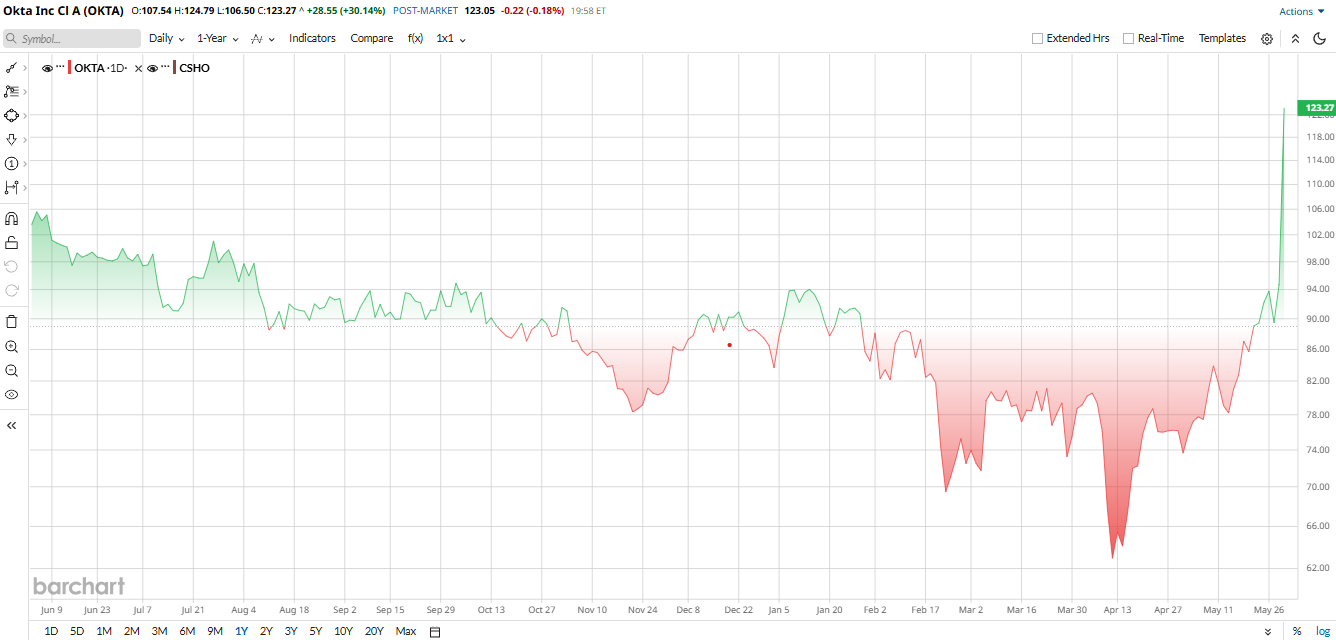

Okta (OKTA) has gone from a forgotten software name to one of the market’s loudest AI security stories in a matter of weeks. That is saying something in 2026, because software stocks have been battling a simple fear. Investors keep asking whether AI will eat the software world or help the right software names grow faster. Okta is landing in the second camp. The company helps manage identity, access, and security. That makes it a natural fit for a world where people are not the only users anymore. AI agents are showing up, too. And that is exactly the story investors loved when Okta reported earnings and the stock jumped about 30% to a 52-week high, after a long stretch of doubt earlier this year.

That signals the turnaround story for the software company has finally begun.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Okta Stock Is Suddenly Back in Favor

Okta is still the independent identity company that sits between users and the apps they touch. That sounds boring. It is not. It is the gatekeeper. And in an AI world, gatekeeping is valuable. Companies do not want their identity layer locked into one cloud provider. They want something neutral. Okta keeps pitching that idea, and now it is pitching the same idea for AI agents. That is the part of the business investors are starting to notice.

The stock has had a wild ride. In early 2026, Okta stock plunged because the market was still worried about a software selloff and AI disruption. Fast forward to now, and the picture looks very different.

Now, Okta is up 61.7% year-to-date and up 35.5% over the past 12 months. The stock is also trading well above its 50-day average of $79.52 and its 200-day average of $85.15, which tells you the trend has turned sharply higher. The move is not just momentum for momentum’s sake either. It is a reaction to stronger execution, better guidance, and a cleaner AI story.

