analysts see PLTR stock climbing as much as 36% from current levels. The high price estimate of $255 suggests a potential upside of 78% from here.

www.barchart.com

www.barchart.com The Case for Snowflake

Snowflake is a cloud software company that helps businesses store, organize, share, and analyze massive amounts of data across different systems and cloud platforms. Snowflake stock has put investors' patience to the test this year despite strong financials. Before a 36% rally on Thursday, the stock had dipped 15% over the past year and 19% YTD. Now it sits at 17% up over 52 weeks and 9% year-to-date. An explosive Q1 print released on May 27 and a $6 billion deal with Amazon (AMZN) have already altered the stock’s trajectory.

www.barchart.com

www.barchart.com In the first quarter of fiscal 2027, Snowflake reported revenue of $1.39 billion, up 33% YOY, while adjusted EPS came in at $0.39, both comfortably ahead of Wall Street expectations. Product revenue climbed 34% YOY to $1.33 billion, while net revenue retention improved to 126%. Snowflake added 616 net new customers during the quarter, bringing its total customer count to 13,912. The company now has 64 customers spending more than $10 million annually on the platform, while 779 spend more than $1 million each year.

But investors seem more excited about the upbeat guidance. Snowflake raised its full-year product revenue forecast to $5.84 billion from $5.66 billion, signaling stronger enterprise AI demand than expected. The biggest highlight of the quarter, however, was the expanded $6 billion, five-year deal with Amazon Web Services (AWS). The partnership focuses heavily on generative and agentic AI infrastructure, deeper AI integration, and helping enterprises migrate AI workloads onto Snowflake’s platform. It also expanded its partnership with OpenAI through a $200 million agreement and deepened integration with SAP to connect enterprise business data across AI systems.

Analysts estimate Snowflake’s earnings will increase by 53% to $1.92 per share in fiscal 2027, with earnings increasing by 35% the next year. SNOW stock is currently valued at a premium of 91 times forward estimated earnings for 2027. The combination of strong growth in Q1, improving margins, raised guidance, and growing AI momentum has put all eyes back on Snowflake. However, Snowflake still operates mainly as a data cloud company rather than a fully integrated operational AI platform like Palantir.

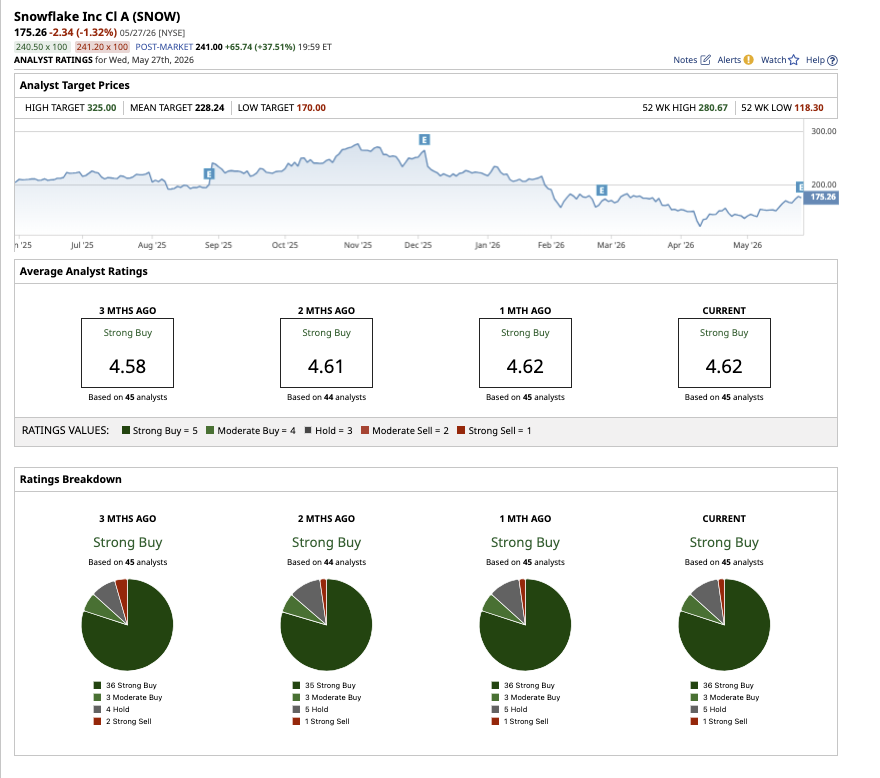

On Wall Street, SNOW stock is an overall “Strong Buy.” Of the 45 analysts covering PLTR stock, 36 rate it as a “Strong Buy,” three have a “Moderate Buy" rating, five have a “Hold” rating, and one analyst has a "Strong Sell" rating. Based on the high price target of $325, analysts see PLTR stock climbing as much as 36% from current levels.

www.barchart.com

www.barchart.com Only One AI Software Stock Looks Built for the Next Decade

Both Palantir and Snowflake are benefiting from the AI boom and investors expect massive growth from these critical software providers. This expectation is reflected in their lofty valuations. In my opinion, Palantir appears to have the stronger strategic position in the broader AI ecosystem. Its staggering revenue growth, expanding profitability, rising government and commercial adoption worldwide, and growing role in operational AI make it one of the few software companies that genuinely looks built for the next decade of AI.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Palantir vs. Snowflake: Only 1 AI Software Stock Looks Strong for the Next Decade S&P Futures Gain on Hopes for U.S.-Iran Deal; Dell Pops on Blowout Earnings Ford Stock Is Moving Like Tesla Now. Its Results Can’t Justify the Premium. Nano Nuclear Stock Looks Very Risky Despite Its Recent Acquisition