Realty Income O and Prologis PLD are two of the best-known REITs, but they give investors very different kinds of real estate exposure. Realty Income, often called “The Monthly Dividend Company,” is built around long-term net leases, a large retail-heavy portfolio and a steady monthly payout. Prologis, on the other hand, is the global leader in logistics real estate, with warehouses, distribution assets, data center opportunities and energy-related growth tied to modern supply chains.

This is a useful comparison for investors looking beyond the broad REIT label. Realty Income offers stability, diversification and income dependability. Prologis offers exposure to logistics demand, digital infrastructure and a development platform that can create value over time.

Both have scale, strong tenant relationships and access to capital, but their growth profiles are not the same. The better choice depends on whether an investor wants a steadier income story or a stronger long-term growth engine.

The Case for Realty Income

Realty Income’s biggest strength is still its dependable business model. The company owned or held interests in more than 15,500 properties at the end of the first quarter of 2026, leased to 1,786 clients across 92 industries. This level of diversification helps reduce reliance on any single tenant, property type or market. Compared with Prologis, which is more focused on logistics real estate, Realty Income gives investors broader exposure across retail, industrial, gaming and other net lease categories.

The company also continues to deliver steady operating performance. In the first quarter, Realty Income reported 98.9% portfolio occupancy, a rent recapture rate of 103.4% on re-leased properties and 6.6% year-over-year AFFO per share growth. Those are solid numbers for a large, mature REIT. Realty Income also raised its 2026 AFFO per share guidance and increased its full-year investment volume outlook to $9.5 billion, showing that management still sees room to deploy capital at scale.

Another positive is Realty Income’s dividend record. The company has declared hundreds of consecutive monthly dividends and has increased its dividend for more than 31 straight years as a public company. For investors who mainly want predictable income, that consistency is hard to ignore. Prologis also pays a dividend, but Realty Income’s identity is more clearly built around monthly cash returns and a long history of dividend growth.

However, Realty Income’s growth profile is not as exciting as Prologis’. Same-store rental revenues increased only 0.8% in the first quarter, and its 2026 AFFO per share growth guidance points to a low-single-digit growth rate. Its private capital partnerships with Apollo and GIC, along with its U.S. Core Plus fund, could help over time, but the business still looks more like a steady income compounder than a faster-growing real estate platform.

The Case for Prologis

Prologis stands out because it sits at the center of global logistics. The company owns or has investments in properties and development projects expected to total about 1.3 billion square feet across 20 countries, serving roughly 6,500 customers. Compared with Realty Income’s more diversified net lease model, Prologis has a sharper focus on warehouses and supply chain infrastructure, which remain critical to e-commerce, retail distribution, manufacturing and business-to-business activity.

Its first-quarter results showed that demand is still healthy. Prologis delivered record leasing, with 64 million square feet of lease signings and 66.7 million square feet of leases commenced across its operating and development portfolio. Occupancy was 95.3%, retention was 75.8%, and cash same-store NOI grew 8.8%. These figures compare well with Realty Income’s steadier but slower same-store rental revenue growth, and they point to stronger internal growth from Prologis’ existing portfolio.

Prologis also has a stronger development engine. During the quarter, it started $1.78 billion of development on its share, with an estimated value creation of $571 million from development starts. Its build-to-suit activity is especially important because it shows that large customers are still willing to commit to new space. Its broader platform includes logistics assets, data centers and energy. The data center angle is especially important, as Prologis has been advancing power-secured sites and build-to-suit projects tied to major technology demand. Realty Income is also deploying capital at scale, but Prologis has a more visible path to creating value through development.

The balance sheet and capital platform add another layer to the case. Realty Income has a solid balance sheet, supported by $3.9 billion of available liquidity, net debt to adjusted EBITDAre of 5.2X and strong investment-grade ratings. Prologis looks even stronger, with $6.7 billion of liquidity, debt-to-adjusted EBITDA of 4.8X, a 3.3% weighted average interest rate and an 8.1-year debt term. Both are well-positioned, but PLD has better financial flexibility.

