CONMED Corporation CNMD is well-positioned for growth on the back of rising adoption of its high-margin, differentiated platforms like AirSeal, Buffalo Filter and BioBrace. The company’s long-term prospects seem good as robotic procedure volume rises, coupled with the expanding penetration of Ambulatory Surgery Centers. Moreover, improving supply-chain bottlenecks should drive top- and bottom-line growth.

CONMED is facing tariff headwinds that are unfavorably impacting its earnings per share (EPS) and revenue expansion. Higher operating expense investments remain a concern.

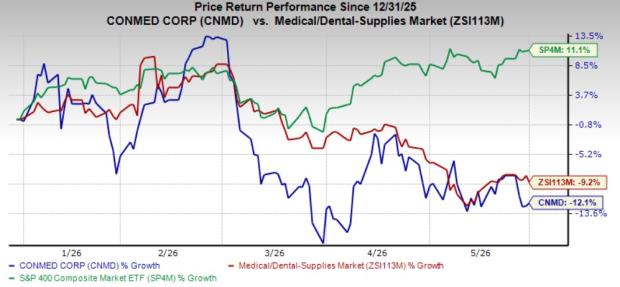

Shares of this Zacks Rank #3 (Hold) company have lost 12.1% in the year-to-date period, underperforming the industry’s 9.2% decline and the S&P 500 Index’s 11.1% return.

Image Source: Zacks Investment Research

CONMED, a renowned global medical products manufacturer specializing in surgical instruments and devices, has a market capitalization of $1.07 billion. The company projects 5.1% earnings growth over the next five years.

The company’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 5.38%.

Factors Favoring CNMD Stock

Strategic Portfolio Simplification Should Improve Growth and Margin Quality: CONMED’s decision to fully exit its gastroenterology (GI) product portfolio represents a significant strategic shift toward higher-growth and higher-margin businesses. Management emphasized that the divestiture allows the company to redirect capital, commercial resources and management attention toward AirSeal, Buffalo Filter and BioBrace — three platforms with stronger competitive positioning and better long-term economics. While the GI business historically contributed to revenue generation, it carried lower strategic relevance and diluted growth rates. By concentrating investments on minimally invasive surgery, smoke evacuation and orthopedic soft tissue repair, CONMED is creating a more focused portfolio that should support faster organic growth, improved margin expansion and a clearer investment narrative over the next several years.

AirSeal Continues to Benefit From Multiple Structural Growth Drivers: AirSeal remains one of CONMED’s most important growth assets, supported by both robotic surgery expansion and underpenetrated laparoscopic procedures. The company now has an installed base exceeding 10,000 systems globally, providing recurring disposable revenues and strong surgeon familiarity. Beyond robotics, management highlighted that AirSeal is currently utilized in only 6-7% of the more than three million laparoscopic procedures performed annually in the United States, suggesting a substantial runway for adoption. CONMED placed more than 50% additional AirSeal units into the market compared with the prior-year quarter, which should support future disposable utilization. This combination of installed-base growth and low market penetration creates an attractive long-term growth profile.

BioBrace Emerging as a Differentiated Orthopedic Growth Platform: BioBrace continues to gain traction as a next-generation soft tissue repair technology and is increasingly becoming a cornerstone of CONMED’s orthopedic strategy. The implant uniquely combines structural reinforcement with biologic healing support, differentiating it from competing repair solutions. Management noted that surgeons are expanding the use of BioBrace across both primary repairs and more complex procedures, with more than 30 published studies strengthening clinical confidence. Additionally, the ongoing 268-patient randomized controlled trial could provide a powerful clinical catalyst. The trial is expected to complete enrollment in 2026. As orthopedic surgeons increasingly prioritize biologic augmentation and durability of repair outcomes, BioBrace appears well-positioned to capture share within a large and growing sports medicine market.

Supply Chain Recovery Creating Opportunity for Market Share Recapture: After several years of operational challenges, CONMED appears to be making meaningful progress in restoring supply chain reliability. Management stated that improvements achieved in late 2025 have been sustained through the first quarter of 2026, enabling orthopedic sales teams to become more proactive with customers rather than focusing primarily on product availability issues. Orthopedics delivered mid-single-digit growth for the third consecutive quarter, supported by improved service levels and stronger execution. Management believes customer relationships remained intact during supply disruptions, creating an opportunity to gradually regain lost business as contracts renew. A more reliable supply chain should not only support revenue growth but also improve operational leverage and customer confidence over time.

