As an investment theme, artificial intelligence stocks have been one of the best in the stock market for several quarters. Since Jan. 1, 2024, the Nasdaq CTA Artificial Intelligence Index, which tracks the software, hardware, and service providers in the industry, is up 118%. And the Global X Artificial Intelligence & Technology ETF (AIQ), which tracks AI and big data stocks, is up 101%. Both of those handily beat the 59% return of the S&P 500 in that same time.

But don’t despair if you’ve still not brought some of these AI stocks into your portfolio. Wedbush analyst Dan Ives, who is recognized as one of the top AI and tech analysts on Wall Street, says that the AI boom still has plenty of staying power. He estimates that companies will eventually spend $4 trillion on AI development and implementation, which will fuel growth throughout the industry.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

“This AI party started at 9 p.m.,” Ives told CNBC. “It’s about 11, 11:30 p.m. That party goes to 4 a.m., and I think that’s why we’re still in the early days."

Two companies that Ives singled out as particularly strong cases right now are Snowflake (SNOW) and Datadog (DDOG), which he says prove that investors can find promising stocks beyond chip and data center stocks. “That’s showing it's spreading to the software use cases,” he said.

Let’s look at both companies.

Snowflake

Snowflake offers a cloud-based platform that helps organizations store, manage, and analyze data across different cloud services. The company, which is based in Menlo Park, California, has a market capitalization of $88 billion.

Snowflake stands out because its system is designed to work seamlessly with the major cloud providers — Amazon (AMZN) Web Services, Microsoft (MSFT) Azure and Alphabet’s (GOOG) (GOOGL) Google Cloud. The company leans into the AI space through its AI Data Cloud, which allows companies to build, test, and operate AI-powered applications in cloud environments. Snowflake has more than 13,900 global customers that average 6.3 billion daily queries on the Data Cloud.

Earnings from the company’s first quarter of fiscal 2027 (ending April 30, 2026), showed revenue of $1.39 billion, up 33% from a year ago. The company added 616 net new customers in the quarter, up 38% from a year ago, and expanded its partnership with AWS through a $6 billion, multi-year agreement to accelerate enterprise AI adoption.

“AI continues to be a powerful tailwind for Snowflake, and Q1 marks a clear inflection point in that journey,” CEO Sridhar Ramaswamy said.

However, it should be noted that Snowflake isn’t turning a profit. With heavy investments into sales, marketing, and development, the company posted an operating loss of $326.2 million in the quarter. The company issued fiscal Q2 revenue guidance of $1.415 billion to $1.420 billion, up 30% from a year ago.

Forty-five analysts who cover SNOW stock have a consensus “Strong Buy” rating, with a mean price target of $277 that is just above the current stock price. Considering that Snowflake stock is up 86% in the last month, I expect analysts to begin raising their price targets soon.