Prologis also expanded its Strategic Capital platform through partnerships with GIC and La Caisse. Like Realty Income, Prologis is using private capital to grow, but PLD’s platform appears more directly tied to high-growth logistics, data center and energy opportunities.

How Do Estimates Compare for Realty Income & Prologis?

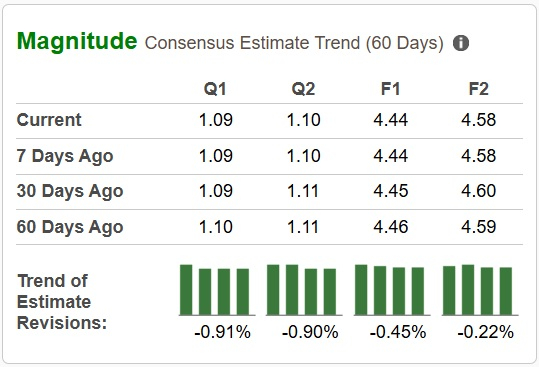

The Zacks Consensus Estimate for Realty Income’s 2026 and 2027 sales implies year-over-year growth of 8.55% and 7.33%, respectively. The consensus mark for 2026 and 2027 funds from operations (FFO) per share suggests a year-over-year increase of 3.74% and 3.28%, respectively. Over the past month, estimates for O’s 2026 and 2027 FFO per share have been tweaked southward.

For Realty Income:

Image Source: Zacks Investment Research

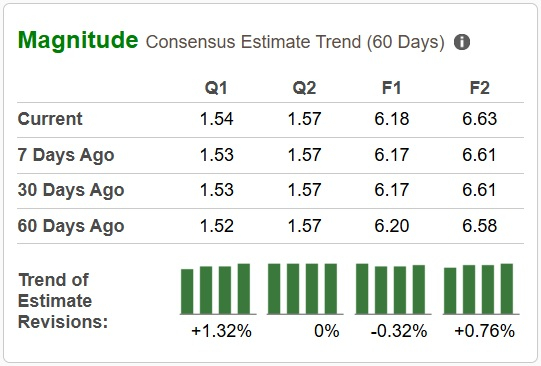

The Zacks Consensus Estimate for Prologis’ 2026 and 2027 sales calls for year-over-year growth of 4.92% and 3.39%, respectively. The consensus estimates for both 2026 and 2027 FFO per share have been revised marginally upward over the past seven days. The figures suggest a year-over-year increase of 6.37% and 7.28%, respectively.

For Prologis:

Image Source: Zacks Investment Research

Price Performance and Valuation of O & PLD

So far in the year, Realty Income shares have risen 9.4%, while Prologis stock has rallied 14.1%. In comparison, the S&P 500 composite has advanced 10.4% in the same time frame.

Image Source: Zacks Investment Research

O is trading at a forward 12-month price-to-FFO, which is a commonly used multiple for valuing REITs, of 13.70X, which is above its three-year median.

Meanwhile, PLD is presently trading at a forward 12-month price-to-FFO of 22.94X, which is also above its three-year median of 20.81X. Both O and PLD carry a Value Score of D.

Image Source: Zacks Investment Research

Conclusion: PLD Has the Edge

Realty Income remains a strong REIT for investors who value monthly income, high occupancy and a diversified net lease portfolio. It is steady, proven and built for dependable cash flow. However, Prologis looks like the better stock to consider now for investors seeking a stronger blend of quality and growth. Its record leasing, stronger same-store NOI growth, global logistics footprint, development pipeline, and expanding data center and energy opportunities give it more ways to compound over time. Realty Income is the steadier income play, but Prologis has the more compelling long-term growth setup. Estimate revisions also suggest that Prologis stands out as the better REIT pick currently.

While PLD carries a Zacks Rank #2 (Buy), O has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Note: Anything related to earnings presented in this write-up represent funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Prologis, Inc. (PLD): Free Stock Analysis Report

Realty Income Corporation (O): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).