Downsides of CNMD Stock

Rising Debt Costs Could Become a Meaningful Earnings Headwind: CONMED faces increasing financing costs as it refinances upcoming debt obligations. Management indicated that replacing expected convertible financing with traditional bank debt will increase interest expense and create at least a 10-cent EPS headwind in 2026, with potential implications extending into 2027. Long-term debt stood at approximately $860 million, while leverage remains around 3.1x EBITDA. Although management emphasized strong banking relationships and liquidity access, higher borrowing costs reduce financial flexibility and may limit future capital deployment options. In an environment where medtech valuations remain depressed and interest rates elevated, refinancing risk could continue to weigh on earnings growth and shareholder returns.

Smoke Evacuation Growth Still Being Offset by Weak OEM Performance: Buffalo Filter remains a compelling long-term opportunity, particularly as more states adopt smoke-free operating room legislation. However, near-term growth continues to be constrained by weakness in the OEM smoke evacuation business, which management described as a “meaningful headwind” during the first quarter. The OEM portion remains volatile and lumpy, creating quarterly revenue fluctuations that can mask the stronger performance of the direct smoke business. While management expects direct smoke evacuation to increasingly dominate the revenue mix over time, the transition period could create uneven growth patterns. Investors may therefore continue to see variability in reported performance despite favorable long-term legislative and clinical adoption trends.

Inflationary and Cost Pressures Could Limit Margin Expansion: Management acknowledged ongoing cost inflation across several key inputs, including oil-based materials, precious metals and medical device components. Although CONMED currently believes these pressures are incorporated into guidance and manageable through supplier negotiations and pricing actions, the company remains vulnerable to broader macroeconomic and geopolitical developments. Gross margin improved 100 basis points in the first quarter, aided by a favorable product mix, but sustaining that improvement may become increasingly difficult if commodity inflation accelerates or supply chain costs rise further. Given the company’s ongoing investment cycle and refinancing-related interest expense pressures, any inability to offset cost inflation could constrain future margin expansion and earnings growth.

Estimate Trend

CONMED is witnessing a stable estimate revision trend for 2026. In the past 60 days, the Zacks Consensus Estimate for earnings has improved 2 cents to $4.38 per share.

The Zacks Consensus Estimate for second-quarter fiscal 2026 revenues and EPS is pegged at $337.2 million and $1.10, suggesting 1.5% and 4.4% declines, respectively, from the year-ago reported numbers.

CONMED Corporation Price

CONMED Corporation price | CONMED Corporation Quote

Stocks to Consider

Some better-ranked stocks from the broader medical space are Pacific Biosciences of California PACB, Globus Medical GMED and Biodesix BDSX.

Globus Medical, sporting a Zacks Rank #1 (Strong Buy) at present, reported first-quarter 2026 adjusted EPS of $1.12, which outpaced the Zacks Consensus Estimate by 21.7%. Revenues of $760 million surpassed the Zacks Consensus Estimate by 4%. You can see the complete list of today’s Zacks #1 Rank stocks here.

GMED has an estimated long-term earnings growth rate of 10.2% compared with the industry’s 12.6% appreciation. The company beat earnings estimates in each of the trailing four quarters, with the average surprise being 26.26%.

Pacific Biosciences of California, currently carrying a Zacks Rank #2 (Buy), reported a first-quarter 2026 adjusted loss per share of 12 cents, which surpassed the Zacks Consensus Estimate by 29.4%. Revenues of $37 million missed the Zacks Consensus Estimate by 9.3%.

PACB’s earnings are estimated to improve at a rate of 22.6% compared with the industry’s 13.3% growth in 2026. The company beat earnings estimates in each of the trailing four quarters, with the average surprise being 29.76%.

Biodesix, currently carrying a Zacks Rank of 2, reported a first-quarter 2026 adjusted loss per share of 81 cents, which beat the Zacks Consensus Estimate by 35.71%. Revenues of $26 million beat the Zacks Consensus Estimate by 12.3%.

BDSX has an estimated earnings growth rate of 36% for 2026 compared with the industry’s 12.5% return. The company beat earnings estimates in three of the trailing four quarters and missed once, with the average surprise being 25.56%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CONMED Corporation (CNMD): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Pacific Biosciences of California, Inc. (PACB): Free Stock Analysis Report

Biodesix, Inc. (BDSX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).