Blue Owl Capital Inc. OWL is priced for a “prove it” stretch. The shares recently traded around $10, and the long-term stance for the stock is Neutral.

That setup reflects mixed signals. Blue Owl has multiple growth lanes that can expand fee sources, but near-term headwinds in private-credit liquidity, capital deployment timing, and expenses can keep sentiment choppy.

OWL Trades Below Key Benchmarks on Forward Earnings

OWL trades at 10.67X forward 12-month earnings. That is below the industry at 13.56X.

Image Source: Zacks Investment Research

The discount suggests the market is not simply paying for scaled alternative-asset exposure. Investors appear to be weighing near-term friction in private credit and the risk that fee growth does not arrive as smoothly as embedded capital pools imply.

The valuation framework also shows how expectations are being set. The $10.75 price target corresponds to 11.56X forward 12-month earnings, modestly above the current multiple but still well below the broader benchmarks.

Blue Owl’s Growth Drivers Still Look Durable

Fundraising scale remains a core support for OWL. The company raised $42 billion in 2025, up from $27.5 billion in 2024 and $15.4 billion in 2023. Momentum carried into the first quarter of 2026 with $11 billion raised, and management expects 2026 fundraising to look similar to 2025.

Product breadth is widening the fee engine. Management is advancing newer strategies in digital infrastructure, net lease, and alternative credit. The mix of flagship closes and evergreen wealth products is positioned to keep fundraising durable across channels.

That feeds an organic growth narrative that has already been visible in earnings quality. Fee-Related Earnings revenues posted a 31% compound annual growth rate from 2021 to 2025, supported by diversification beyond direct lending and exposure to secular themes in infrastructure and artificial intelligence. The uptrend continued in the first quarter of 2026.

Image Source: Zacks Investment Research

OWL’s Fee Ramp Depends on Deployment Timing

A key swing factor is the pool of capital that is committed but not yet paying fees. As of March 31, 2026, AUM not yet paying fees totaled $29.9 billion, which Blue OWL expects would translate into about $349 million of annualized management fees once deployed.

The issue is timing. The company expects deployment to play out over roughly the next 12 to 24 months, but the cadence can vary by strategy and market conditions. Any elongation in deal closings can delay when those fees show up in results.

Muted sponsor merger and acquisition activity is part of the near-term constraint, and a back-half clustering of deployment would push fee recognition out. That dynamic can cap near-term upside even if the longer-run fee base is building.

Blue Owl Faces Redemption and Liquidity Friction

Liquidity and sentiment in private credit remain the most important near-term risk, especially in retail-oriented vehicles. Toward the end of 2025, non-traded business development companies saw slower flows and elevated redemption requests.

Blue Owl took actions to manage withdrawals and liquidity needs. In February, the firm restricted withdrawals at OBDC II after requests hit a 5% threshold and sold assets across affiliated funds to meet liquidity needs.

Redemption pressure also showed up in first-quarter 2026 disclosures. Management cited net outflows of roughly $170 million from OCIC and OTIC, while redemptions from non-traded business development companies were about $1.2 billion. If redemption activity persists or broadens, it can weigh on fundraising and fee growth.

OWL’s Credit Quality Monitoring Is a Must

Credit quality is a watch item for OWL, with particular attention on software and artificial intelligence-adjacent borrower exposure. Investors are becoming more cautious toward mid-sized technology companies where earnings durability and cash-flow visibility can be harder to assess.

The first-quarter 2026 insights were constructive on near-term indicators. Key direct lending measures such as the watch list, nonaccruals, amendment requests, and revolver draws did not show meaningful adverse movement, and the average annual loss rate remains 12 basis points.

Even so, monitoring needs to stay active. Spreads have begun to widen, and public company volatility can tighten equity cushions over time. A sustained macro slowdown could still translate into higher downgrade risk and more restructuring activity.

Blue Owl’s Expense Trajectory Can Swing the Story

Blue Owl is investing in distribution and product build-out, and expenses have been trending higher over time. Total expenses recorded a 2021-2025 compound annual growth rate of 8.4%, and expenses remained elevated in the first quarter of 2026.

In that quarter, total GAAP expenses rose 6% year over year to $644.3 million, driven by higher compensation and benefits costs. Management expects expenses to remain elevated due to steady franchise investments and higher revenue-related compensation costs.

For investors, the message is straightforward. The margin outlook improves if revenue growth outpaces expense growth as planned, including the expected 2026 FRE margin of 58.5% versus 58.3% in 2025. If that relationship flips, the valuation discount can persist.

OWL’s Bottom Line: What Would Change the View

The long-term Neutral stance fit the Blue Owl stock with clear growth avenues and real near-term friction. A decision-focused checklist starts with fundraising pace and the mix between flagship closes and evergreen wealth products.

Next, watch net flows and redemption activity, particularly across retail-oriented private-credit vehicles, along with any further steps taken to manage liquidity.

Finally, track the deployment cadence of fee-eligible AUM, signs of credit stress in direct lending indicators, and whether estimate revisions stabilize after recent downward changes noted for 2026 and 2027.

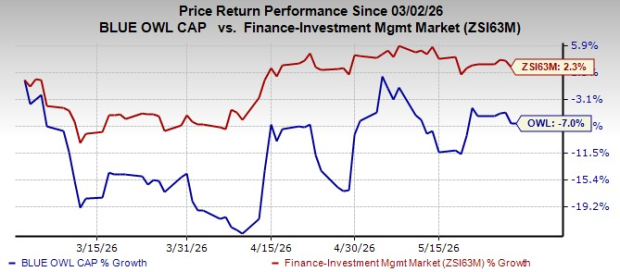

Over the past three months, shares of this Zacks Rank #4 (Sell) company have lost 7%, against the industry’s rally of 2.3%.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Image Source: Zacks Investment Research

In the meantime, OWL’s larger peers like Apollo Global Management APO and Blackstone Inc. BX can be useful reference points for how investors price alternative managers when flows and deployment momentum are strong compared with when liquidity concerns rise. Similar to Blue Owl, both Apollo Global and Blackstone witnessed higher-than-normal redemption requests in some of their flagship funds during the first quarter.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Blackstone Inc. (BX): Free Stock Analysis Report

Apollo Global Management Inc. (APO): Free Stock Analysis Report

Blue Owl Capital Inc. (OWL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).