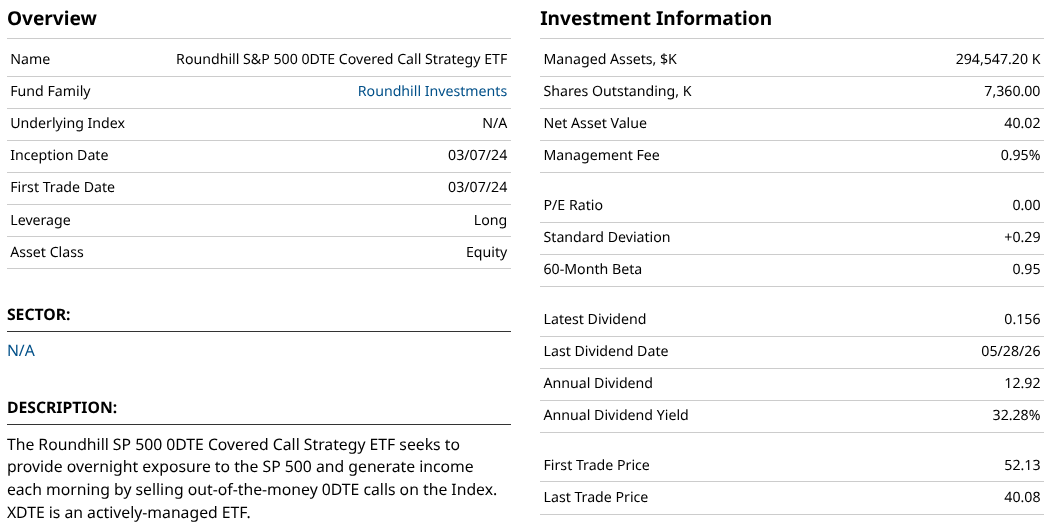

The modern yield-hunting crowd has officially found a new obsession: 0DTE (zero days to expiration) covered call ETFs, spearheaded by vehicles like the Roundhill S&P 500 0DTE Covered Call Strategy ETF (XDTE) and the YieldMax S&P 500 0DTE Covered Call Strategy ETF (SDTY).

Do we really need them?

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

Let’s see how this new product in the ETF market has done during its first two years and three months of life.

www.barchart.com

www.barchart.com Instead of writing standard monthly or weekly options, these funds sell call options that expire at the close of every single trading session. By grabbing some intraday premium from the market’s constant chopping around, they promise breathtaking, annualized distribution yields frequently crossing 25% to 35% — often distributed to shareholders on a weekly basis.

But here’s the thing: Cash flow is not the same as investment performance. Not if the ETF is essentially paying you with your own money. Thus, we need to understand how they actually hold up when market structure breaks down, and whether they are a fundamentally superior investment.

Did They Hold Up During the Early 2026 Decline?

The early 2026 technical correction served as a perfect real-world stress test for the 0DTE mechanism. The verdict? They performed exactly how mathematical option theory predicted. They mitigated the bleeding, but they still suffered.

www.barchart.com

www.barchart.com That has resulted in XDTE trailing the SPDR S&P 500 Trust (SPY) by a 51% to 43% margin since the latter’s inception. For each of its first two completed years, 2024 and 2025, XDTE captured about 70% of SPY’s total return. Is it worth it, just to get something you can call “income” out of it? Not to me.

If we look at what happens at the extremes, I think it explains that conclusion. During a multi-week cascading drop, selling 0DTE options behaves differently than selling standard 30-day options. Every single morning, the fund writes fresh out-of-the-money or at-the-money calls, pocketing an elevated intraday premium because the CBOE Volatility Index ($VIX) has spiked.

That’s what happened during the sudden market drops we saw earlier this year. The S&P 500 fell by 9% in a matter of weeks. The same type of thing occurred back during the tariff chaos in early 2025, except that decline was 19% in just seven weeks.

On days when the market falls straight down from the opening bell, that 0DTE premium expires completely worthless, providing an instant cash cushion that allows the ETF to slightly outperform the raw index on a daily basis.

When the market is in a structural downtrend, it doesn’t just drift lower during regular trading hours. It gaps down overnight. Because XDTE and SDTY maintain a synthetic or direct long exposure to the S&P 500, they take the full brunt of those overnight gap-downs. The premium captured during the day cannot mathematically compensate for a major multi-point gap at the next morning’s opening bell. So what XDTE and its ilk giveth, it also taketh away.

Are They Any Better Than Owning SPY?

The short answer is no, unless your sole, strict objective is immediate liquidity extraction at the expense of long-term wealth creation.

To understand the structural difference, compare a 0DTE income fund to the traditional heavyweights. SPY is built to capture the unlimited upside of the S&P 500 Index ($SPX). It doesn’t cap its upside as XDTE and its peers do.

So, if the S&P 500 stages a massive 2.5% vertical intraday breakout, a 0DTE fund will only participate in the move up to its written strike price. Over time, this creates some lopsided math for investors. You get much of the downside during crashes, but you do not participate much during massive, vertical recovery days. Long-term data shows SPY’s total return profile fundamentally outperforms the 0DTE structure over a full market cycle.

0DTE ETFs are an engineering marvel of modern financial plumbing, but they are not magic money trees. They are highly complex, derivative-heavy income investments. But if the markets are more mixed or worse going forward, I have a strong suspicion that the proof will be in that pudding. And that many disillusioned investors will be the result.

It is easy to say you’ll be OK with a fund handing you a nice yield while the price declines net out to a 20%-30% loss. But when it actually happens? The reality often produces a different reaction.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

These New 0DTE Covered Call ETFs Are Not Magic Money Trees. In Fact, You’re Better Off Just Buying SPY. Investors Bearish on Oracle Ahead of Earnings - Unusually Heavy ORCL Put Options Trading Microsoft Stock Still Looks Cheap - Shorting One-Month Puts Has a 2.0% Yield How to Buy CROX for an 11% Discount, or Achieve a 30% Annual Return