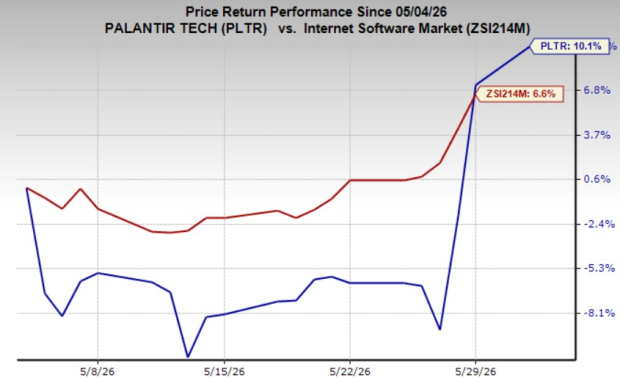

Palantir Technologies PLTR has rebounded strongly following the recent software-sector selloff, with shares gaining 10% over the past month.

The recovery reflects renewed investor confidence in the company’s expanding role within the artificial intelligence ecosystem. More importantly, Palantir’s latest financial profile increasingly suggests that the company is evolving beyond the framework of a traditional software business.

Palantir’s Financial Profile Continues to Strengthen

The most striking aspect of Palantir’s recent quarter was not just its 85% revenue growth but the extraordinary profitability achieved alongside that expansion. The company reported adjusted operating margins of 60%, adjusted free cash flow margins of 57%, and a GAAP net margin of 54% while generating $1.63 billion in revenues. Such profitability levels remain extremely rare among rapidly scaling software companies, which typically experience margin compression as operating expenses rise.

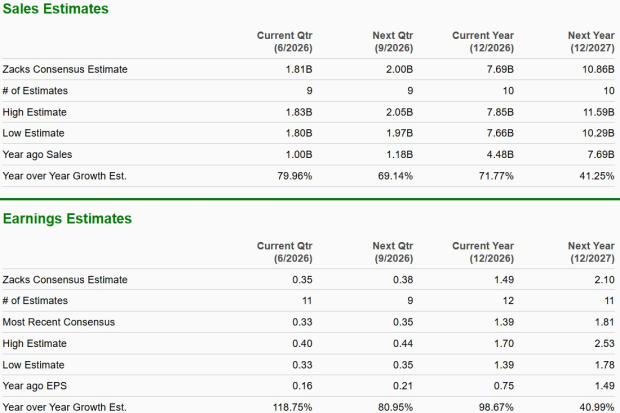

Management’s forward outlook further strengthened the bullish narrative. Palantir guided for approximately $7.66 billion in fiscal 2026 revenues alongside projected adjusted operating income exceeding $4.44 billion and adjusted free cash flow of around $4.4 billion. These projections suggest Palantir could soon generate more free cash flow annually than many mature software companies produce from their entire operations.

Underlying customer metrics also continue to reinforce the long-term growth story. The company’s net dollar retention rate climbed to 150%, signaling strong expansion among existing customers. Additionally, U.S. commercial remaining deal value surged 112% year over year, indicating that enterprises are significantly increasing adoption of Palantir’s Artificial Intelligence Platform after initial deployment success.

AI Infrastructure Dynamics Differentiate Palantir

Palantir increasingly resembles an AI infrastructure provider rather than a conventional SaaS business. As artificial intelligence models become more accessible and commoditized, organizations may place greater importance on platforms capable of integrating, managing and operationalizing those models effectively across large-scale workflows.

This shift could work heavily in Palantir’s favor. Once deployed, the company’s platforms generate powerful scaling dynamics because incremental usage carries relatively low additional costs. That helps explain how Palantir continues expanding margins even during hypergrowth.

Its Rule of 40 score of 145 further highlights the unusual economics of the business. Very few companies in technology history have managed to sustain such elevated growth rates while simultaneously maintaining exceptionally high free cash flow margins. This combination increasingly supports the argument that Palantir deserves to be viewed differently from traditional software firms.

Analyst Sentiment Remains Highly Favorable

Consensus estimates continue to support Palantir’s growth trajectory. Earnings are projected to increase 98.7% in 2026 and 41% in 2027, while revenue growth expectations remain robust at 72% in 2026 and 41% in 2027, as commercial AI adoption accelerates.

Analyst sentiment has also improved considerably. Over the past 30 days, analysts issued 11 upward earnings estimate revisions for 2026 without any downward revisions. Forecasts for 2027 also moved higher with 10 upward revisions against none downward, reflecting growing confidence in Palantir’s execution capabilities and expanding AI opportunity.

Peer View

Snowflake SNOW remains one of the most important competitors within enterprise data analytics and AI infrastructure. Like Palantir, Snowflake benefits from growing enterprise demand for cloud-based data platforms and AI-driven analytics solutions. However, Snowflake maintains greater exposure to cloud data warehousing and enterprise data-sharing ecosystems.

C3.ai AI also competes within the enterprise artificial intelligence market, particularly in predictive analytics and AI application deployment. Similar to Palantir, C3.ai focuses heavily on helping enterprises operationalize AI workflows across industries. Still, C3.ai continues to face greater questions about profitability, consistency, and large-scale commercial adoption.

Is PLTR Stock Still a Buy?

Palantir increasingly looks like a foundational AI infrastructure company rather than a conventional software provider. Its expanding profitability, exceptional customer retention metrics, and strong free cash flow generation continue to reinforce the long-term investment thesis. Although valuation multiples remain elevated and market expectations are extremely ambitious, the company’s operational execution continues to support bullish sentiment. The biggest risk lies in whether Palantir can consistently exceed the enormous expectations already embedded in the stock price. Still, the combination of accelerating AI adoption, infrastructure-like economics and improving enterprise dependency on its platforms suggests the long-term opportunity remains compelling. For growth-oriented investors willing to tolerate volatility, PLTR still appears to be a buy.

PLTR stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

C3.ai, Inc. (AI): Free Stock Analysis Report

Snowflake Inc. (SNOW): Free Stock Analysis Report

Palantir Technologies Inc. (PLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).