Valuation is where investors need to take a breath. Okta is not cheap. Its trailing PE ratio is 94.82x, and its forward PE is 20.62x. Its enterprise-value-to-sales ratio is 6.57x. That is a rich setup for any software company, even one with improving growth. The market is clearly paying up for a stronger product cycle, and the hope that AI identity can become a bigger business than expected.

www.barchart.com

www.barchart.com Okta's Business Is Getting Stronger

The real spark came from the latest quarter. Okta reported first quarter fiscal 2027 revenue of $765 million, up 11% year-over-year. Subscription revenue was $750 million, also up 11%. RPO reached $4.7 billion, up 16%, while current RPO rose 12% to $2.5 billion.

Net income was $74 million, up from $62 million a year earlier. EPS came in at $0.91, up from $0.86. Free cash flow was $271 million, and the company ended the quarter with $2.6 billion in cash, cash equivalents, and short-term investments. CEO Todd McKinnon said AI agents are becoming a new workforce, and that is the kind of line that fits the moment.

Okta then guided second-quarter revenue to $790 million to $794 million and full-year fiscal 2027 revenue to $3.19 billion to $3.2 billion, with full-year non-GAAP EPS of $3.79 to $3.87.

What Else Is Driving Growth in 2026?

Okta is not just talking about AI. It is shipping around it. In May, the company expanded Okta for AI agents to support new agent ecosystems, any identity provider, and governance across enterprise resources. It also added an integration with Amazon Bedrock AgentCore. Okta is trying to secure AI agents whether they live inside Okta’s world or not. That matters because the market is moving toward hybrid identity stacks, not neat single vendor setups. Okta’s own AI agents report backed up the urgency, saying 58% of executives reported an AI-related security incident or close call in the past year, and 52% of knowledge workers said they use unsanctioned AI tools at work. That is a problem Okta is built to solve.

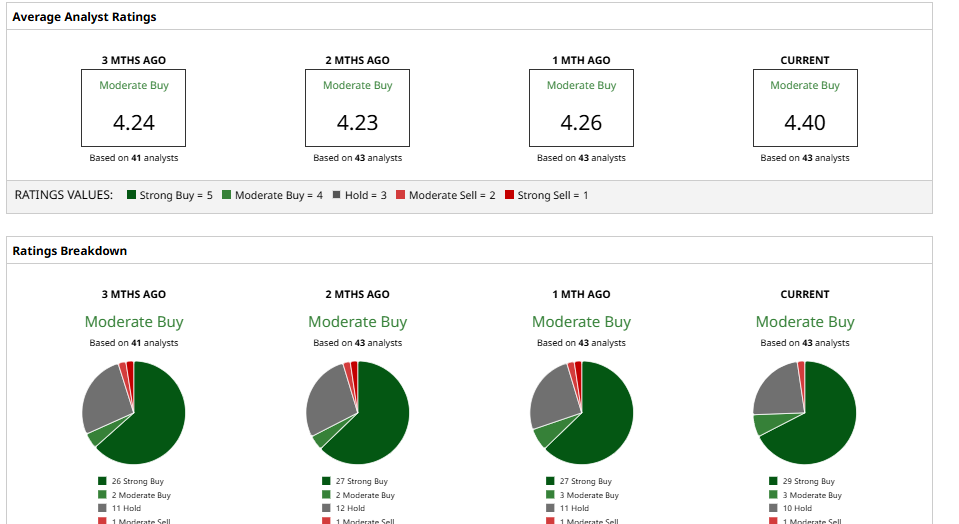

What Wall Street Thinks of OKTA Stock

Analysts are warming up, but they are not all shouting from the rooftops. Barchart shows a consensus “Moderate Buy” on Okta, with an average price target of $106, which sits below the current $123 share price. That means the stock has already outrun the average target. Still, the firm-by-firm calls look stronger.

Royal Bank of Canada raised its target to $122 and kept an “Outperform” rating. Oppenheimer lifted its target to $125 and stayed “Outperform.” Needham moved its target to $120 and kept “Buy.” BMO Capital also raised its target to $120 and kept “Outperform.” The Street likes the setup, but it also knows a big earnings pop can get ahead of itself fast.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $5 Billion Reason to Buy Salesforce Stock Now Nvidia CEO Jensen Huang Is Building the Future Faster Than Infrastructure Can Support It Dell Stock Is the New Nvidia of AI Infrastructure Why Okta Is One of the Hottest AI-Driven Stocks to Buy Now