www.barchart.com

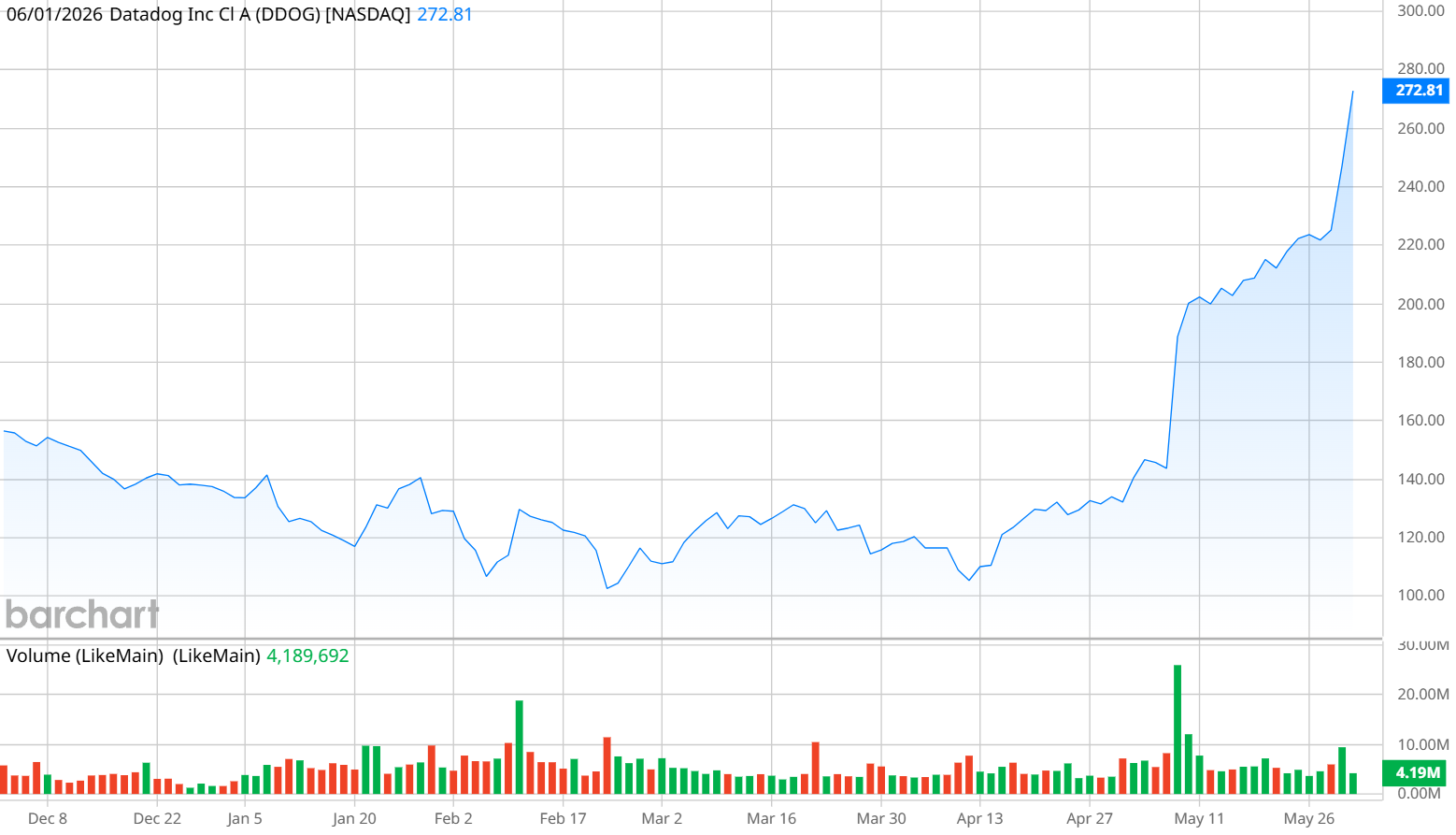

www.barchart.comDatadog

Datadog operates a cloud-based monitoring and analytics platform that monitors servers, applications, and cloud-based infrastructure and provides real-time analytics to allow operators to identify and correct problems. Its platform can connect to and monitor many existing tech systems without customers having to build custom connections — meaning that it functions with public and private clouds, physical servers, and third-party software tools.

The New York-based company also has a market cap of $88 billion. Revenue in the first quarter was $1 billion, up 32% from a year ago, and net income was $52.6 million, which more than doubled from Q1 2025. Diluted earnings per share were $0.15, versus $0.07 a year ago.

“We showed broad-based acceleration of revenue growth across cohorts, including both our AI and non-AI customers,” CEO Olivier Pomel said. “Our AI-native customer cohort continues to grow and diversify rapidly both in the number of customers we serve and the scale of those customers.”

In addition, the company saw revenue growth of 25% from non-AI customers, accelerating from 19% a year ago. “We think this is a sign of strong continued cloud migration, greater adoption of our products, and customers of all kinds accelerating their use of AI,” Pomel said.

Datadog issued Q2 guidance for revenue between $1.07 billion and $1.08 billion. DDOG stock is also up more than 91% in the last month and shows a mighty gain of 128.6% in the last year. Nearly four dozen analysts who cover DDOG stock also have it as a consensus “Strong Buy,” with a mean price target of $226 that is far below the current price of $269 at this writing.

www.barchart.com

www.barchart.com On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

These 2 AI Software Stocks Are Through the Roof. Dan Ives Says There’s Still Time to Buy. This Trade for Adobe Systems Profits if the Stock Stays Above $220 S&P Futures Muted as Fresh U.S.-Iran Hostilities Lift Oil and Bond Yields, ADP Jobs Report and Broadcom Earnings on Tap This Dividend Stock Has Rebounded as ‘AI-Pocalypse’ Fears Subside. Buy It Now.